20/01/2013

- What Exactly is a Joint Bank Account?

- Who Can Open a Joint Bank Account?

- What Does a Joint Account Offer?

- Types of Joint Bank Accounts

- How to Choose the Best Joint Bank Account

- How Do Joint Bank Accounts Work?

- Can I Convert a Personal Bank Account to a Joint Account?

- Can a Joint Account Affect Your Credit Rating?

- Joint Bank Accounts and Debt Responsibility

- Disputes and Closing a Joint Bank Account

- Joint Accounts and Mental Incapacity

- What Happens to a Joint Bank Account When Someone Dies?

- Frequently Asked Questions (FAQs)

- Conclusion

What Exactly is a Joint Bank Account?

A joint bank account is a single bank account shared by two or more individuals. This financial arrangement is not exclusively for couples; friends, housemates, and even business partners can benefit from shared accounts to streamline their financial management. The key advantage lies in the ease of access and convenience it offers for managing shared expenses, such as rent, utility bills, or mortgage payments. Essentially, it consolidates finances, making it simpler to track spending and ensure bills are paid on time.

Who Can Open a Joint Bank Account?

Generally, any two or more individuals aged 18 or over can open a joint bank account. There's no requirement for a familial or romantic relationship. The most common pairings include couples, family members (such as parents and adult children), or housemates pooling resources for shared living costs. Crucially, all applicants must meet the bank's standard eligibility criteria, which typically includes providing proof of identity and address.

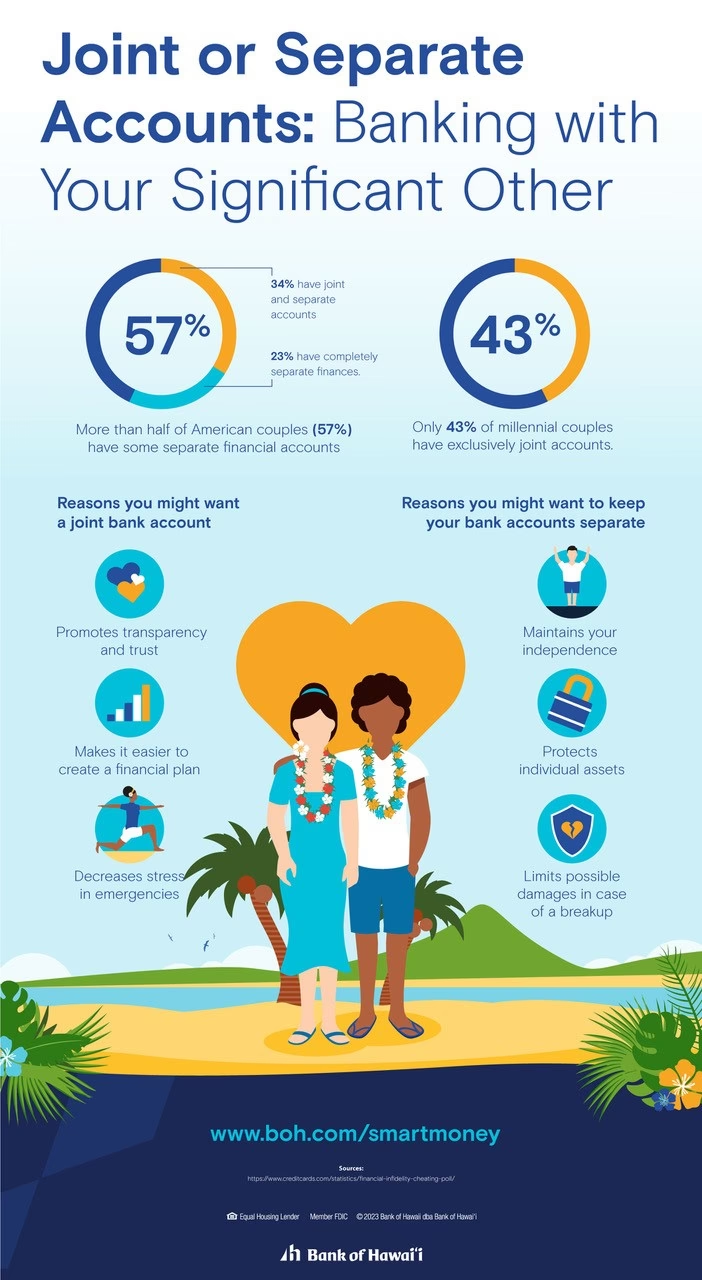

What Does a Joint Account Offer?

Joint accounts offer a centralised hub for shared finances, simplifying the process of managing money with others. Here's a breakdown of the key benefits:

- Simplified Expense Management: Easily pay for shared bills, rent, groceries, and other joint expenses without the need for constant transfers between individual accounts.

- Enhanced Transparency: All account holders have visibility into transactions and the account balance, fostering transparency and trust, especially for partners or close associates.

- Streamlined Budgeting: Pooling funds for shared expenses into one account makes budgeting and tracking overall spending much more straightforward.

- Convenience: Having a single account for shared outgoings reduces administrative hassle and makes it easier to manage day-to-day finances collectively.

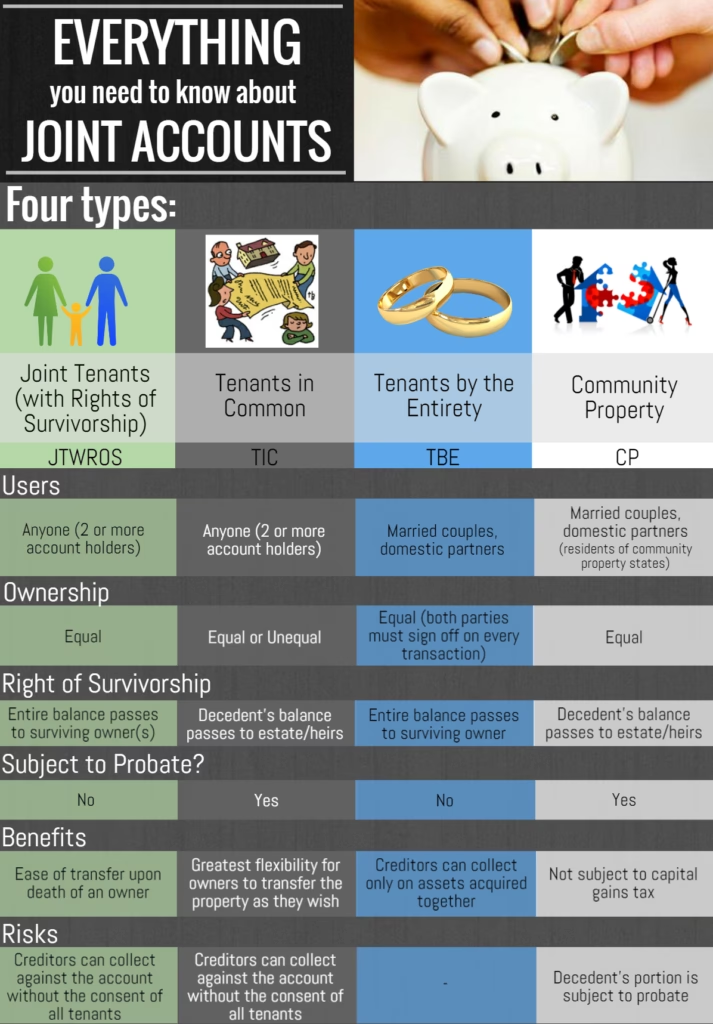

Types of Joint Bank Accounts

In the UK, joint bank accounts can be broadly categorised into three main types:

1. Standard Joint Bank Accounts

These are the most common and offer essential features for everyday banking, including debit cards for each holder, online and mobile banking access, and potentially overdraft facilities (subject to approval and credit checks).

2. Packaged Joint Bank Accounts

These accounts come with additional perks and benefits, such as travel insurance, mobile phone insurance, breakdown cover, or cashback rewards, in exchange for a monthly fee. They can be cost-effective if the value of the included benefits exceeds the monthly charge.

3. Basic Joint Bank Accounts

Designed for individuals who may not qualify for standard accounts (perhaps due to credit history) or prefer a no-frills banking solution. These accounts provide essential services like receiving payments and paying bills but typically lack features like overdrafts or cheque books.

How to Choose the Best Joint Bank Account

Selecting the right joint account depends on your specific needs and priorities. Consider the following factors:

Features and Functionality

Assess whether you need features like cheque books, the convenience of mobile and online banking, or additional perks such as cashback or rewards. Choose an account that provides the tools and services necessary for your shared financial management.

Account Fees

Be mindful of any monthly maintenance fees, transaction charges (especially for international use), and overdraft fees. Opt for accounts with transparent and competitive fee structures that align with your expected usage.

Customer Service and Accessibility

Research the provider's reputation for customer service. Consider their accessibility through various channels (phone, online chat, branches) and read customer reviews to gauge their responsiveness and helpfulness.

Interest Rates and Savings Features

While less common for current accounts, some joint accounts may offer interest on balances. If growing your savings is a goal, look for accounts with competitive interest rates.

How Do Joint Bank Accounts Work?

When opening a joint account, all applicants will need to provide proof of identity and address. The process is similar to opening an individual account, but all parties must apply together. Once the account is active, each holder typically receives a debit card, allowing them to make transactions. It's crucial to understand the 'either-to-sign' versus 'both-to-sign' mechanisms. In an 'either-to-sign' arrangement, any account holder can authorise transactions independently. In a 'both-to-sign' setup, all account holders must approve transactions, offering greater control but potentially less flexibility.

Can I Convert a Personal Bank Account to a Joint Account?

In many cases, yes. Most high street banks allow you to convert an existing personal account into a joint one. However, this often requires both parties to visit a branch or speak to the bank over the phone to complete eligibility and identity checks. Some specific types of personal accounts, like student or youth accounts, may not be convertible. Additionally, some banks, like First Direct and Virgin Money, do not offer this conversion service, requiring you to open a new joint account instead.

Can a Joint Account Affect Your Credit Rating?

Yes, absolutely. Joint accounts create a financial link between account holders, known as 'financial associates'. When you apply for credit, lenders may review the credit reports of all associated account holders. If you share an account with someone who has a poor credit history, it could potentially make it more challenging for you to obtain credit in your own name. This highlights the importance of choosing your joint account partner wisely.

Joint Bank Accounts and Debt Responsibility

It's vital to understand that all account holders are jointly responsible for any debt accrued on a joint account, regardless of who initiated the spending. In an 'either-to-sign' account, any individual holder can alter overdraft limits without the other's permission. The bank can pursue any account holder for an overdrawn balance, even if they were unaware of the extent of the debt.

Disputes and Closing a Joint Bank Account

Disputes: If a disagreement arises, notify your bank immediately. The bank will typically freeze the account or switch it to a 'both-to-sign' status, suspending debit card, cheque book, and online banking access until the dispute is resolved or the account is closed. Essential bills might need to be managed through a separate sole account during this period.

Closing: Some banks allow one person to close a joint account if no dispute is active. Otherwise, both parties must sign a closure form or visit a branch together. Any outstanding overdraft must be cleared before closure. You'll also need to decide how to distribute the remaining funds and what to do with standing orders and direct debits.

Credit Report Disassociation: To prevent a former joint account holder's financial circumstances from affecting your credit applications in the future, contact credit reference agencies (Equifax, Experian, TransUnion) to issue a 'notice of disassociation'.

Joint Accounts and Mental Incapacity

In England and Wales, a joint account may be frozen if one account holder loses mental capacity, unless a power of attorney is in place. This can lead to lengthy and costly legal processes to appoint a deputy. However, in Scotland, banks must allow the other account holder to continue operating the account if it's set up on an 'either-to-sign' basis. Practices vary in Northern Ireland.

What Happens to a Joint Bank Account When Someone Dies?

Typically, when one account holder dies, the funds in a joint account pass automatically to the surviving account holder, allowing them continued access without the need for probate. However, Scottish law has different provisions. After receiving a death certificate, the bank can transfer the account into the survivor's sole name, though overdraft facilities may be reviewed. Tax implications, particularly Inheritance Tax (IHT), can be complex and depend on the relationship between the account holders and the source of the funds.

Frequently Asked Questions (FAQs)

Is there a downside to having a joint bank account?

Yes. Both account holders have equal access to funds, which can lead to disagreements if communication or trust is lacking. Furthermore, both parties are equally liable for any overdrafts or debts, meaning one person's spending can impact the other's financial standing and credit rating.

Can one person withdraw all the money from a joint account?

Generally, yes. Unless the account has specific restrictions (like requiring dual authorisation for withdrawals), any joint account holder typically has the right to withdraw all available funds.

Do all banks offer joint accounts?

Most banks offer joint accounts, but not all. It's advisable to check with your preferred bank or use comparison tools to see their offerings.

Can I set up a joint account as either-to-sign?

Yes, many banks offer both 'either-to-sign' (where any holder can authorise transactions) and 'both-to-sign' (where all holders must authorise transactions) options for joint accounts. This is a crucial feature to consider based on your desired level of control and convenience.

What is the best joint bank account for couples?

The 'best' account depends on individual needs. For couples seeking rewards and perks, the Nationwide FlexPlus is often highly rated. For those prioritising cashback, the Santander Edge Up is a strong contender. Budget-conscious couples might prefer the Monzo Joint Account for its budgeting tools.

Conclusion

A joint bank account can significantly simplify managing shared finances, but choosing the right one is paramount. By understanding the various types, features, and potential implications, you and your co-account holder can select an account that perfectly aligns with your financial goals and lifestyle. Use the information provided to make an informed decision and find your ideal joint banking solution.

If you want to read more articles similar to Understanding Joint Bank Accounts, you can visit the Automotive category.