22/07/2012

A car accident, no matter how minor, can leave you feeling shaken and overwhelmed. Beyond the immediate shock, a flurry of questions often arises: Do I have to repair my car? How quickly do I need to act? What are the insurance implications? Navigating the aftermath, especially when dealing with potential personal injury and vehicle damage, can be a daunting task. This article aims to clarify the confusion and provide straightforward answers to common queries about collision repair after an incident on UK roads.

- Do I Have to Repair My Car After an Accident?

- How Long Do I Have to Repair My Car After an Accident?

- Consequences of Delaying Car Repair

- Do I Have to Use the Insurance Money for Repairs?

- What Should I Do If I Can’t Afford Car Repair?

- Can I Drive My Car While It’s Damaged?

- How Long Do Car Repairs Take?

- Can I Repair My Own Car After an Accident?

- Steps to Repair Your Car After a Collision

- Common Mistakes to Avoid After an Accident

- Frequently Asked Questions About Car Accident Repairs

Do I Have to Repair My Car After an Accident?

The necessity of repairing your car after an accident largely depends on two key factors: the extent of the damage and whether your vehicle is still under a finance agreement. If the damage is superficial and doesn't affect the vehicle's roadworthiness or safety, and you own the car outright, you might technically have the option not to repair it. However, this is rarely advisable. Unrepaired damage can significantly reduce your car's resale value, potentially worsen over time, and could even lead to issues with future insurance policies or MOTs.

More critically, if your car is subject to a finance agreement (such as a Hire Purchase, Personal Contract Purchase, or lease), the finance provider legally owns the vehicle until all payments are made. In such cases, you are almost certainly contractually obligated to have the vehicle repaired to its pre-accident condition by an approved workshop. This is because the finance company has a vested interest in maintaining the asset's value. Failing to do so could breach your contract, leading to significant penalties or even repossession of the vehicle.

How Long Do I Have to Repair My Car After an Accident?

Unlike some jurisdictions, there isn't typically a strict, nationwide deadline in the UK for when car repairs must be completed after an accident. However, there are crucial timelines related to reporting the incident and making an insurance claim that you must adhere to. Most insurance policies require you to notify them of an accident 'as soon as reasonably practicable' or within a specific timeframe, often 24-48 hours. Delaying this notification can jeopardise your claim and potentially invalidate your policy.

Once your claim is approved, your insurer will typically authorise repairs. While there might not be an explicit deadline for the repairs themselves, it's always advisable to proceed without undue delay. The sooner you get the repair process underway, the better. Not only will you have your car back sooner, but the details of the incident will still be fresh, which can be helpful if your insurer or repairer has further questions.

The Importance of Prompt Reporting

Even if you're unsure whether you'll claim, it’s generally a good idea to inform your insurance company about any accident involving your vehicle. This is because a third party might later make a claim against you, and if you haven't reported the incident to your insurer, it could cause significant issues. Your policy terms will outline your specific obligations, so always refer to them or contact your insurer directly for clarification. Once a claim is filed, an appointed claims handler or adjuster will guide you through the process, advising on any specific time limits for using your coverage.

Consequences of Delaying Car Repair

While you might be tempted to put off car repairs after an accident, perhaps due to cost or inconvenience, doing so can lead to a multitude of problems. Delaying repairs can result in:

- Worsening Vehicle Damage: Minor damage, if left untreated, can often escalate. A small crack in a bumper could lead to a larger section breaking off, or a slightly misaligned panel could cause water ingress and rust.

- Increased Repair Costs: As damage worsens, so too do the costs associated with fixing it. What might have been a straightforward repair could become much more complex and expensive.

- Compromised Vehicle Safety: Damage to critical components like the chassis, suspension, steering, or braking system can severely impact your car's safety and handling. Driving a compromised vehicle puts you and other road users at risk.

- Impact on Insurance Coverage: Some insurance companies may refuse to cover additional damages that arise directly from delays in undertaking repairs. Furthermore, if you continue to drive a damaged vehicle and it's involved in another incident, your insurer might argue that the prior unrepaired damage contributed to the second incident, potentially affecting your claim.

- MOT Failure: Significant unrepaired damage can lead to your vehicle failing its annual MOT test, making it illegal to drive until fixed.

It’s essential to prioritise repairs that affect your car’s roadworthiness and safety to avoid these pitfalls.

Do I Have to Use the Insurance Money for Repairs?

This question is a common one, and the answer, as mentioned, largely depends on whether you own the vehicle outright or if it's under a finance agreement.

- If You Own the Vehicle Outright: If there's no outstanding finance on your car, and your insurer declares it repairable, they will typically offer a cash settlement for the estimated repair costs. In this scenario, you are generally free to use that money as you see fit. While most people opt to repair the damage to restore the vehicle's value and safety, you could theoretically keep the money. However, be mindful that driving an unrepaired, damaged vehicle could lead to safety issues, MOT failures, and difficulties with future insurance or resale.

- If Your Vehicle is Financed: If your car is on a Hire Purchase, Personal Contract Purchase (PCP), or lease agreement, the finance company holds a vested interest. They will almost certainly require the vehicle to be repaired by an approved garage to maintain its value as their asset. The insurance payout will likely be sent directly to the repairer, or you will be reimbursed upon proof of repair. Failing to repair a financed vehicle can lead to a breach of contract with the finance provider.

What Should I Do If I Can’t Afford Car Repair?

Even with insurance, you might face an excess (the amount you pay towards a claim) or find that the damage isn't covered. If you're struggling to afford the repair costs, consider these options:

- Insurance Claim: If you have comprehensive cover, this is usually the primary route. Your insurer will assess the damage and, if approved, cover the costs minus your excess.

- Third-Party Claim: If the accident was not your fault, the at-fault driver's insurance should cover your repair costs, and you shouldn't have to pay an excess.

- Payment Plans/Financing: Some reputable garages offer payment plans or work with finance companies to help spread the cost of repairs. It's worth asking if this is an option.

- Prioritise Essential Repairs: If full repairs are currently out of reach, focus on addressing critical safety issues first to ensure your car is roadworthy. Cosmetic damage can sometimes wait, but structural or mechanical damage cannot.

- Personal Loan: As a last resort, a personal loan might be an option, but carefully consider the interest rates and your ability to repay.

Can I Drive My Car While It’s Damaged?

The legality and safety of driving a damaged car in the UK depend entirely on the nature and extent of the damage. While a minor scratch or a small dent might be permissible, significant damage can render your vehicle unsafe or illegal to drive under the Road Vehicles (Construction and Use) Regulations 1986. You could face fines, penalty points, or even prosecution if caught driving an unroadworthy vehicle. Here are some examples of damage that would likely make your car unsafe and/or illegal to drive:

- Cracks or chips in the windscreen that obstruct your view or are within the driver's 'swept area' of the wipers.

- Doors, bonnets, or boots that do not latch securely or are liable to open unexpectedly.

- Damage that affects the integrity of the chassis, suspension, steering, or braking system.

- Missing or severely damaged bumpers, lights (headlights, tail lights, indicators), or mirrors.

- Sharp or jagged edges on the bodywork that could injure pedestrians or other road users.

- Leaks of fluids (oil, coolant, fuel) that pose a fire risk or environmental hazard.

- Any damage that obscures your number plates.

If in doubt, it’s always best to err on the side of caution and arrange for your vehicle to be recovered to a repair shop rather than driving it.

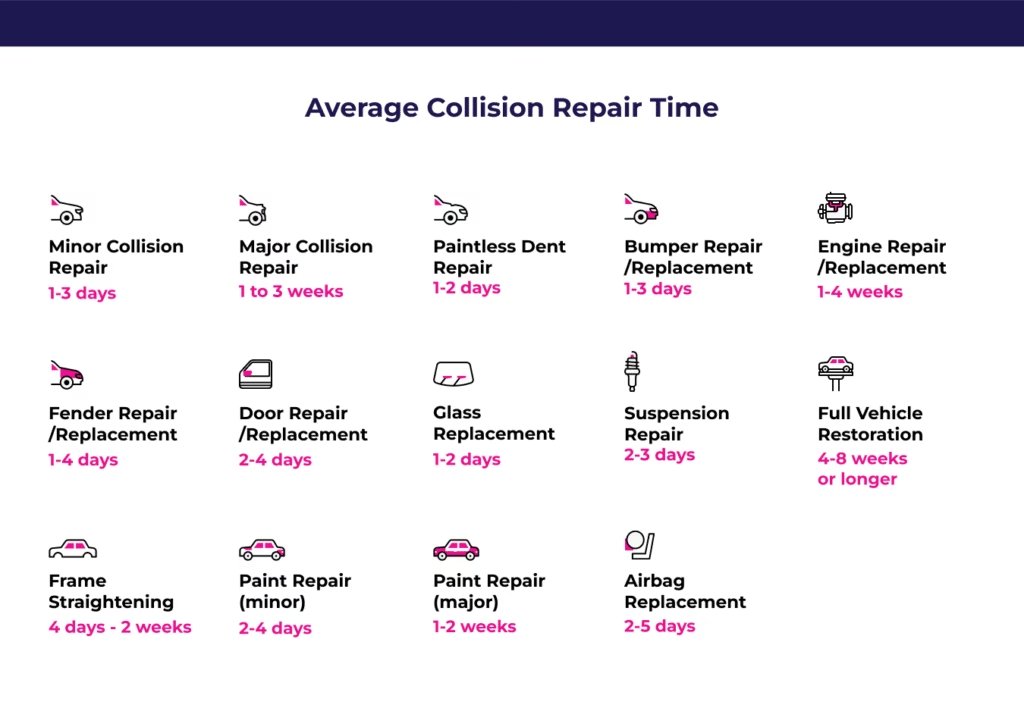

How Long Do Car Repairs Take?

The time required for car repairs after an accident can vary significantly. Factors influencing the repair duration include:

- Extent and Type of Damage: A minor bumper scuff might take a day or two, while extensive structural damage, particularly to the chassis or engine, could take weeks or even months.

- Parts Availability: If specialist parts are needed, especially for classic, imported, or limited-edition vehicles, sourcing them can cause significant delays.

- Vehicle Make and Model: Some manufacturers have more complex repair procedures or require specialised tools, extending the repair time.

- Body Shop Workload: The current workload of the chosen body shop can impact how quickly they can start and complete your repairs.

- Insurance Approval: Delays in your insurer approving the repair estimate can also prolong the process.

The best way to get an accurate estimate of repair time is to take your vehicle to a reputable body shop for a thorough assessment.

Can I Repair My Own Car After an Accident?

While the idea of saving money by performing repairs yourself might be appealing, it's generally not recommended for anything beyond very minor cosmetic damage. If you own your vehicle outright and the damage is genuinely superficial (e.g., a paint scratch that doesn't require panel work), you are legally free to attempt repairs yourself. However, for anything more significant, consider the following:

- Hidden Damage: Professional auto body shops are trained to spot hidden damage, such as bent chassis components or subtle alignment issues, which a DIY enthusiast might miss. Unseen damage can compromise safety and lead to long-term problems.

- Specialised Tools and Skills: Modern vehicles are complex. Repairs often require specialised tools, diagnostic equipment, and expert knowledge that most individuals don't possess.

- Quality and Warranty: Professional repairs come with a warranty on parts and labour, providing peace of mind. DIY repairs offer no such guarantee.

- Insurance and Finance: If your car is financed, you will almost certainly not be permitted to perform repairs yourself, as the finance company requires professional standards. If you plan to claim on your insurance, they will typically insist on approved repairers.

For any damage that affects the structural integrity, safety systems, or mechanical components, always opt for professional repair.

Steps to Repair Your Car After a Collision

Navigating the post-accident repair process can be smoother if you follow a structured approach:

- Assess and Document the Damage: As soon as it's safe to do so, inspect your vehicle. Take clear photographs and videos of all damage from various angles, including the accident scene if possible. This documentation is crucial for your insurance claim.

- Inform Your Insurance Provider: Contact your insurer immediately to report the accident and initiate a claim. Provide them with all the details and documentation you've gathered.

- Get a Repair Estimate: Your insurer may direct you to an approved repairer, or you may have the option to choose your own. Take your car to a trusted body shop or mechanic for a comprehensive damage assessment and an estimate for repairs.

- Body Shop vs. Mechanic for Accident Repairs: It's important to understand the distinction. A body shop (or accident repair centre) specialises in collision damage, including panel beating, paintwork, structural repairs, and chassis alignment. A mechanic typically focuses on the engine, brakes, suspension, and other mechanical systems. For accident damage, a body shop is usually the correct choice, though a mechanic might be needed for specific mechanical issues caused by the impact. Many larger body shops have mechanical repair capabilities too.

- Approve and Schedule Repairs: Once your insurer has approved the repair estimate, schedule the work with the chosen repair centre. Ensure you understand the timeline for repairs and any courtesy car arrangements.

- Collect Your Repaired Vehicle: Before driving away, thoroughly inspect the repairs. Ensure everything looks correct and functions as expected. Don't hesitate to ask questions if something isn't right.

Common Mistakes to Avoid After an Accident

The aftermath of an accident can be stressful, leading to oversight. Avoid these common pitfalls:

- Failing to Document the Damage: Without photos or videos, proving the extent of damage to your insurer can be challenging. Always document everything thoroughly at the scene.

- Delaying the Insurance Claim: As discussed, waiting too long to report an accident can lead to coverage denial or complications with your policy terms. Act promptly.

- Not Understanding Your Policy: Many drivers aren't fully aware of their insurance coverage. Take the time to review your policy documents or speak to your insurer about your coverage for repairs, courtesy cars, and any excesses.

- Choosing the Cheapest Repair Shop Blindly: While budget is a factor, don't compromise on quality. Research reviews, check for certifications (e.g., PAS 125/Kitemark), and ensure the shop offers a warranty on their work.

- Ignoring Hidden Damage: Some damage, particularly to the chassis or suspension, might not be immediately visible. Skipping a professional inspection could leave you with unresolved problems that worsen over time and compromise safety.

- Driving an Unsafe Vehicle: Prioritise safety above all else. Driving a damaged car that doesn't meet road safety standards is not only illegal but extremely dangerous.

- Disposing of the Vehicle Without Insurer Approval: Do not scrap or sell your damaged vehicle without first consulting your insurer, especially if you plan to make a claim.

Frequently Asked Questions About Car Accident Repairs

Q: Do I have to use my insurer's approved repairer?

A: Most insurance policies allow you to use an approved repairer from their network, which often streamlines the process and guarantees the work. Some policies (often called 'choice of repairer' or 'any repairer' policies) allow you to choose your own garage, though you might need to get multiple quotes or your insurer might still want to inspect the vehicle. Always check your specific policy wording.

Q: What if the repair cost is more than the car's value (write-off)?

A: If the cost of repairs, plus salvage value, exceeds the vehicle's market value, your insurer will likely declare it a 'total loss' or 'write-off'. They will then pay you the current market value of your vehicle (minus any excess), and the car will be categorised (A, B, S, or N) depending on the severity of damage and whether it can be safely returned to the road. You will then need to purchase a new vehicle.

A: Making a claim, especially if you were at fault, will almost certainly affect your future insurance premiums. Even if you weren't at fault, a claim can still sometimes lead to an increase, as it signals you've been involved in an incident. Your no-claims discount may also be affected unless it's protected.

Q: What is an excess?

A: The excess is the agreed amount you pay towards a claim before your insurer contributes. It's split into two parts: a compulsory excess set by the insurer and a voluntary excess you choose to reduce your premium. If the accident wasn't your fault and your insurer recovers costs from the third party's insurer, your excess may be reimbursed to you.

Q: Can I get a courtesy car?

A: Many comprehensive insurance policies include courtesy car cover, but the terms vary. Some provide a basic small car for the duration of repairs, while others might offer a temporary replacement vehicle only if you use their approved repair network. If the accident wasn't your fault, you might be entitled to a like-for-like replacement vehicle from the at-fault driver's insurer through a credit hire company.

Dealing with the aftermath of a car accident can be a complex and stressful experience. By understanding your obligations, knowing what to expect from your insurance company, and choosing reputable repair services, you can navigate the process more effectively and ensure your vehicle is returned to a safe and roadworthy condition. Always prioritise safety and consult professionals when in doubt.

If you want to read more articles similar to Car Accident: Do I Need to Repair My Vehicle?, you can visit the Automotive category.