08/10/2017

When is a Car Deemed a Write-Off?

Experiencing a car accident can be a stressful and financially draining event. Beyond the immediate aftermath of dealing with insurance claims, potential demerit points, and the hassle of repairs, there's a possibility that your vehicle might be considered beyond economical repair. This is often referred to as a car being 'written off' or declared a 'total loss'. But how do insurance companies arrive at this decision, and what does it mean for you?

Essentially, a car is written off when the estimated cost of repairs, including parts and labour, approaches or exceeds the vehicle's pre-accident market value. Insurers use a formula that compares the repair costs against the car's actual cash value (ACV) minus its salvage value. If the combined cost of repairs and the salvage value is greater than the car's ACV, the insurer will likely declare it a total loss.

The Write-Off Assessment Process

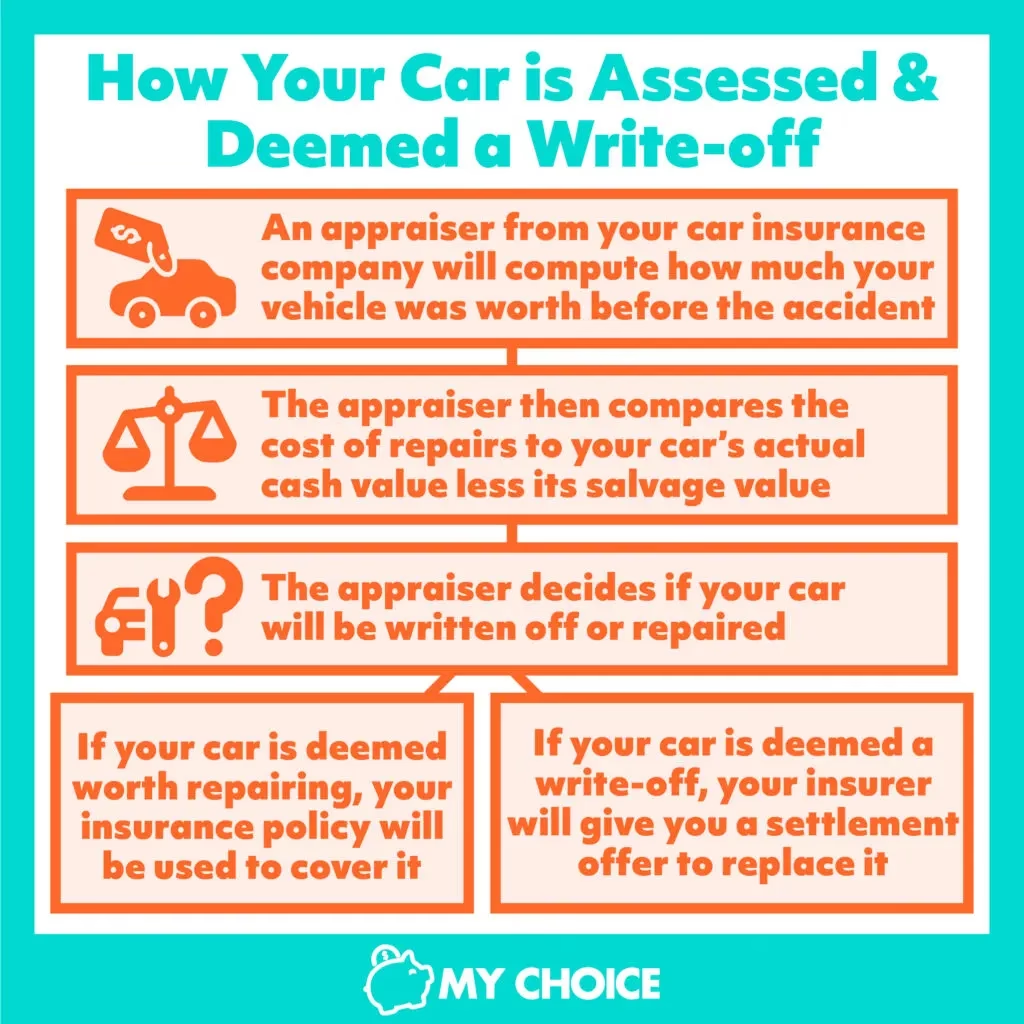

After an accident, your insurance provider will assign an appraiser to assess the damage to your vehicle. This appraiser will meticulously calculate:

- The Pre-Accident Value: This is the market value of your car just before the collision occurred. It's important to note that depreciation plays a significant role here; cars lose value the moment they are driven off the forecourt.

- The Estimated Repair Costs: This includes the cost of all necessary parts, labour, and any associated diagnostic or recalibration services.

- The Salvage Value: This is the amount the damaged vehicle could be sold for, typically for parts or to a specialist salvage yard.

The appraiser then compares the repair costs to the car's pre-accident value. If the repairs are deemed too expensive relative to the car's worth, it will be declared a write-off. This decision is often influenced by factors beyond just visible damage; for instance, the cost of recalibrating sophisticated electronic sensors, common in modern vehicles, can significantly increase repair bills.

What Happens When Your Car is a Write-Off?

If your car is classified as a write-off, your insurance company will typically offer you a settlement cheque. This cheque represents the ACV of your vehicle at the time of the accident, less your policy's deductible. You will then be responsible for purchasing a replacement vehicle.

It's crucial to understand that the settlement amount is based on the car's depreciated value, not its original purchase price. This means the payout might not be enough to buy an identical new car. However, if you have a depreciation waiver on a brand-new vehicle, your settlement might be equivalent to the original purchase price, putting you in a stronger position financially.

Branding of Written-Off Vehicles

Once a car is written off, it's usually given a 'brand'. The two most common brands are:

- Irreparable: This means the vehicle is damaged so severely that it can never be legally driven on the road again. It can only be used for parts.

- Salvage: This indicates that the car can be repaired, but it must undergo a rigorous inspection and be certified before it can be driven on public roads again.

In some cases, if the car has no significant structural or safety issues, you might be allowed to keep the written-off vehicle as part of the settlement. This is often the case with minor damage where the repair cost still exceeds the vehicle's low market value.

Your Options If Your Car is Written Off

Receiving a write-off notification can be disheartening, but you have several options:

1. Accept the Settlement and Purchase a New Vehicle

The most straightforward option is to accept the settlement cheque and use it towards purchasing a replacement car. Remember to budget for potential differences in cost, as the payout may not cover a brand-new equivalent.

2. Dispute the Settlement Amount

If you believe the insurer's valuation of your car is too low, you have the right to dispute it. Gather evidence such as:

- Receipts for recent upgrades or significant repairs (e.g., new engine, transmission, tires).

- Advertisements for similar vehicles in your area with comparable mileage and condition.

- Valuation reports from independent sources.

Present this evidence to your insurer. If you still can't reach an agreement, you can explore arbitration through a neutral third party, as outlined in your policy. Crucially, do not cash the settlement cheque or sign any release documents until you are satisfied with the amount.

3. Argue Against the Write-Off Decision

If you genuinely believe your car is repairable and the insurer has overestimated the repair costs or underestimated the car's value, you can argue against the write-off. You will need to provide a credible, lower repair estimate from a reputable mechanic and evidence that the repairs will restore the car to a safe driving condition.

4. Keep Your Damaged Vehicle

If the car is deemed a write-off but you wish to keep it, you can negotiate with your insurer. They will deduct the salvage value from your settlement cheque, and you will then be responsible for all repairs and any necessary re-branding inspections yourself.

How Insurers Determine Your Car's Value

The valuation of your vehicle by an insurance company is a complex process that considers several factors:

| Factor | Consideration |

|---|---|

| Make, Model, and Year | Newer cars and luxury models generally have higher market values. |

| Odometer Reading | Lower mileage typically indicates a higher value. |

| Engine Type | Engine size and type can influence value. |

| Overall Condition | Interior and exterior condition, including any pre-existing damage or wear and tear. |

| Market Comparables | Values from industry guides (e.g., Red Book), online databases, and local classified ads for similar vehicles. |

The Role of Collision Insurance

Collision insurance is designed to cover the costs of repairing or replacing your vehicle if it's damaged in a collision with another vehicle or object. This coverage is essential for protecting you financially after an accident.

However, it's important to be aware of the limitations:

- Contents Not Covered: Collision insurance typically does not cover personal belongings inside your car.

- Aftermarket Parts: You might have to pay the difference if you opt for replacement parts that are of higher quality or cost than the original parts.

- Repair Location: While you can often choose where to have your car repaired, insurers may only guarantee the quality of work done at their preferred repair shops.

For protection against other risks like theft, vandalism, or natural disasters, you would need comprehensive insurance.

Why Might a Seemingly Minor Damage Result in a Write-Off?

Sometimes, even if the visible damage doesn't appear catastrophic, a car can still be written off. This is often due to the increasing complexity of modern automotive technology. For example:

- Sensor Recalibration: Many vehicles are equipped with advanced safety features and sensors (e.g., for airbags, adaptive cruise control, lane departure warnings) that require specialised recalibration after even minor repairs. The cost and time involved in this process can make repairs uneconomical.

- Structural Integrity: Even if the cosmetic damage is minimal, underlying structural damage can compromise the vehicle's safety and be very expensive to rectify.

Frequently Asked Questions

Q: What is the difference between 'Irreparable' and 'Salvage' branding?

A: An 'Irreparable' vehicle is permanently unfit for the road and can only be used for parts. A 'Salvage' vehicle can be repaired and retuned to roadworthiness after a thorough inspection.

Q: Can I choose my own mechanic if my car is being repaired?

A: Yes, you can usually choose your own mechanic. However, you will need to get an estimate for parts and labour approved by your insurer. Be aware that your insurer may only guarantee the quality of repairs done at their preferred shops.

Q: Is a written-off car a taxable expense?

A: If you used the car for business purposes, the payout from a written-off car might be considered a taxable expense, depending on your specific circumstances and tax regulations. It's advisable to consult with a tax professional.

Q: What if my car was stolen and then recovered damaged?

A: If a stolen car is recovered and the repair costs exceed its market value, it will likely be declared a total loss. This would typically fall under your comprehensive insurance coverage.

Q: Can I negotiate the salvage value if I want to keep my written-off car?

A: Yes, you can negotiate the salvage value with your insurer. Be sure to research the market value for salvage vehicles to ensure you're getting a fair price.

Navigating the process after your car is declared a write-off can be challenging. Understanding your insurer's assessment methods, your rights, and the available options is key to achieving a fair settlement and moving forward after an accident.

If you want to read more articles similar to Car Write-Offs Explained, you can visit the Insurance category.