17/10/2024

Experiencing a car accident can be a profoundly unsettling event, leaving you not only shaken but also facing the daunting task of assessing the damage to your vehicle. While some minor dents and scratches might be easily repairable, more significant impacts can lead to a far more serious outcome: your car being declared a ‘write-off’ by your insurance provider. This term often conjures images of irreparable wreckage, but the reality is more nuanced, with various categories determining the fate of your vehicle. Understanding what a write-off truly means, how it’s assessed, and what steps you need to take afterwards is crucial for any motorist in the UK.

This comprehensive guide will demystify the world of car insurance write-offs, walking you through the assessment process, the different categorisations, and the implications for both your vehicle and your insurance policy. We’ll also delve into the practicalities of what happens next, from compensation to the potential of buying a written-off car, ensuring you’re well-equipped to navigate this challenging situation with confidence.

- What Does It Mean When Your Car Is a “Write-Off”?

- The Different Car Insurance Write-Off Categories

- What Happens When a Car Is Written Off?

- Am I Still Insured if My Car Is Written Off?

- Should I Buy a Written-Off Car?

- Frequently Asked Questions About Car Write-Offs

- How does my car insurance assess damage after a crash?

- Will my car be written off if the damage doesn't look too bad?

- How is the compensation payment calculated for a written-off car?

- What's the difference between the old Cat C/D and the new Cat S/N?

- Do I lose my no-claims bonus if my car is written off?

- Conclusion

What Does It Mean When Your Car Is a “Write-Off”?

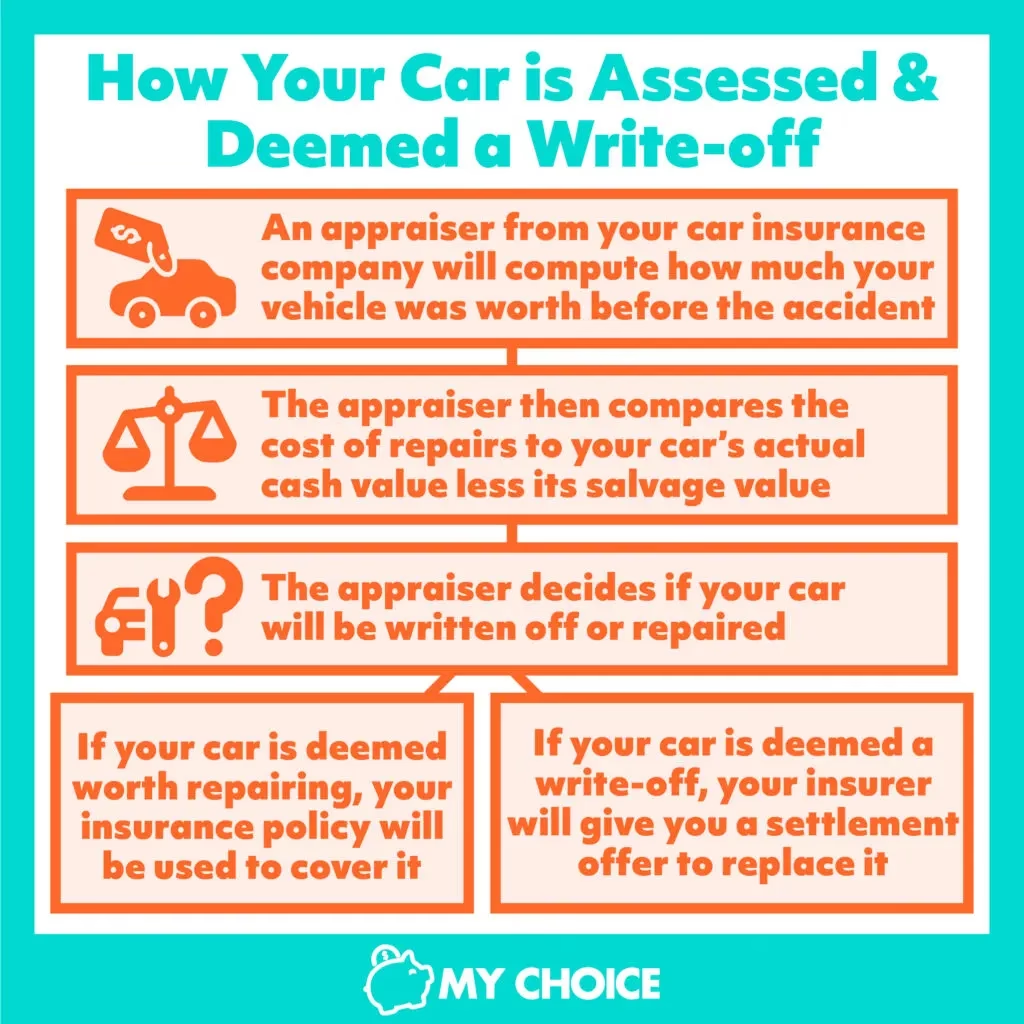

In the simplest terms, if your car is declared a write-off, it means that your insurance company has determined that the cost of repairing the damage it sustained in an accident is economically unviable. This doesn’t always mean the car is physically beyond repair; rather, it implies that the expense of bringing it back to a roadworthy and safe condition would exceed its current market value. Your car insurance provider will meticulously assess the damage and compare the estimated repair costs against the vehicle’s pre-accident value, taking into account factors such as its age, mileage, and overall condition. If the repair costs cross a certain threshold – typically around 50-60% of the car’s market value, though this can vary – it’s likely to be deemed a write-off.

Once a car is declared a write-off, ownership typically transfers to your insurance company. They then take responsibility for disposing of the vehicle, either by crushing it or selling it on for salvage, depending on the severity and nature of the damage. In return, you receive a compensation payment, calculated to reflect the vehicle’s market value at the time of the incident, allowing you to purchase a similar replacement.

The Different Car Insurance Write-Off Categories

Since October 2017, the UK insurance industry has utilised a revised system of four main write-off categories, replacing the older A, B, C, and D system. These categories are crucial as they dictate whether a car can ever be returned to the road and what actions must be taken. The categories are A, B, S, and N, each signifying a different level of damage and salvageability.

- Category A (Scrap Only): This is the most severe category. Vehicles in Category A are so extensively damaged that they are deemed completely irreparable and pose a significant safety risk. The entire vehicle, including any salvageable parts, must be crushed and cannot be used for spares. These cars are never allowed back on the road under any circumstances.

- Category B (Break): While also irreparable and destined for the scrap heap, Category B vehicles differ from Category A in one key aspect: some parts can be salvaged. If your car falls into this category, it means the main structural components are too damaged to be repaired, but certain components – such as the engine, gearbox, or interior fittings – might be safe and suitable for reuse. The vehicle’s shell, however, must be crushed.

- Category S (Structurally Damaged): Previously known as Category C, Category S indicates that the vehicle has sustained significant structural damage. This could include damage to the chassis, suspension, or other load-bearing components. While the damage is severe, Category S cars are repairable and can be returned to the road once professionally repaired and deemed safe. However, due to the structural nature of the repairs, all Category S cars must be re-registered with the DVLA (Driver and Vehicle Licensing Agency) once repaired before they can legally be driven on public roads. This ensures that the DVLA is aware the vehicle was previously a write-off and has undergone significant restoration.

- Category N (Non-Structurally Damaged): Formerly Category D, Category N covers vehicles with significant non-structural damage. This might include extensive cosmetic damage, electrical faults, or problems with mechanical components that are not integral to the car’s structural integrity. While often less severe than Category S, these vehicles still require substantial repairs to be roadworthy. The crucial difference is that Category N cars do not need to be re-registered with the DVLA once repaired, as their structural integrity was not compromised. However, you must still notify the DVLA that your vehicle was written off.

Understanding these categories is vital, as they directly impact whether a vehicle can ever be driven again and the administrative steps involved in getting it back on the road or disposing of it.

| Category | Type of Damage | Repairable? | Parts Salvageable? | DVLA Re-registration Needed? |

|---|---|---|---|---|

| A (Scrap Only) | Extensive, unsafe, beyond repair | No | No | N/A (Crushed) |

| B (Break) | Extensive structural, beyond repair | No | Yes (non-structural) | N/A (Crushed) |

| S (Structural) | Significant structural damage | Yes (with professional repair) | Yes | Yes (mandatory) |

| N (Non-Structural) | Cosmetic, electrical, non-structural damage | Yes (with repair) | Yes | No (but notify DVLA) |

What Happens When a Car Is Written Off?

Once your insurance provider determines your car is a write-off, a series of standard procedures will follow. The primary outcome is that ownership of the vehicle officially transfers from you to the insurance company. In exchange for your car, they will provide you with a compensation payment. This payment is typically based on the market value of your vehicle immediately before the accident occurred. Insurers will consider various factors to determine this value, including the car’s age, its mileage, its overall condition, and any optional extras it might have had. The aim is to provide you with enough funds to replace your written-off vehicle with a similar make, model, and condition on the open market.

For Category A and B write-offs, the process is quite definitive: the car will be scrapped. For Category A vehicles, the entire car is crushed, with no parts allowed to be salvaged. For Category B cars, while the main structure is crushed, a certified breaker can salvage usable parts before the rest of the vehicle is disposed of. Your insurer will generally manage the logistics of getting the vehicle scrapped for you, but there are crucial steps you must take:

- Retain Your Registration Number (Optional): If you have a personalised or cherished registration number that you wish to keep, you must apply to take it off the vehicle before it’s scrapped. This needs to be done through the DVLA.

- Send Your V5C (Log Book) to Your Insurer: You will need to send the vehicle log book (V5C) to your insurance company. However, it is critically important that you keep the yellow ‘sell, transfer or part-exchange your vehicle to the motor trade’ section (section 9) from it. This part serves as your proof that you’ve transferred ownership.

- Inform the DVLA: This is arguably the most important step. You are legally obliged to notify the DVLA that your vehicle has been written off. Failure to do so can result in a hefty fine of up to £1,000, as the DVLA will still consider you the registered keeper and responsible for the vehicle.

If your car falls into Category N or S, the situation is different. While ownership transfers to the insurer, they have the option to sell the vehicle on, either to a third party (often a salvage dealer) or back to you if you express a desire to keep it. This is a common occurrence, particularly for Cat N vehicles where the damage is less severe and easily repairable.

Keeping a Category N or S Vehicle

Should you decide to keep your Category S vehicle, you will need to send your log book to your insurance provider and then apply for a new one from the DVLA. There is typically no charge for this. This new V5C will clearly state that the vehicle was previously a Category S write-off. For Category N write-offs, this re-application to the DVLA for a new log book is not necessary, though you must still inform them that the car was written off.

Am I Still Insured if My Car Is Written Off?

When your car is declared a write-off, your existing insurance policy doesn’t automatically cease. However, its coverage for *that specific vehicle* will change dramatically. If you decide to accept the write-off payment and let your insurer take ownership, your policy for that car effectively ends as far as physical damage cover is concerned. You would then need to arrange new insurance for any replacement vehicle you purchase.

If you choose to keep a Category N or S write-off and intend to repair it, the vehicle will only be insured for road use once the necessary repairs are completed and it is certified as roadworthy. Your insurer will likely require a valid MOT certificate, dated after the incident, to confirm the car's safety and legality for public roads. Furthermore, some insurers might impose a deadline for these repairs and the subsequent MOT; for example, you might have 45 days for a Cat N write-off or 8 weeks for a Cat S write-off before the policy for that specific vehicle is cancelled.

What Happens to Your Policy?

Your overall insurance policy will not be automatically cancelled simply because your car was written off. You retain the ability to cancel your policy at any time. The financial implications for your policy depend on whether the incident was deemed a ‘fault’ or ‘non-fault’ claim:

- Fault Incident: If the accident was deemed your fault, or if your insurer cannot recover their costs from a third party, you typically won’t receive a refund on your policy premium for the remaining term. Your no-claims bonus may also be affected.

- Non-Fault Incident: If the incident was clearly not your fault and your insurer can recover their costs from the responsible party, you would usually receive a pro-rata refund for the unused portion of your premium, and no cancellation fee would be applied. Your no-claims bonus should remain unaffected.

It’s always advisable to discuss the specifics with your insurer once your car has been written off to understand the exact impact on your current policy and future premiums.

Should I Buy a Written-Off Car?

The prospect of buying a written-off car, particularly a Category N or S, can be tempting due to the significant cost savings involved. These vehicles are often sold at a much lower price than their non-written-off counterparts, making them an attractive option for budget-conscious buyers or those with the expertise to undertake repairs themselves. However, it’s crucial to proceed with extreme caution and a thorough understanding of the risks.

If you’re considering purchasing a written-off vehicle, it’s absolutely paramount that it’s a Category N or S. Categories A and B cars are illegal to put back on the road. For Cat N or S vehicles, the key to a successful purchase lies in ensuring the repairs have been carried out to an exceptionally high standard. A poorly repaired write-off can be a death trap, compromising safety and leading to ongoing mechanical and structural issues.

Before committing to a purchase, always ensure the following:

- Proof of Repair: Request detailed documentation of all repairs undertaken, including invoices for parts and labour.

- MOT Certificate: The car must have a valid MOT certificate dated *after* the repairs were completed. This confirms it has passed basic roadworthiness checks, but it’s not a guarantee of the quality of the repairs.

- Independent Inspection: This is perhaps the most critical step. Arrange for an independent vehicle expert or engineer to thoroughly inspect the car before you buy it. They can identify any lingering structural damage, shoddy repairs, or hidden issues that might not be apparent to the untrained eye. This professional assessment is invaluable and can save you significant trouble and expense down the line.

- Insurance Implications: Be aware that insuring a previously written-off car can sometimes be more challenging or expensive. Some insurers might be reluctant to offer cover, or they might charge higher premiums due to the car’s history. Always get insurance quotes before you buy.

- Resale Value: A car with a write-off history, even a repaired Cat N or S, will always have a lower resale value than a comparable vehicle without such a history. Be prepared for this depreciation when you eventually come to sell it.

While buying a written-off car can indeed offer a good deal and save you money upfront, it requires diligent research, professional inspection, and an acceptance of the potential long-term implications. For many, the peace of mind offered by a car that has never been written off outweighs the initial cost saving.

Frequently Asked Questions About Car Write-Offs

Navigating the aftermath of an accident and the complexities of insurance write-offs can raise many questions. Here are some of the most common ones:

How does my car insurance assess damage after a crash?

Your insurer assesses damage primarily by comparing the estimated cost of repairs against the vehicle’s pre-accident market value. They will send an assessor to inspect the car, who will then calculate the repair costs, including parts and labour. If these costs exceed a certain percentage (often 50-60%) of the car’s market value, or if the damage is so severe it falls into Category A or B, the car will be declared a write-off. The assessor also determines which write-off category the vehicle falls into based on the nature and extent of the damage (structural vs. non-structural, irreparable vs. repairable).

Will my car be written off if the damage doesn't look too bad?

Yes, it's entirely possible. Even if the visible damage appears minor, there could be hidden structural issues or complex electrical faults that are very expensive to repair. For example, a seemingly small dent might require extensive re-alignment of the chassis, or a simple impact could have damaged intricate sensor systems. If the cost of these repairs, even for seemingly minor cosmetic or non-structural damage, exceeds the car's market value, it will be declared a write-off (likely Category N or S).

How is the compensation payment calculated for a written-off car?

The compensation payment is designed to reflect the pre-accident market value of your car. Insurers will research recent sales of similar vehicles (same make, model, age, mileage, and condition) in your area. They also take into account any modifications or optional extras that would genuinely increase the car’s value. The goal is to provide you with enough money to buy a direct replacement for your written-off vehicle, not the 'new' price of the car or the amount you paid for it years ago.

What's the difference between the old Cat C/D and the new Cat S/N?

The categories were updated in October 2017 to provide clearer guidance on repairability and safety. The key difference is that the new system explicitly distinguishes between structural damage (Category S) and non-structural damage (Category N), whereas the old Category C and D were based purely on repair cost versus value. Category S now requires mandatory DVLA re-registration, highlighting the importance of structural integrity. The old Category C was superseded by Category S, and Category D by Category N.

Do I lose my no-claims bonus if my car is written off?

Whether you lose your no-claims bonus (NCB) depends on whether the incident leading to the write-off is deemed a 'fault' or 'non-fault' claim. If it's a non-fault incident where your insurer can recover costs from a third party, your NCB should remain intact. However, if it's a fault claim (where you are responsible or your insurer cannot recover costs), your NCB will likely be reduced or lost, unless you have NCB protection in place.

Conclusion

Dealing with a car write-off can be a stressful and confusing experience, but understanding the process and your options can significantly ease the burden. From the moment your insurer assesses the damage to the final compensation payment or the decision to repair a salvageable vehicle, each step is governed by clear, albeit complex, regulations and industry practices. Knowing the difference between a Category A and a Category N write-off, understanding your obligations to the DVLA, and being fully aware of the implications for your insurance policy are all crucial elements in navigating this situation effectively. Whether your car is destined for the scrap heap or has the potential to return to the road, being informed empowers you to make the best decisions for your motoring future.

If you want to read more articles similar to Car Insurance Write-Offs: Your Essential Guide, you can visit the Insurance category.