15/08/2022

Following a car accident, the question of settlement often arises, particularly for parties not directly involved in the collision but who have suffered losses. In the United Kingdom, the process of settling claims after a road traffic incident is governed by specific legal frameworks. This article delves into the intricacies of whether a third party can receive a cash settlement and the factors influencing such a resolution.

- Understanding 'Third Party' in Car Accident Claims

- Can a Third Party Settle in Cash?

- Factors Influencing Cash Settlements

- Advantages of a Cash Settlement for a Third Party

- Potential Pitfalls of Cash Settlements

- Comparison: Cash Settlement vs. Insurer-Managed Repairs

- When to Seek Professional Advice

- Frequently Asked Questions

- Q1: Can I demand a cash settlement from the other driver's insurance?

- Q2: What if the cash settlement offered isn't enough to cover my repairs?

- Q3: Can I settle directly with the at-fault driver without involving insurers?

- Q4: Does accepting a cash settlement mean I can't claim for injuries later?

- Q5: How long does a third-party cash settlement typically take?

- Conclusion

Understanding 'Third Party' in Car Accident Claims

In the context of a car accident claim, a 'third party' typically refers to an individual or entity that is not the policyholder or the driver of the vehicle that caused the accident, but who has sustained damage or injury as a result of the incident. This can include:

- Passengers in either vehicle involved.

- Drivers or occupants of other vehicles not directly involved in the initial impact but affected by it.

- Pedestrians or cyclists who have been injured.

- Property owners whose premises (e.g., walls, fences, street furniture) have been damaged.

The primary party seeking compensation is usually the injured party or the owner of the damaged property. The party from whom compensation is sought is typically the driver or owner of the vehicle deemed at fault, or their insurer.

Can a Third Party Settle in Cash?

Yes, a third party can receive a cash settlement after a car accident, provided they have a valid claim and an agreement is reached with the at-fault party's insurer or directly with the at-fault party if they are uninsured or choose to settle privately. A cash settlement means the third party receives a sum of money directly to compensate for their losses, rather than the insurer carrying out repairs or replacements themselves.

Types of Losses a Third Party May Claim

A third party can claim for a range of losses, including:

- Personal Injury: Compensation for physical and psychological harm, including pain and suffering, loss of amenity, and future medical expenses.

- Property Damage: Costs associated with repairing or replacing damaged vehicles, personal belongings within a vehicle, or property belonging to others (e.g., a homeowner's fence).

- Loss of Earnings: If the accident has prevented the third party from working.

- Other Expenses: Such as travel costs to medical appointments or the cost of hiring an alternative vehicle.

The Process of Settling a Third-Party Claim

The process generally involves the following steps:

- Notification: The third party, or their representative, will notify the insurer of the at-fault driver about their claim.

- Assessment of Loss: The insurer will assess the extent of the third party's damages or injuries. This may involve requesting repair estimates, medical reports, or other evidence.

- Negotiation: Negotiations will take place between the third party (or their legal representative) and the insurer to agree on a fair settlement amount.

- Settlement Agreement: Once an agreement is reached, a settlement agreement is signed, and the cash payment is made.

Factors Influencing Cash Settlements

Several factors can influence whether a cash settlement is offered and accepted:

1. Type of Damage

For minor property damage, such as cosmetic scratches or dents, a cash settlement can be a straightforward way to resolve the claim. The third party can then choose their preferred repairer or decide not to repair the damage at all. However, for significant vehicle damage, insurers might prefer to manage the repairs directly through their approved repair network to control costs and ensure quality.

2. Insurer's Policy and Procedures

Different insurers have varying policies regarding cash settlements. Some may be more amenable to offering cash settlements for property damage, while others might have a strong preference for managing repairs themselves. This is often driven by their agreements with repair networks and their internal cost-management strategies.

3. Third Party's Preference

The third party's preference also plays a crucial role. If a third party wishes to have the repairs carried out by a specific garage, or if they prefer to handle the repairs themselves and receive compensation, they can express this preference to the insurer. If the insurer agrees, a cash settlement can be arranged.

4. Complexity of the Claim

For personal injury claims, cash settlements are the standard method of compensation. The settlement amount is calculated based on the severity of the injury, the impact on the claimant's life, and various legal guidelines. Property damage claims that are straightforward and easily quantifiable are also more likely to result in a cash settlement.

Advantages of a Cash Settlement for a Third Party

A cash settlement can offer several benefits to a third party:

- Choice and Flexibility: The third party has the freedom to choose their own repairer, purchase a different vehicle, or use the money as they see fit.

- Speed: In some cases, a cash settlement can be quicker than waiting for an insurer to arrange and complete repairs.

- Control: It gives the third party more control over the repair process and the quality of work.

Potential Pitfalls of Cash Settlements

While beneficial, cash settlements also carry potential risks:

- Underestimation of Costs: The cash amount offered might not be sufficient to cover the full cost of repairs, especially if unexpected issues arise during the repair process.

- DIY Repairs: If the third party attempts to do the repairs themselves or hires an unqualified person, the quality might be compromised.

- Insurance Implications: If the third party uses the cash to buy a replacement vehicle, they need to ensure it is properly insured before driving it.

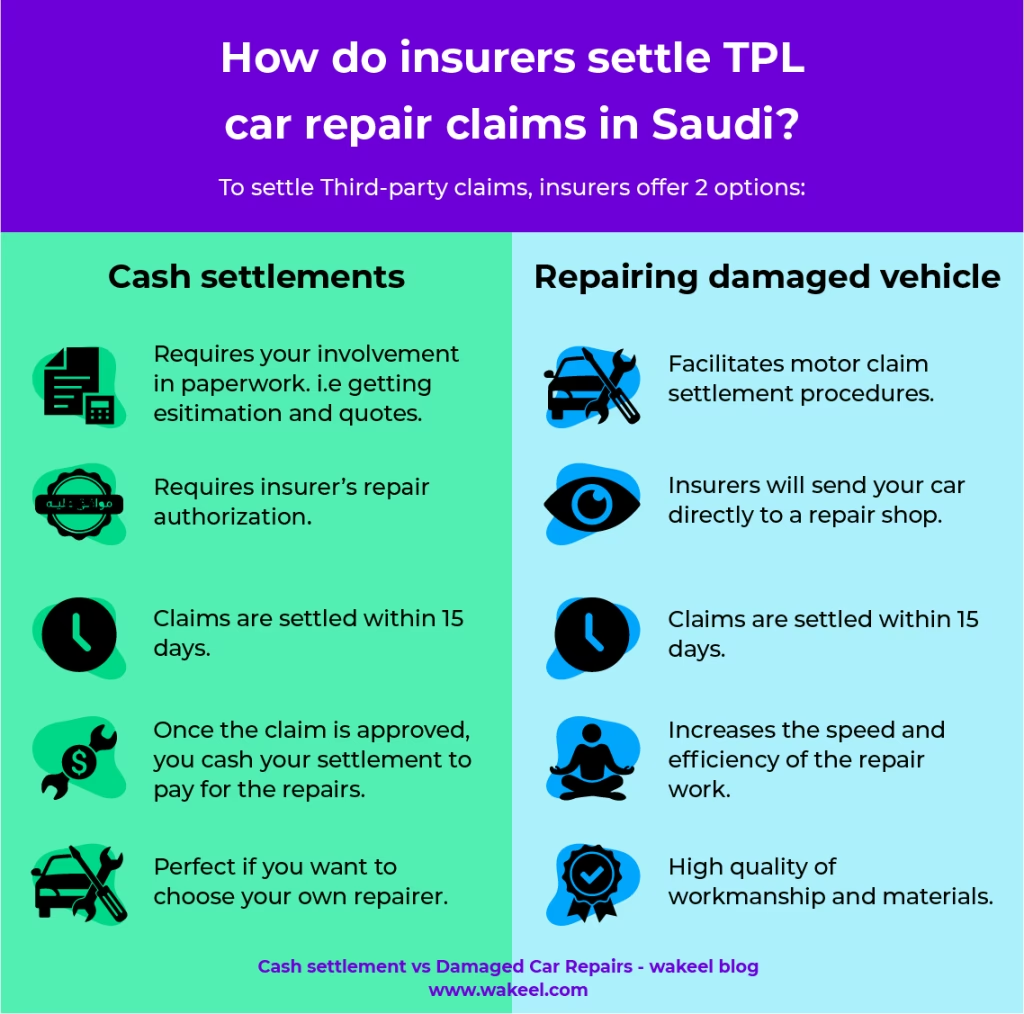

Comparison: Cash Settlement vs. Insurer-Managed Repairs

Here's a brief comparison:

| Feature | Cash Settlement | Insurer-Managed Repairs |

|---|---|---|

| Control over Repairer | High (Claimant chooses) | Low (Insurer's network) |

| Flexibility | High (Use funds as desired) | Low (Repairs are the focus) |

| Speed of Resolution | Potentially faster for payment | Can be slower, dependent on repairer availability |

| Risk of Underpayment | Higher if repair costs escalate | Lower (Insurer covers agreed costs) |

| Administrative Burden | Higher for claimant (managing repairs) | Lower for claimant (insurer handles) |

When to Seek Professional Advice

It is advisable for a third party to seek professional legal advice if:

- The accident involves significant personal injury.

- The property damage is extensive or complex.

- There is a dispute over liability or the amount of compensation.

- The insurer is being difficult or is offering a settlement that seems inadequate.

A solicitor specialising in personal injury or road traffic accidents can help ensure the third party receives fair compensation and understands all their options.

Frequently Asked Questions

Q1: Can I demand a cash settlement from the other driver's insurance?

While you can request a cash settlement, the insurer is not always obligated to agree. They may prefer to manage the repairs through their own network. However, for personal injury claims, cash is the standard form of compensation.

Q2: What if the cash settlement offered isn't enough to cover my repairs?

If you believe the cash offer is insufficient, do not accept it immediately. You can negotiate with the insurer, providing evidence to support your valuation of the damage. If an agreement cannot be reached, seeking legal advice is recommended.

Q3: Can I settle directly with the at-fault driver without involving insurers?

In some minor cases, you might consider a private settlement directly with the at-fault driver. However, this is generally not advisable, especially if there are injuries involved. Insurers provide a level of security and a formal process for claims. Settling privately carries the risk that hidden damage may emerge later, or that the agreed amount is insufficient, with no recourse to the insurer.

Q4: Does accepting a cash settlement mean I can't claim for injuries later?

If you settle only for property damage and later discover you have sustained an injury, it can be very difficult to reopen the claim for injuries if the initial settlement was intended to cover all aspects of the accident. It is crucial to ensure all potential losses, including injuries, are fully assessed before agreeing to any settlement.

Q5: How long does a third-party cash settlement typically take?

The timeframe can vary significantly. Simple property damage claims settled quickly might take a few days to a couple of weeks. Personal injury claims, due to the need for medical assessments and negotiations, can take much longer, sometimes months or even years for complex cases.

Conclusion

In summary, a third party can indeed receive a cash settlement following a car accident in the UK, particularly for property damage and personal injury claims. This offers flexibility and control but also requires careful consideration of potential underestimation of costs. Understanding the process, your rights, and the implications of accepting a cash settlement is vital. When in doubt, always seek advice from qualified legal professionals to ensure you receive appropriate compensation for your losses.

If you want to read more articles similar to Third-Party Cash Settlements After Accidents, you can visit the Automotive category.