19/02/2010

- Understanding VAT on MOT Testing for Garages

- What is an MOT Test?

- VAT Registration and Liability

- The Taxable Status of MOT Testing

- Can Garages Reclaim VAT on MOT Testing Expenses?

- Potential Complications and Exceptions

- The Consumer's Perspective

- Example Scenario

- Comparison: VAT Registered vs. Non-VAT Registered Garage

- Frequently Asked Questions

- Conclusion

Understanding VAT on MOT Testing for Garages

The question of whether a garage can claim Value Added Tax (VAT) on MOT testing is a common one, often arising from curiosity about the pricing of these mandatory vehicle inspections. For many consumers, the MOT fee is a fixed cost, and the intricacies of business taxation might seem distant. However, for garage owners and those involved in the automotive industry, understanding the VAT implications is crucial for financial planning and compliance. This article delves into the specifics of how VAT applies to MOT testing in the UK, examining the rules from the perspective of the garage performing the service.

What is an MOT Test?

Before we explore the VAT aspect, it's important to clarify what an MOT test is. The MOT (Ministry of Transport) test is an annual test of vehicle safety, road-worthiness, and exhaust emissions. It is a legal requirement for most vehicles over three years old. The test itself is carried out by an authorised MOT test centre, and the price is regulated by the government, although garages can charge up to the maximum allowed fee. The MOT certificate confirms that the vehicle met the minimum acceptable road safety and environmental standards at the time of the test.

VAT Registration and Liability

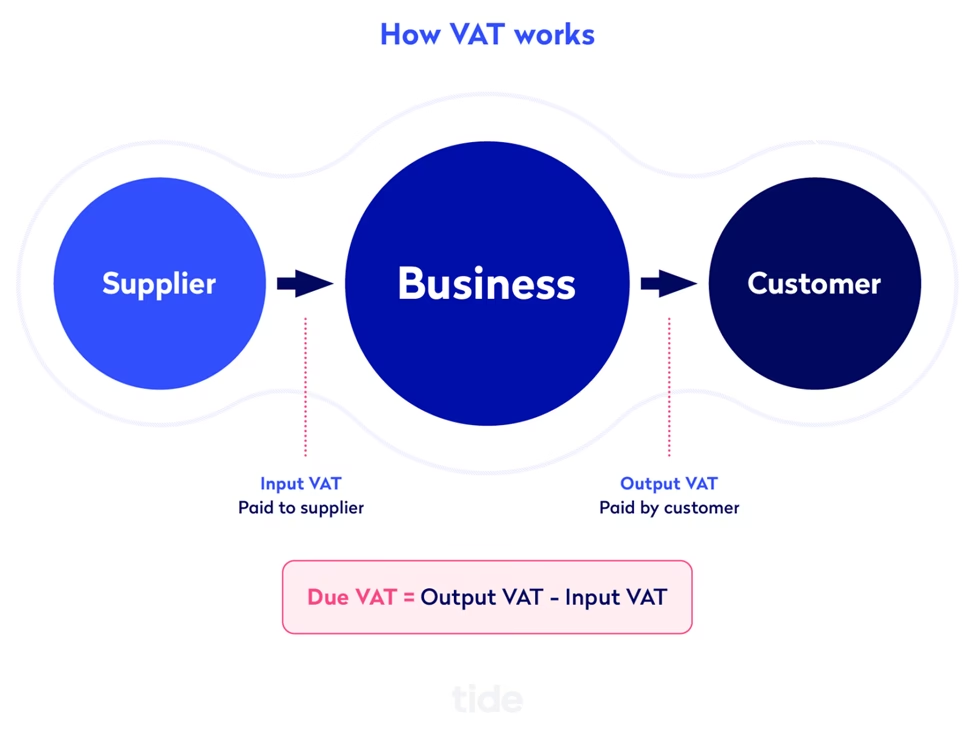

In the United Kingdom, businesses must register for VAT if their taxable turnover exceeds a certain threshold. Currently, this threshold is £90,000 per annum. Once registered, a business is liable to charge VAT on its taxable goods and services and can reclaim VAT on eligible purchases and expenses.

The core of the question lies in whether the MOT testing service itself is considered a taxable supply for VAT purposes. For a business to be able to claim VAT on its expenses, it must be making taxable supplies. If a business's supplies are exempt or outside the scope of VAT, it generally cannot reclaim the VAT it incurs.

The Taxable Status of MOT Testing

According to HMRC (Her Majesty's Revenue and Customs) guidance, MOT testing is generally considered a taxable supply when performed by an authorised MOT centre. This means that if a garage is VAT registered, it must charge VAT on the MOT test fee it charges to its customers. The standard rate of VAT in the UK is currently 20%.

Therefore, when a customer pays for an MOT test at a VAT-registered garage, the fee they pay will include VAT. For example, if the maximum MOT test fee for a car is £54.85, a VAT-registered garage charging the maximum will charge this amount inclusive of VAT. The garage will then need to account for the VAT portion of this fee to HMRC.

Can Garages Reclaim VAT on MOT Testing Expenses?

This is where the nuance comes in. While the MOT test itself is a taxable supply, the ability of a garage to reclaim VAT on expenses related to performing MOT tests depends on how those expenses are incurred and whether they relate to taxable supplies.

A VAT-registered garage can reclaim VAT on most business expenses, provided they are used for making taxable supplies. This includes:

- Equipment: VAT on the purchase or lease of MOT testing equipment (e.g., brake testers, emissions analysers, headlight testers).

- Premises: VAT on rent, utilities, and repairs for the premises where the MOT testing is conducted.

- Staff Costs: VAT on training and development for MOT testers.

- Consumables: VAT on items like stationery, cleaning supplies, and minor tools used in the testing process.

The key principle is 'input tax' (VAT paid on business purchases) can be reclaimed if it relates to 'output tax' (VAT charged on sales). Since MOT testing is a taxable supply, the VAT incurred on expenses directly attributable to performing these tests is generally reclaimable.

Potential Complications and Exceptions

While the general rule is that VAT-registered garages can reclaim VAT on MOT-related expenses, there can be some complexities:

- Mixed Use Expenses: If a garage's expenses are used for both taxable supplies (like MOT tests and repairs) and non-taxable supplies (e.g., certain advisory services or goods not subject to VAT), only the portion of VAT relating to taxable supplies can be reclaimed. This often requires careful apportionment.

- Non-VAT Registered Garages: Garages that are not VAT registered (because their turnover is below the threshold) cannot reclaim any VAT on their purchases and do not charge VAT on their services, including MOT tests.

- Non-MOT Related Expenses: VAT on expenses that are not directly related to the business of providing MOT tests or other taxable supplies (e.g., VAT on entertainment for staff) may not be reclaimable.

- Private Use: If any of the equipment or premises are used for private purposes by the garage owner, the VAT on that portion of the expense is not reclaimable.

The Consumer's Perspective

For the consumer, the ability of a garage to reclaim VAT on its expenses doesn't directly change the price they pay for an MOT test, as the maximum fees are regulated. However, it impacts the garage's profitability. A VAT-registered garage charging the maximum fee will be accounting for VAT on that fee. If they are efficient in reclaiming VAT on their own costs, it can improve their overall financial health, potentially allowing them to invest more in equipment, training, or customer service.

Example Scenario

Let's consider a VAT-registered garage performing a car MOT. The maximum fee is £54.85. The garage charges this amount. This £54.85 includes VAT at 20%. The VAT element is £9.14 (£54.85 / 1.20 * 0.20). The garage must pay this £9.14 to HMRC.

Now, let's say the garage recently bought a new piece of MOT testing equipment for £1,200 plus £240 VAT (£1,440 total). Since this equipment is used to perform taxable MOT tests, the garage can reclaim the £240 VAT on its VAT return.

The net effect on the garage's VAT liability is that they collect £9.14 from the customer for the MOT and can reclaim £240 (or a portion of it, depending on how many MOTs the equipment is used for) on their VAT return. The reclaimable VAT on expenses reduces the overall VAT cost to the business.

Comparison: VAT Registered vs. Non-VAT Registered Garage

To illustrate the difference, consider two garages, one VAT registered and one not:

| Feature | VAT Registered Garage | Non-VAT Registered Garage |

|---|---|---|

| Charge to Customer (Max Fee) | £54.85 (includes £9.14 VAT) | £54.85 (no VAT charged) |

| VAT to HMRC (from MOT) | £9.14 | £0.00 |

| Reclaim VAT on Equipment (£1200 + £240 VAT) | £240.00 (if used for taxable supplies) | £0.00 (cannot reclaim) |

| Net VAT Impact | Collect £9.14, reclaim £240 (reduces VAT cost) | No VAT collected, no VAT reclaimable |

| Overall Cost of Equipment | £1,200 (effectively, after VAT reclaim) | £1,440 (includes non-reclaimable VAT) |

Frequently Asked Questions

Q1: Does the price of an MOT test include VAT?

Yes, if the garage is VAT registered and charges the maximum fee, the price includes VAT. The garage is then obligated to account for this VAT to HMRC.

Q2: Can a garage claim VAT on the MOT testing equipment?

Yes, a VAT-registered garage can generally reclaim the VAT paid on MOT testing equipment, provided it is used for making taxable supplies, such as performing MOT tests.

Q3: What if a garage is not VAT registered?

A garage that is not VAT registered cannot charge VAT on its services and, consequently, cannot reclaim VAT on its business expenses.

Q4: Are there any exceptions to reclaiming VAT on MOT expenses?

Yes, expenses with mixed business and private use, or expenses not directly related to making taxable supplies, may not be fully reclaimable.

Q5: Does the customer pay more if the garage is VAT registered?

No, the maximum charge for an MOT test is regulated. A VAT-registered garage charges the same maximum price as a non-VAT registered one, but the VAT-registered garage accounts for VAT on that fee to HMRC.

Conclusion

In summary, VAT-registered garages in the UK can and should charge VAT on MOT testing fees, as it is considered a taxable supply. Furthermore, they are generally entitled to reclaim the VAT incurred on expenses directly attributable to performing these tests, such as specialised equipment and premises costs. This ability to reclaim input tax is a fundamental aspect of the VAT system, allowing businesses to effectively operate without bearing the VAT burden on their costs. While the consumer pays a regulated fee, the VAT status of the garage impacts its financial operations and its ability to invest in the infrastructure necessary for providing compliant and efficient MOT services. Understanding these financial mechanics provides a clearer picture of how the automotive service industry operates within the UK's tax framework.

If you want to read more articles similar to VAT on MOT Testing: Garage's Perspective, you can visit the Automotive category.