05/08/2025

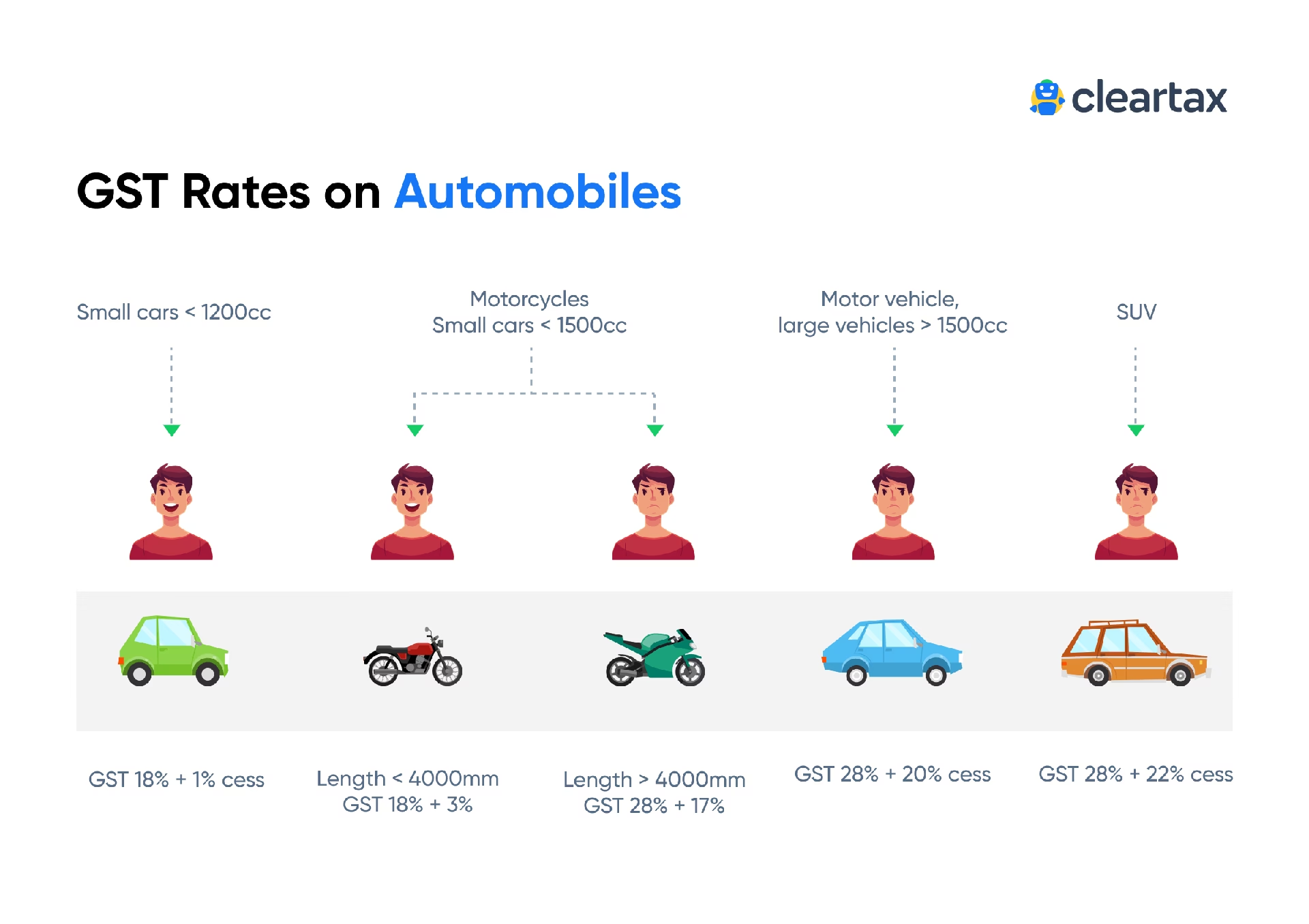

When discussing vehicle taxation, it's crucial to understand the specific tax regime applicable to your region. While the provided information details the Goods and Services Tax (GST) as applied in India, the United Kingdom operates under a different indirect tax system known as Value Added Tax, or VAT. This article will clarify how VAT is applied to vehicles in the UK, offering insights for both private buyers and businesses, and addressing common queries related to car purchases, leasing, and financing under UK tax laws. It's important to note that the GST rates and rules mentioned in the original query are specific to India and do not apply to vehicle transactions in the UK.

- Understanding Value Added Tax (VAT) in the UK

- How VAT Applies to Vehicle Purchases

- UK VAT Rates Relevant to Vehicles

- Calculating VAT on Vehicles

- Reclaiming VAT (Input Tax) on Vehicles for Businesses

- VAT Impact on Vehicle Leasing and Financing

- Other Vehicle-Related Taxes in the UK

- Exemptions and Special Cases for VAT on Cars

- Frequently Asked Questions (FAQs)

- Conclusion

Understanding Value Added Tax (VAT) in the UK

VAT is a consumption tax levied on goods and services in the UK. It is charged at each stage of the supply chain, from manufacturing to the final sale to the consumer. For most goods and services, including vehicles, the standard rate of VAT applies. Businesses registered for VAT can generally reclaim the VAT they pay on purchases that are used for business purposes, a concept similar to the 'Input Tax Credit' in GST systems.

How VAT Applies to Vehicle Purchases

The application of VAT on vehicles in the UK can vary significantly depending on whether the vehicle is new or used, and whether the buyer is a private individual or a VAT-registered business.

New Vehicles

When you purchase a brand-new vehicle from a dealership in the UK, the price advertised typically includes the standard rate of VAT. Currently, this standard rate is 20%. The dealer charges VAT on the full sale price of the vehicle, and as a private buyer, you pay this VAT as part of the purchase price. Businesses that purchase new vehicles for specific commercial purposes may be able to reclaim this VAT, though strict rules apply, particularly for passenger cars.

Used Vehicles (The VAT Margin Scheme)

The VAT treatment of used vehicles is often more nuanced due to the VAT Margin Scheme. This scheme is designed to prevent 'double taxation' of VAT on second-hand goods. Under the Margin Scheme, a VAT-registered dealer only pays VAT on the difference between the price they paid for the vehicle and the price they sell it for (their profit margin), rather than on the full selling price. This is common when dealers buy vehicles from private individuals (who cannot charge VAT) or from other dealers who also sold under the Margin Scheme.

However, if a VAT-registered dealer buys a used vehicle from another VAT-registered business and the original seller charged full VAT (e.g., on a commercial vehicle where VAT was reclaimed), the buying dealer will then charge full VAT on their sale price. This means that a business buying a used car from a dealer might or might not be able to reclaim VAT, depending on how the dealer acquired the vehicle and if they charged VAT on the full value or just the margin.

UK VAT Rates Relevant to Vehicles

Unlike the varied GST rates for different vehicle categories in India, the UK's VAT system is generally simpler for vehicles, primarily applying the standard rate. However, it's useful to see the overall UK VAT rates for context:

| VAT Rate Category | Current Rate | Application |

|---|---|---|

| Standard Rate | 20% | Most goods and services, including new cars, commercial vehicles, repairs, and parts. |

| Reduced Rate | 5% | Some goods and services, e.g., domestic fuel and power, children's car seats. (Not typically directly on vehicles themselves). |

| Zero Rate | 0% | Certain goods and services, e.g., most food, books, children's clothes. (Not applicable to vehicles). |

For vehicles, the 20% standard rate is the most common. There is no 'compensation cess' equivalent in the UK VAT system that adds further percentage points based on vehicle type or engine size, as seen with India's GST.

Calculating VAT on Vehicles

Calculating VAT is relatively straightforward for new vehicles. The ex-showroom price (or list price) includes the manufacturing cost, profit margins, and logistics, with VAT added on top. Registration and insurance fees are typically separate and may have their own VAT implications or be exempt from VAT.

Let's consider an example for a new car:

If a new car is advertised at £24,000 including VAT, and the standard VAT rate is 20%:

- Price before VAT (Net Price): £24,000 / 1.20 = £20,000

- VAT Amount: £20,000 * 0.20 = £4,000

- Total Price (Gross Price): £20,000 + £4,000 = £24,000

For used vehicles under the Margin Scheme, the calculation is more complex as it's based on the dealer's profit. A dealer might sell a car for £10,000 that they bought for £8,000. Their margin is £2,000. VAT at 20% on this margin would be £400. So, the total VAT-inclusive price would be £10,000, but only £400 of that is VAT.

Reclaiming VAT (Input Tax) on Vehicles for Businesses

One of the most significant aspects of VAT for businesses is the ability to reclaim VAT paid on purchases. However, reclaiming VAT on vehicles, especially passenger cars, is heavily restricted in the UK.

General Rule: Blocked VAT on Cars

For passenger cars, businesses generally cannot reclaim VAT on the purchase price if the car is available for private use, even if it's primarily used for business. HMRC considers that most cars have some element of private use, making the VAT non-reclaimable. This is often referred to as 'blocked VAT'.

When VAT Can Be Reclaimed on Vehicles

Despite the general restriction, there are specific scenarios where businesses can reclaim 100% of the VAT on a vehicle purchase:

- Commercial Vehicles: If the vehicle is genuinely a commercial vehicle (e.g., a van, lorry, or pick-up truck with a payload of over one tonne) and is used exclusively for business purposes, the VAT can usually be reclaimed.

- Vehicles for Specific Business Activities: If the vehicle is purchased solely for a specific commercial activity where private use is strictly prohibited and the vehicle is 'stock in trade' or used for 'onward supply'. Examples include:

- Cars bought by a car dealership for resale.

- Vehicles used exclusively as taxis or for private hire (e.g., minicabs).

- Vehicles used exclusively for driving instruction.

- Pool cars that are genuinely available for use by more than one employee and are not ordinarily assigned to a single employee for private use.

- Vehicles used for self-drive hire (car rental businesses).

For a business to reclaim VAT, proper documentation is essential. This includes a valid VAT invoice from the supplier showing the VAT charged, the business's VAT registration number, and clear evidence that the vehicle meets the criteria for reclaimable VAT.

VAT Impact on Vehicle Leasing and Financing

The application of VAT also significantly impacts vehicle leasing and financing arrangements in the UK.

Vehicle Leasing

When a business leases a vehicle, VAT is typically charged on each monthly lease payment. For commercial vehicles, businesses can usually reclaim 100% of the VAT on these lease payments, provided the vehicle is used exclusively for business. For passenger cars, however, VAT on lease payments is generally 50% reclaimable, acknowledging an element of private use, even if the car is primarily for business. If the car is used exclusively for business and no private use is allowed, then 100% of the VAT on lease payments can be reclaimed, but proving this to HMRC's satisfaction can be challenging.

Vehicle Financing (Loans)

For those opting for vehicle loans, VAT does not apply to the loan amount itself, as lending money is generally an exempt supply for VAT purposes. However, VAT may be charged on related services such as processing fees, arrangement fees, or certain insurance products bundled with the finance, depending on their VAT status. The purchase price of the vehicle, whether funded by a loan or cash, will still be subject to VAT as per the rules for new or used vehicles.

Long-Term Cost Efficiency for Businesses

Leasing can often be a more VAT-efficient solution for businesses compared to outright purchase, especially for passenger cars, due to the ability to reclaim 50% of the VAT on lease payments, whereas VAT on purchase is typically 100% blocked. Businesses should carefully consider their specific usage patterns and consult with a tax advisor to determine the most VAT-efficient approach for their vehicle fleet.

Beyond VAT, vehicles in the UK are subject to other taxes that contribute to their overall cost of ownership:

- Vehicle Excise Duty (VED) / Road Tax: An annual tax payable to use a vehicle on public roads. The amount depends on factors like the vehicle's CO2 emissions, fuel type, and age. Electric vehicles currently benefit from zero VED.

- Fuel Duty: A tax levied on petrol, diesel, and other road fuels. This is included in the pump price you pay at the petrol station.

- Company Car Tax (Benefit-in-Kind): If an employer provides an employee with a company car that is available for private use, the employee will pay income tax on the 'Benefit-in-Kind' (BIK) value of the car. The BIK value is calculated based on the car's CO2 emissions and its P11D value (list price including VAT, delivery charges, and accessories). Electric vehicles have significantly lower BIK rates, making them an attractive option for company car schemes.

Exemptions and Special Cases for VAT on Cars

While broad exemptions for vehicle categories like those seen in India's GST (e.g., for electric vehicles or ambulances) are not direct VAT exemptions in the UK, there are specific reliefs and considerations:

- Electric Vehicles (EVs): EVs are subject to the standard 20% VAT rate on purchase. However, they benefit from zero VED and significantly lower Company Car Tax, making them financially attractive. There are also grants available for charging infrastructure.

- Vehicles for Persons with Disabilities: VAT relief is available for adaptations made to vehicles for disabled persons, and in some cases, on the supply of specially designed vehicles for wheelchair users. This is not a general exemption on the vehicle's purchase price but rather a relief for specific modifications or types of vehicles.

- Ambulances: While not VAT exempt, the purchase of ambulances by eligible bodies (e.g., NHS trusts) would typically be for a business purpose, allowing VAT to be reclaimed, provided they meet the definition of a commercial vehicle or are used exclusively for qualifying activities.

Frequently Asked Questions (FAQs)

Q: Can I reclaim VAT on a car I buy for personal use?

A: No, as a private individual, you cannot reclaim VAT on any purchases, including cars, as you are not a VAT-registered business.

Q: Is VAT charged on used cars?

A: Yes, VAT is charged on used cars sold by VAT-registered dealers. However, it's often applied under the VAT Margin Scheme, where VAT is only charged on the dealer's profit margin, not the full sale price. If the dealer was able to reclaim VAT on their purchase, they will typically charge full VAT on their sale price.

Q: How does VAT apply to company cars?

A: If a company buys a car that is available for private use by an employee, the company generally cannot reclaim the VAT on the purchase. If leased, 50% of the VAT on lease payments can usually be reclaimed. The employee will also pay Company Car Tax (Benefit-in-Kind) on the private use of the vehicle.

Q: What about electric cars and VAT?

A: Electric vehicles are subject to the standard 20% VAT rate on purchase and lease payments, just like petrol or diesel cars. However, they benefit from other tax advantages, such as zero Vehicle Excise Duty and very low Company Car Tax rates.

Q: Is VAT charged on car repairs and servicing?

A: Yes, standard rate VAT (20%) is charged on car repairs, servicing, and replacement parts. Businesses can typically reclaim this VAT if the vehicle is used for business purposes.

Q: What's the difference between GST (as in India) and UK VAT?

A: Both GST and VAT are consumption taxes. The key difference lies in their implementation, rates, and specific rules. GST in India has varying rates for different goods and services, including specific vehicle categories and an additional compensation cess. UK VAT primarily uses a standard 20% rate for most goods, including cars, with very few specific vehicle-based rate variations or additional cesses. The input tax credit/reclaim rules also differ significantly, particularly regarding passenger vehicles.

Conclusion

While the Goods and Services Tax framework is a cornerstone of vehicle taxation in India, the UK employs its Value Added Tax system. Understanding how VAT applies to vehicles in the UK is vital for both private buyers and businesses. From the standard 20% VAT on new car purchases to the complexities of the Margin Scheme for used vehicles, and the strict rules governing VAT reclamation for businesses, the UK system is designed to capture consumption tax efficiently. Although UK vehicles don't face the varied 'cess' seen in GST, other factors like Vehicle Excise Duty and Company Car Tax contribute to the overall cost of ownership. Navigating these taxes effectively requires careful consideration, especially for businesses looking to optimise their vehicle fleet costs. Always consult a tax professional for specific advice tailored to your circumstances.

If you want to read more articles similar to Understanding UK VAT on Your Vehicle Purchase, you can visit the Vehicles category.