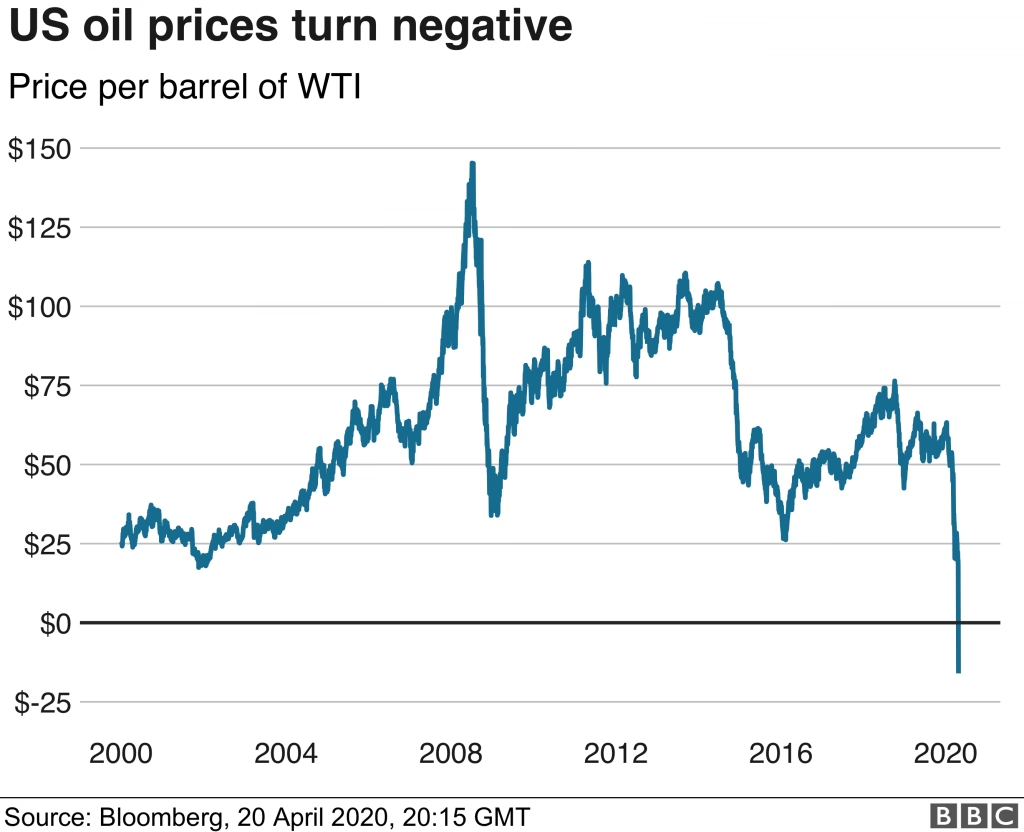

22/09/2008

The global oil market is a tempestuous sea, constantly buffeted by the winds of geopolitical shifts, unexpected natural disasters, and the ever-present ebb and flow of supply and demand. For oil producers, this inherent volatility is not just an abstract market characteristic; it's a direct threat to their profitability and operational stability. To navigate these turbulent waters, companies in the oil and gas sector employ sophisticated risk management strategies, primarily through a practice known as hedging. This article delves into the essential methods oil producers use to shield themselves from the damaging impact of falling oil prices, offering insights valuable to both industry professionals and astute investors alike.

The Imperative of Hedging in the Energy Sector

At its core, hedging is a strategic manoeuvre designed to mitigate risk. It involves taking an opposing position in a financial instrument that is related to the primary asset – in this case, oil or gas. The fundamental principle is to offset potential losses incurred in the physical market with gains in the financial market, or vice versa. For oil producers, hedging is not a speculative gamble but a crucial tool for financial planning and survival. It allows them to stabilise cash flows, ensuring that essential operations, investments in exploration and infrastructure, and shareholder returns are not derailed by sudden price plunges. Without effective hedging, companies can face severe financial distress, impacting everything from job security to national energy supplies.

Key Hedging Instruments Explained

The oil and gas industry relies on a suite of financial instruments to construct robust hedging strategies. The most prevalent among these are futures contracts, options contracts, swaps, and collars. Each offers a distinct approach to managing price risk, with varying degrees of flexibility and cost.

1. Futures Contracts: Locking in Future Prices

A futures contract is a legally binding agreement between two parties to buy or sell a specific quantity of a commodity, such as oil, at a predetermined price on a future date. For an oil producer, this means agreeing today on the price at which they will sell their oil several months or even years down the line.

The primary benefit of a futures contract is price certainty. If an oil producer anticipates a price drop, they can enter into a futures contract to sell their expected output at a current, higher price. This effectively locks in their revenue, providing a safety net against a declining market. However, this certainty comes at a cost: if the market price of oil were to rise significantly above the contracted price, the producer would not benefit from this upward movement, as they are obligated to sell at the lower, pre-agreed rate.

Example: Securing Future Revenue

Imagine an oil producer expecting to extract 100,000 barrels of crude oil over the next six months. Concerned that the market price might fall from its current $80 per barrel, they enter into a futures contract to sell these 100,000 barrels at $78 per barrel in six months.

Scenario A: Market Price Falls

If, in six months, the spot market price for oil has dropped to $70 per barrel, the producer is protected. They still sell their oil at the contracted $78 per barrel, avoiding a significant loss and maintaining their projected revenue stream.

Scenario B: Market Price Rises

Conversely, if the spot market price rises to $90 per barrel, the producer is obligated to sell at $78. While they miss out on the higher market price, their initial hedging strategy successfully protected them from the downside risk they were concerned about. The cost of this protection is the foregone profit from the price increase.

2. Options Contracts: The Right, Not the Obligation

Options contracts offer a more flexible approach to hedging. Unlike futures, options provide the buyer with the *right*, but not the obligation, to buy (a call option) or sell (a put option) a specific quantity of a commodity at a predetermined price, known as the strike price, on or before a specified expiry date. The buyer pays a premium for this right.

This flexibility is a significant advantage. If the market moves favourably, the option holder can choose not to exercise the option and instead participate in the market at the better price. If the market moves unfavourably, they can exercise the option to limit their losses. This selective participation makes options contracts a popular choice for managing risk while retaining the potential to benefit from market upturns.

There are two primary types of options relevant to oil producers:

- Put Options: These give the holder the right to sell an asset at a specific price. An oil producer concerned about falling prices would buy put options, setting a minimum selling price for their oil.

- Call Options: These give the holder the right to buy an asset at a specific price. While less common for producers hedging against falling prices, a company needing to purchase oil for refining might use call options to protect against rising costs.

Example: Protecting Against Price Drops with Puts

Consider the same oil producer, again anticipating selling 100,000 barrels in six months, with the current price at $80. To hedge against a fall, they purchase put options with a strike price of $75, costing them $2 per barrel (a total premium of $200,000).

Scenario A: Market Price Falls Significantly

If the market price drops to $70 per barrel, the producer exercises their put option. They can sell their oil at $75 per barrel, effectively securing a net price of $73 per barrel ($75 strike price minus the $2 premium). This is far better than selling at the market price of $70.

Scenario B: Market Price Rises

If the market price rises to $90 per barrel, the producer lets the put option expire worthless. They then sell their oil on the open market at $90 per barrel. Their net revenue is $88 per barrel ($90 market price minus the $2 premium). In this case, they benefited from the price rise, albeit reduced by the cost of the option premium.

3. Swaps: Exchanging Cash Flows

Swaps are over-the-counter (OTC) agreements between two parties to exchange cash flows over a specified period. In the context of oil prices, a common type is a fixed-for-floating swap. One party agrees to pay a fixed price for a certain volume of oil, while the other party agrees to pay a floating price, typically linked to a benchmark oil index like West Texas Intermediate (WTI) or Brent Crude.

An oil producer concerned about price volatility might enter into a swap agreement where they agree to pay a floating price and receive a fixed price. This effectively guarantees them a minimum revenue per barrel, as the fixed price payment they receive offsets any losses from selling their physical oil at a lower market price.

The advantage of swaps is their customisability; they can be tailored to the specific needs and risk profiles of the parties involved. However, as OTC instruments, they carry counterparty risk – the risk that the other party in the agreement may default on their obligations.

Example: A Fixed Price Guarantee

An oil producer enters into a swap agreement to sell 50,000 barrels per month for a year. They agree to pay the floating market price and receive a fixed price of $77 per barrel.

Scenario A: Market Price is $75

The producer sells their oil at $75. In the swap, they receive $77 and pay the floating $75, resulting in a net gain of $2 per barrel from the swap. Their total revenue for the month is effectively $77 per barrel ($75 from physical sale + $2 from swap).

Scenario B: Market Price is $85

The producer sells their oil at $85. In the swap, they receive $85 but pay the floating $85, resulting in a net of $0 from the swap. Their total revenue remains the market price of $85 per barrel. The swap has effectively capped their revenue at $77 in this instance, a consequence of hedging against a downturn.

4. Collars: Creating a Price Band

A collar is a strategy that combines buying a put option and selling a call option. This creates a price range, or 'collar', within which the producer's effective selling price will fall. The producer buys a put option to set a minimum selling price, providing protection against a price decline. To offset the cost of purchasing the put option, they sell a call option, which caps their potential upside gains.

This strategy is often chosen when a producer wants a degree of downside protection but is willing to forgo some potential upside to reduce the upfront cost of hedging. It's a way to manage risk within a defined band.

Example: A Hedged Price Range

An oil producer wants to hedge 100,000 barrels. They buy a put option with a strike price of $75 (costing $2 per barrel) and sell a call option with a strike price of $85 (receiving $1 per barrel). The net cost of this collar is $1 per barrel ($2 paid - $1 received).

Scenario A: Market Price is $70

The market price is below the put option strike. The producer exercises the put to sell at $75. The call option expires worthless. Their net selling price is $74 ($75 sale price - $1 net premium cost).

Scenario B: Market Price is $80

The market price is between the strike prices. The producer lets the put expire and lets the call expire. They sell at the market price of $80. Their net selling price is $79 ($80 market price - $1 net premium cost).

Scenario C: Market Price is $90

The market price is above the call option strike. The producer sells at the market price of $90. The buyer of the call option exercises it, forcing the producer to sell at $85. Their net selling price is $84 ($85 sale price - $1 net premium cost).

The effective selling price for this producer is between $74 and $84 per barrel, depending on the market price at expiry.

The Role of Financial Institutions

Financial institutions, such as investment banks, commercial banks, and specialised hedge funds, play a pivotal role in the oil and gas hedging landscape. They act as crucial intermediaries, facilitating the execution of futures, options, and swap contracts. These institutions possess the market expertise and infrastructure necessary to manage complex derivative trades.

Furthermore, financial institutions often take on the 'other side' of these hedging transactions. By doing so, they assume the risk that the oil producer is trying to offload, in return for the premiums or fees charged. This allows them to profit from market movements and the management of risk itself. Their involvement is essential for the liquidity and efficiency of the derivatives markets that underpin these hedging strategies.

Why Hedging Matters for Investors

Understanding how oil companies hedge their price exposure is vital for investors looking to make informed decisions in the energy sector. Companies with well-structured and executed hedging strategies are often better equipped to weather market downturns. They tend to exhibit more stable earnings, predictable cash flows, and a reduced risk of financial distress compared to unhedged counterparts.

Consequently, companies that demonstrate a prudent approach to managing price volatility may be viewed as more attractive investments. Their ability to maintain operational continuity and financial stability, even during periods of significant price fluctuation, can translate into more consistent shareholder returns and a stronger competitive position in the long run.

Frequently Asked Questions (FAQs)

Q1: Is hedging a guarantee against all losses?

No. Hedging is a risk management tool, not a foolproof shield. While it significantly reduces exposure to adverse price movements, it does not eliminate all risk. Basis risk (the risk that the price of the hedged commodity differs from the price of the hedging instrument), counterparty risk (for OTC contracts), and the risk of misjudging market movements can still lead to losses.

Q2: Why don't all oil companies hedge 100% of their production?

Hedging involves costs (premiums for options, potential foregone gains with futures) and complexity. Companies must balance the cost of hedging against the perceived risk. Furthermore, some companies may have a bullish view on future oil prices and choose to remain unhedged to capture potential upside. The optimal hedging strategy depends on a company's specific financial situation, risk appetite, and market outlook.

Q3: What is the difference between hedging and speculating?

Hedging is used to reduce or eliminate an existing risk. A producer hedging their output is trying to protect the value of oil they already own or expect to produce. Speculating, on the other hand, involves taking on risk in the hope of profiting from price movements, without necessarily having an underlying physical exposure to manage.

Q4: How often do oil companies review their hedging strategies?

Companies typically review their hedging strategies regularly, often quarterly or annually, and adjust them based on market conditions, production forecasts, and evolving business objectives. Some may also have triggers that prompt immediate review if certain market thresholds are breached.

Conclusion

In the dynamic and often unpredictable world of oil and gas, hedging is an indispensable strategy for producers seeking to maintain stability and profitability. By strategically employing instruments like futures, options, swaps, and collars, companies can effectively manage the inherent risks of price volatility. For investors, understanding these mechanisms provides a clearer lens through which to evaluate the financial health and resilience of energy sector companies, ultimately leading to more informed investment decisions in this critical global industry.

If you want to read more articles similar to How Oil Giants Shield Against Price Crashes, you can visit the Automotive category.