11/06/2005

The term 'write-off' or 'totalled' is commonly used when a vehicle has been involved in a significant accident. While these terms are familiar, the intricacies of what constitutes a write-off, how insurers determine it, and what rights you have as a vehicle owner can be confusing. This article aims to demystify the process of a car being declared a total loss in the UK, clarifying the steps involved and your potential recourse.

- What Exactly is a Car Write-Off?

- How Insurers Determine a Write-Off

- What Happens After Your Car is Written Off?

- Protecting Yourself: Gap Insurance and Depreciation Waivers

- Can You Negotiate the Insurer's ACV Settlement?

- What If You Disagree on the ACV?

- Key Considerations After an Accident

- Frequently Asked Questions

What Exactly is a Car Write-Off?

A car is declared a 'write-off' by an insurance company when the cost to repair the damage exceeds a certain threshold relative to the vehicle's pre-accident value. Essentially, it's deemed uneconomical for the insurer to repair the vehicle, and they will instead offer a settlement based on its market value before the damage occurred. This decision isn't based on your preference or the amount you still owe on a loan or lease; it's a purely financial calculation for the insurer.

The insurance policy typically states that the insurer has the right to repair, replace, or rebuild the vehicle rather than paying for the damage. In most cases, they will opt for the most cost-effective solution for their business, which is usually a write-off if the repair costs are high.

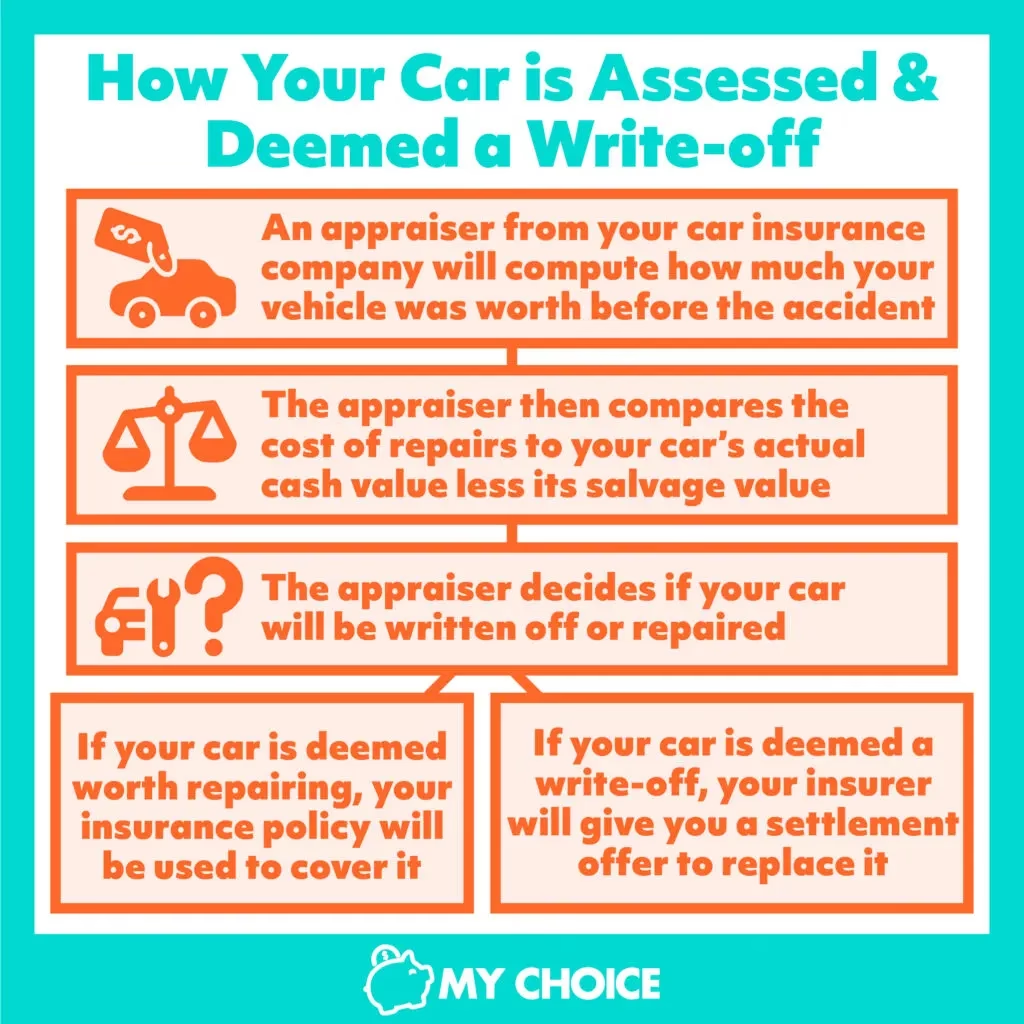

How Insurers Determine a Write-Off

While there isn't a single, universally applied industry standard for determining a write-off, insurance companies generally follow a set of criteria. A vehicle is ordinarily declared a total write-off if it meets one or more of the following conditions:

- Repair Costs Exceed Vehicle Value: The estimated cost of repairs, including parts and labour, surpasses a significant percentage (often 70-80%) of the vehicle's Actual Cash Value (ACV) before the accident.

- Structural Damage: The damage is so severe that the vehicle's structural integrity is compromised, making it unrepairable to a safe standard.

- Airbag Deployment: If the airbags have deployed, this significantly increases repair costs. It often indicates substantial physical or structural damage, making a write-off more likely.

Calculating the Vehicle's Write-Off Value (ACV)

The Actual Cash Value (ACV) is the market value of your car immediately before the accident. Insurers determine this by reviewing comparable vehicles and considering several factors:

| Factor | Consideration |

|---|---|

| Vehicle Type | Make, model, and year all significantly impact ACV. Expect your investment in higher-priced packages to influence ACV, but not always directly proportionally. |

| Customisation | Aftermarket additions or custom equipment can positively or negatively impact ACV, depending on their quality and desirability. |

| Mileage | Unusually low or high mileage can significantly affect the ACV. |

| Condition | The insurer will estimate the pre-accident condition of the interior, exterior, engine, and tyres, seeking comparable vehicles in similar condition. |

| Sale Price | The insurer will review current market prices for similar vehicles sold in your local area. Online marketplaces and dealership listings are often consulted. |

Repair Cost Estimates and Salvage Value

Repair costs, including labour, are usually estimated by a mechanic. Your insurer will typically use their preferred repair shops, but you have the right to choose your own. However, be aware that the insurer may not cover repair costs or labour that exceed their own estimate if you select an independent mechanic.

Salvage value is the amount the insurance company can receive for your car if they decide not to repair it, usually by selling it at auction or to a wholesaler. Unless you specifically ask, they may not disclose this figure. You always have the right to repurchase your written-off vehicle. If you intend to do so, inform your insurer from the outset, as the salvage value will be deducted from your settlement payout.

The basic formula used is:

If (Repair Costs + Salvage Value) > ACV, then the vehicle is a write-off.

If not, the vehicle will typically be repaired.

What Happens After Your Car is Written Off?

The process following a write-off depends on whether you own your vehicle outright or have outstanding finance.

If You Own the Vehicle Outright:

You will receive a settlement cheque for the ACV of your vehicle, minus your policy's deductible. You are free to use these funds as you wish, typically to purchase a replacement vehicle.

If You Have Finance or a Lease Agreement:

The insurance company will usually forward the settlement funds directly to the finance or leasing company to clear the outstanding balance. If the settlement is insufficient to cover the remaining debt, you will be responsible for paying the difference. You may need to negotiate repayment terms with the financial institution or consider rolling the balance into a new car deal.

Protecting Yourself: Gap Insurance and Depreciation Waivers

To mitigate potential financial shortfalls, consider these optional coverages:

- Gap Insurance: This coverage bridges the gap between the ACV settlement and the outstanding balance on your loan or lease. It's particularly useful for newer vehicles that depreciate rapidly.

- OPCF 43 / 43A Endorsement (Removing Depreciation Deduction): If you own a relatively new vehicle (generally less than two years old), this endorsement is highly recommended. It ensures your insurer reimburses you the full purchase price of your vehicle rather than just the ACV, protecting you from immediate depreciation.

Can You Negotiate the Insurer's ACV Settlement?

Yes, you absolutely can and should negotiate your insurer's ACV settlement if you believe it's too low. Insurance companies are businesses, and their initial offer may not always be their best or fairest. Here's how to approach negotiation:

- Don't Accept the First Offer: Treat the initial offer as a starting point for negotiation.

- Challenge Repair/Salvage Estimates: If the insurer's repair cost or salvage price estimates seem unreasonable, obtain your own estimates from reputable mechanics.

- Conduct Comparative Research: Use online resources like AutoTrader, Parkers, or Glass's Guide to research the market value of similar vehicles (same make, model, year, mileage, and condition) in your local area. Be aware that insurers may favour lower-priced comparators.

- Seek Advice: Consult your insurance advisor, a mechanic, or even a legal professional if you feel the need for expert guidance. Friends or family can also offer valuable input on your vehicle's appraisal and negotiation strategy.

Once you have gathered supporting evidence, present a reasonable counteroffer to your claims representative.

What If You Disagree on the ACV?

If you and your insurer cannot agree on a fair ACV, you have the right to initiate an appraisal process as outlined in your policy. This typically involves:

- You and the insurer each appointing an independent appraiser.

- If the appraisers cannot agree, they appoint an umpire to make the final decision.

Be aware that you will need to pay for your own appraiser. While this process can be costly, it can be worthwhile if you strongly believe your vehicle is undervalued. Sometimes, the mere threat of initiating an appraisal can encourage the insurer to make a more favourable offer.

Key Considerations After an Accident

Regardless of whether your car is written off or repaired, it's crucial to:

- Document Everything: Take photographs of all damage, gather police reports, and keep records of all communications with your insurer.

- Report Promptly: Notify your insurance company as soon as possible after an accident.

- Get Multiple Estimates: If your car is being repaired, obtain several written estimates from different reputable repair shops.

- Understand Your Rights: Insurers owe you a duty of good faith. If you feel unfairly treated, explore your options for recourse.

Frequently Asked Questions

- Q1: Can a car be written off if it can still be repaired?

- Yes. A car is written off if the cost of repairs exceeds a significant portion of its pre-accident value, making it uneconomical to repair, even if a repair is physically possible.

- Q2: What happens if my car is written off and I have a loan?

- The insurance payout will typically go directly to the finance company to clear the outstanding loan balance. If the payout is less than the loan amount, you will be responsible for the remaining debt.

- Q3: Can I keep my car if it's written off?

- Yes, you usually have the option to 'buy back' your written-off vehicle from the insurer for its salvage value. The salvage value will be deducted from your settlement payout.

- Q4: Will my insurance premium increase if my car is written off?

- A write-off claim, by itself, should not significantly impact your insurance rates more than a less costly collision claim. However, your claims history overall can affect future premiums.

Navigating the write-off process can be challenging. Understanding your rights, diligently researching your vehicle's value, and being prepared to negotiate are key to achieving a fair outcome when your car is declared a total loss.

If you want to read more articles similar to Understanding Car Write-Offs in the UK, you can visit the Automotive category.