05/04/2025

Having a car accident can be a deeply unsettling and stressful experience. It's crucial to be well-prepared for such situations to understand precisely how to proceed with getting your vehicle, and potentially those of third parties, repaired. This guide will meticulously walk you through the car insurance claim process and elucidate the various types of insurance available.

- Understanding Car Insurance in the UK

- Types of Car Insurance Explained

- How to Claim on Your Car Insurance After an Accident

- Claiming with Different Insurance Types

- Understanding Car Insurance Excess

- The Value of a No-Claims Bonus

- How Long Do Car Insurance Claims Typically Take?

- Key Takeaways for a Smoother Claim

Understanding Car Insurance in the UK

Car insurance is not merely an option in the United Kingdom; it is a legal mandate. At its core, it's a policy designed to provide financial protection for your vehicle in the unfortunate event of accidents (whether caused by yourself or a third party), damage, or car theft. To comply with UK legislation, you have three primary types of insurance policies to consider: Third Party, Third Party Fire and Theft, and Fully Comprehensive. Each of these policies offers distinct coverage levels and is recommended for different circumstances and vehicle owners.

Types of Car Insurance Explained

To effectively navigate the claims process, it's essential to understand the nuances of each insurance type:

Third Party Insurance (TPO)

Often referred to as Third Party Only (TPO), this represents the most basic level of insurance legally required to drive on UK roads. As its name explicitly suggests, this policy primarily covers third parties involved in an accident where you are at fault. Crucially, any damages sustained by your own vehicle will not be covered and must be financed by yourself. This type of insurance is typically chosen by individuals whose vehicle's repair costs might exceed its market value or the cost of a replacement. Therefore, if you own a less valuable car, TPO might appear to be a financially sensible option. However, it's important to recognise that opting for TPO could lead to a false economy. Incidents such as vehicle theft or fire are not covered under this policy, leaving you entirely responsible for the costs of repair or replacement.

What does Third Party Insurance Cover?

This insurance specifically covers damages to third parties only. This means that if you are the cause of an accident, neither your vehicle nor you personally will be covered by this policy. However, any passengers travelling in your car and other road users involved in the incident will be protected. If you are involved in an accident where you are not at fault, you have the right to claim against the at-fault driver's insurance for the cost of repairing your vehicle.

Third Party, Fire and Theft (TPFT)

Known also as TPFT, this policy represents a step up from TPO and is generally considered the mid-range option for car insurance. With TPFT, you receive the same coverage as TPO, with the significant additions of protection against damages resulting from fire and the unfortunate event of car theft. This insurance is often recommended for owners of used cars who are in a position to cover the costs associated with repairing their own vehicle in the event of an accident that they cause. It offers a balance between cost and essential protection.

Comprehensive Insurance (Fully Comp)

Fully Comprehensive insurance, frequently abbreviated as 'fully comp', offers the most extensive coverage. It encompasses all damages, theft, and accidents, including those where you are found to be at fault. Your liabilities towards third parties, such as injuries sustained by others and damage to their property, are also fully covered under this policy. This is often the preferred choice for many drivers due to the peace of mind it provides.

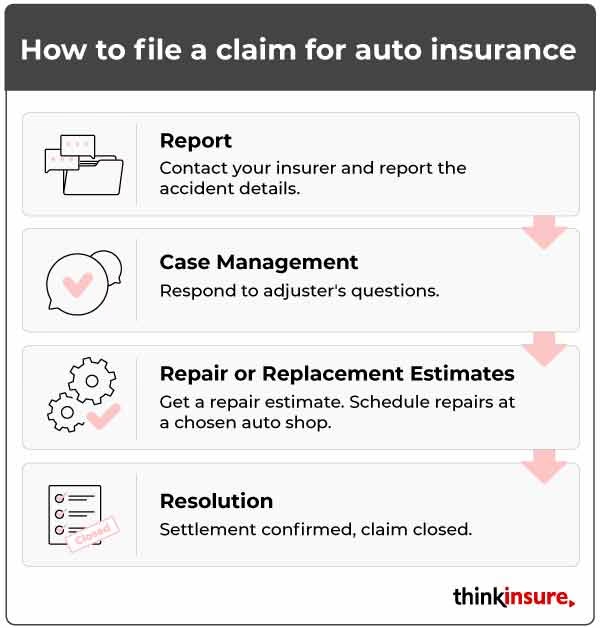

How to Claim on Your Car Insurance After an Accident

Should you find yourself in the unfortunate situation of being involved in a car accident, it is imperative to follow a specific set of steps. Initiating these actions at the scene of the accident can significantly streamline and facilitate a smoother insurance claim process:

- Do not admit fault at the scene. Admitting liability at the accident site could be used against you during the insurance claim process and may lead to unnecessary complications and disputes.

- Ensure everyone's safety. Before proceeding with any other actions, confirm that all individuals involved are uninjured. If anyone is hurt, contact the emergency services (police and ambulance) immediately.

- Exchange contact information. It is vital to exchange full contact details with the other driver(s) involved. This includes their name, address, telephone number, the vehicle's registration number, and, if possible, their insurance policy number.

- Gather evidence. Take as many photographs and videos as you possibly can of the accident scene, the damage to all vehicles involved, and any relevant road conditions. This visual evidence can be invaluable in supporting your claim with the insurance firm.

- Identify witnesses. If there are any witnesses to the accident, endeavour to obtain their contact information. Their independent account of the event can be crucial in establishing fault.

- Note the details. Record the exact location where the accident occurred, along with the precise date and time.

- Police involvement. If the police attend the scene, request a copy of their report and obtain a crime reference number if applicable.

- Notify your insurer promptly. It is essential to inform your insurance provider about the accident as soon as possible, even if you do not intend to make a claim at that moment. This fulfils your policy obligations and can be important for future reference.

Claiming with Different Insurance Types

Claiming Third Party Car Insurance

If you have Third Party insurance and are not at fault for the accident, it is crucial to notify the at-fault driver's insurer about the incident without delay. This allows you to initiate a claim against their policy. The third-party insurer will then be responsible for determining who was at fault for the accident. You can contact the third-party insurance provider in writing, providing a clear and detailed explanation of the situation and outlining precisely what you wish to claim for, such as the cost of vehicle repairs.

Should the insurance company determine that you were at fault for the accident, your Third Party insurance will cover the repair costs for the other driver's vehicle. However, you will be personally responsible for covering the expenses associated with repairing your own car.

Claiming Comprehensive Car Insurance

If you are fortunate enough to have a comprehensive insurance policy, your primary course of action is to report the accident and initiate the claim directly with your own insurance provider. Your insurer will then undertake the process of disputing the claim with the third party's insurance provider. If your insurer is unable to recover the costs from the third-party insurer, it is highly probable that you may forfeit any accumulated no-claims bonuses or discounts you have earned. It is still advisable to pursue a claim through the third party's insurance for any uninsured losses – those expenses not covered by your own policy.

To make a claim under a comprehensive policy, you must contact your insurance provider and adhere strictly to their stipulated procedure. Ensure you retain all evidence of damages and losses incurred. The more photographic and video evidence of the incident you can provide, the greater your likelihood of securing the full coverage to which you are entitled.

Understanding Car Insurance Excess

When you are involved in a car accident and need to make a claim on your insurance, you will typically be required to pay a predetermined amount towards the cost of repairing your vehicle. This agreed-upon contribution is known as the 'excess'. The implementation of excess payments serves as a deterrent against insurance fraud and the submission of spurious claims. The rationale is that individuals who are financially invested in the repair costs are less likely to make non-genuine claims.

The Value of a No-Claims Bonus

A 'no-claims bonus' (NCB) is a valuable incentive offered by most insurance companies to drivers who have maintained a claim-free period for a specified duration. This bonus is instrumental in reducing the overall cost of car insurance and serves as a reward for motorists who are statistically assessed as lower risks. Protecting your no-claims bonus is therefore a significant financial consideration when deciding whether to make a claim.

How Long Do Car Insurance Claims Typically Take?

There is no definitive timeframe for resolving a car insurance claim. The duration can vary significantly, with settlements ranging anywhere from a week to potentially a full year to be resolved. Once your claim has been formally submitted, the primary action you can take is to patiently await the outcome.

Key Takeaways for a Smoother Claim

In the unfortunate event of a car accident, prioritising the immediate well-being of anyone injured and diligently preserving evidence, such as photographs, videos, and witness details, are paramount for a swift recovery and a seamless insurance claim process. Being prepared and informed can make a significant difference during a stressful time.

If you want to read more articles similar to Car Insurance Claims: A User's Guide, you can visit the Insurance category.