04/02/2008

Purchasing a new vehicle is often a significant financial commitment, bringing with it the excitement of fresh journeys and modern features. However, the moment your brand-new car leaves the showroom, it begins to lose value. This rapid depreciation can create a substantial financial shortfall if your vehicle is ever declared a total loss due to theft or an accident. This is precisely where GAP insurance steps in, offering a vital layer of financial protection beyond your standard car insurance policy.

Understanding what GAP insurance is, how it functions, and whether it's the right choice for your circumstances is crucial for any car owner. It's designed to prevent you from being left in a difficult financial position, potentially owing money on a car you no longer own. Let's delve into the intricacies of this specialised cover and explore how it can safeguard your investment.

- What Exactly is GAP Car Insurance?

- What Does GAP Insurance Cover You For?

- When is GAP Insurance Needed?

- GAP Insurance vs. 'New Car Replacement' Cover

- Purchasing GAP Insurance: Dealerships vs. Online

- Timing Your GAP Insurance Purchase

- Navigating the GAP Insurance Market: What to Look For

- Understanding Different Types of GAP Insurance

- GAP Insurance Policy Examples & Costs

- Making a Claim on Your GAP Insurance

- What If You're Unhappy? Complaining About Your GAP Insurer

- Frequently Asked Questions About GAP Insurance

What Exactly is GAP Car Insurance?

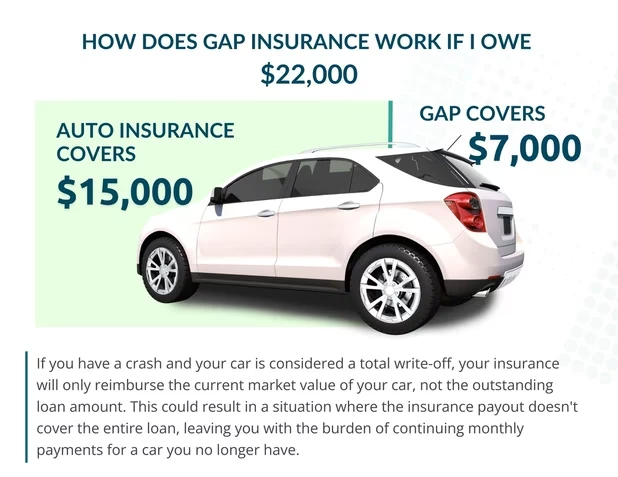

GAP, which stands for Guaranteed Asset Protection, insurance is a supplementary policy designed to work alongside your standard comprehensive car insurance. Its primary purpose is to cover the financial 'gap' that can arise between the amount your main car insurer pays out if your vehicle is stolen or written off, and the original price you paid for it, or the outstanding balance on your car finance agreement.

Imagine you've just bought a car for £15,000, either outright or through a finance agreement. Just a week later, through no fault of your own, the car is stolen or involved in an accident that results in it being written off. Your standard car insurer assesses the vehicle's current market value, which, due to rapid depreciation, might only be £10,000. They issue you a cheque for this amount. This leaves you £5,000 short of what you originally paid. If you financed the car, you could still be liable to your finance company for that £5,000 difference, plus interest, for a car you no longer possess. GAP insurance steps in to cover this exact shortfall, effectively topping up your insurer's payout so you're not left out of pocket or in debt.

What Does GAP Insurance Cover You For?

It's important to clarify that GAP insurance does not replace your car directly, nor does it pay you the full original value of your vehicle. You still need a comprehensive standard car insurance policy for that. Instead, GAP insurance acts as a financial bridge. Depending on the specific type of cover you choose, it will ensure that, after your main car insurer's settlement, you have the necessary funds to either clear any outstanding finance debt or to purchase a replacement vehicle of the same make and model as your original car.

Essentially, it ensures you're not financially disadvantaged by the rapid depreciation of your vehicle. While your comprehensive policy covers the market value at the time of loss, GAP insurance focuses on bridging the difference between that market value and either your original purchase price or the outstanding finance, providing true financial peace of mind.

When is GAP Insurance Needed?

While GAP insurance offers valuable protection, it isn't a one-size-fits-all solution. It's most beneficial in specific scenarios where the financial risk of depreciation is particularly high. We generally recommend considering GAP insurance in the following situations:

- You Used a Large Loan to Buy Your Vehicle: If you've financed a significant portion, or even the entire cost, of your car, GAP insurance can be invaluable. Should your car be stolen or damaged beyond repair, this cover can pay off any outstanding finance on the vehicle. This means you won't be burdened with continuing repayments on a car you no longer own, preventing a potentially devastating financial blow.

- You're Concerned About the Depreciation of Your Vehicle: Cars, especially new ones, notoriously lose value quickly. The quicker your car loses its value, the larger the gap between its purchase price and its market value at the time of a total loss incident. GAP insurance means you'll get more back.

- Your Car is on a Long-Term Lease: For those with long-term rental agreements or leases, a write-off can be particularly problematic. Not only would you be without a car, but you could also face thousands of pounds in early termination fees and remaining lease payments. Lease GAP insurance is specifically designed to protect against these liabilities, covering the outstanding lease payments and any associated charges.

GAP Insurance vs. 'New Car Replacement' Cover

Many standard car insurance policies offer a 'new car replacement' clause, which might seem similar to GAP insurance at first glance. This feature typically means that if your car is less than a year old and is stolen or written off, your insurer will provide a like-for-like replacement. While this is a valuable benefit, it's crucial to understand its limitations and how it differs from the comprehensive protection offered by GAP insurance.

Firstly, new car replacement cover is usually time-limited, often expiring after the first 12 months of ownership. GAP insurance, on the other hand, can often be purchased for a longer duration, sometimes up to five years, though it typically needs to be bought within the first year of owning the car. Some providers even allow you to defer the start of your GAP cover until year two if you wish to rely on your new car replacement policy for the first year.

However, even with new car replacement cover, there can still be a cash shortfall. Your insurer might revert to a cash settlement if a like-for-like replacement isn't available, or if the cost of damage doesn't meet a certain percentage of the car's list price (typically 50-60%). This cash settlement won't necessarily match what you paid or borrowed on finance. Furthermore, if you've financed your vehicle, the finance provider may insist on the full finance amount being paid off in cash, rather than accepting a replacement vehicle from your insurer. Always carefully check the terms and conditions of both your car insurance and your finance agreement to ensure you have adequate cover.

Purchasing GAP Insurance: Dealerships vs. Online

When buying a new car, it's common for dealerships to offer GAP insurance as part of a package of 'extras'. While it's a worthwhile product, the dealership is often not the most cost-effective place to purchase it. You can frequently find far more competitive deals online, directly from insurers, brokers, or through comparison websites.

Regulations are in place to protect consumers from feeling pressured into buying GAP insurance at a dealership. Sales staff must clearly disclose the total premium, policy length, features, benefits, unusual exclusions, and limitations. Crucially, they must also inform you that the product can be purchased elsewhere from standalone providers and whether it's an optional or compulsory add-on. Furthermore, dealerships are prohibited from selling you GAP insurance on the same day they sell you a car. There must be a minimum two-day break, unless you explicitly waive this waiting period. If you do wait, the provider should re-explain the policy details. The decision to waive the waiting period must come from you, not be suggested by the dealership.

Timing Your GAP Insurance Purchase

Unlike standard car insurance, which is typically renewed annually, GAP insurance policies can last for several years, sometimes up to five. However, there's usually a specific window for when you can purchase this cover. Most providers require you to buy GAP insurance within the first year of owning your car, even if you opt to defer the cover's activation until the second year. This 'window' can vary between providers, so it's always wise to check individual policy terms.

Just like with standard car insurance, shopping around for GAP insurance can lead to significant savings. Comparing policies online allows you to find the cheapest deal that meets your needs. When evaluating different policies, pay close attention to the following key features:

- Length of the Policy: How many years will the cover last?

- Excess: What is the amount you'll need to pay towards a claim?

- Significant Exclusions: Are there any specific scenarios or vehicle types that aren't covered?

- Value of Your Vehicle: Ensure the policy's maximum cover level is appropriate for your car's value.

- How to Claim: Understand the claims process and required documentation.

- Cancellation Policy: Know how to cancel your policy if you no longer need it.

Understanding Different Types of GAP Insurance

The GAP insurance market offers a variety of products, each tailored to slightly different needs. Understanding these distinctions is key to choosing the best policy for your circumstances:

Finance GAP Insurance

This is one of the most common and basic forms of GAP cover. It's designed to pay off any outstanding loan payments on your car if it's written off or stolen and not recovered. It ensures you're not left making repayments on a vehicle you no longer possess. However, it typically won't cover negative equity from a previous car loan.

Negative Equity GAP Insurance

If the amount you borrowed to finance your car is higher than the car's actual cost, this extra sum is known as 'negative equity'. This often occurs if you part-exchanged a previous vehicle before fully paying off its finance, transferring the remaining debt to your new car. A standard Finance GAP insurance payout usually won't cover this older debt. Negative Equity GAP Insurance, however, is specifically designed to cover this shortfall, ensuring all your outstanding finance is cleared.

Vehicle Replacement GAP Insurance

Rather than just bridging the gap to your original purchase price, Vehicle Replacement GAP cover aims to bridge the distance between your car insurance payout and the cost of replacing your vehicle with a brand new one of the same make, model, and specification. This is particularly useful for those who want to ensure they can afford to replace their car with an equivalent new model, rather than just recovering the original purchase price.

Return to Value GAP Insurance

Similar to 'Return to Invoice' GAP insurance, this policy pays the difference between your car insurance settlement and the value of the vehicle when it was first purchased. This could prove useful if you bought the car second-hand, or you've had the vehicle for a long time.

Lease GAP Insurance

If you've leased your car rather than buying it outright, Lease GAP insurance is essential. Should your leased vehicle be written off or stolen, this policy helps you pay off the remainder of your lease contract and any additional fees that might apply for early cancellation of the lending agreement. It protects you from substantial financial penalties associated with breaking a lease early.

GAP Insurance Policy Examples & Costs

To give you an idea of typical costs and coverage elements, here are example figures for Vehicle Replacement and Return-to-Invoice GAP policies for various brand new cars, gathered from prominent online providers. These tables also highlight key aspects of the cover provided.

Vehicle Replacement GAP Cover (Examples)

| Provider | Citroen C3 - £13,995 | Mazda 3 - £22,505 | BMW 1-Series - £27,719 | Audi A5 Coupe - £37,935 | Amount towards excess | Maximum cover level | Cover available for (years) | Max. age of vehicle (years) | Max. value of vehicle |

|---|---|---|---|---|---|---|---|---|---|

| ALA | £198 | £240 | £266 | £347 | £250 | £50,000 | 1-4 | 7 | £125,000 |

| Car2Cover | £179 | £199 | £229 | £259 | £250 | No upper limit | 1-4 | 1 | £125,000 |

| Direct Gap | £189 | £249 | £285 | £308 | £1,000 | £50,000 | 1-5 | 9 | £75,000 |

| Total Loss Gap | £149 | £168 | £218 | £235 | £250 | No upper limit | 2-5 | 4 | £50,000 (online; higher by phone) |

Prices collected from company websites in July 2023. These are for three years cover for a brand new car bought on finance from a franchised dealer. The driver uses the car for domestic, social and pleasure purposes as well as commuting to one place of work. Always check policy wording before purchase for full details.

Return-to-Invoice GAP Cover (Examples)

| Provider | Citroen C3 - £13,995 | Mazda 3 - £22,505 | BMW 1-Series - £27,719 | Audi A5 Coupe - £37,935 | Amount towards excess | Maximum cover level | Cover available for (years) | Max. age of vehicle (years) | Max. value of vehicle |

|---|---|---|---|---|---|---|---|---|---|

| ALA | £168 | £187 | £238 | £295 | £250 | £50,000 | 1-4 | 10 | £125,000 |

| Car2Cover | £149 | £174 | £199 | £227 | £250 | No upper limit | 1-4 | 10 | £125,000 |

| Click4Gap | £221 | £224 | £252 | £324 | £250 | £50,000 | 3-4 | 7 | £75,000 |

| Direct Gap | £139 | £203 | £238 | £261 | £1,000 | £50,000 | 1-5 | 9 | £75,000 |

| Gapinsurance.co.uk | £144 | £165 | £197 | £197 | £250 | No upper limit | 1-4 | 9 | £100,000 |

| Gapinsure.com | £194 | £257 | £293 | £402 | £500 | No upper limit | 2-3 | 9 | £125,000 |

| Motoreasy | £134 | £155 | £192 | £235 | £1,000 | £50,000 | 2-4 | 9 | £75,000 |

Prices collected from company websites in July 2023. These are for three years cover for a brand new car bought on finance from a franchised dealer. The driver uses the car for domestic, social and pleasure purposes as well as commuting to one place of work. Always check policy wording before purchase for full details.

Making a Claim on Your GAP Insurance

The process of claiming on your GAP insurance typically begins once your primary car insurer has offered their settlement for your vehicle. Before you initiate the claim, it's vital to review your GAP insurance policy's terms and conditions. Look for any specific time limits for submitting your claim, ascertain your excess amount, and prepare all the necessary information they will require.

A critical piece of advice is to speak to your GAP insurer before you accept any settlement offer from your main car insurance provider. Many GAP providers stipulate that you must contact them prior to agreeing to a claim from your primary insurer. This ensures that the process aligns with their requirements and avoids any potential complications.

If your GAP insurance policy includes cover for outstanding finance, it's worth discussing with them how any remaining loans will be settled and whether the payment will be made directly to your finance company on your behalf. This streamlined process can significantly reduce your administrative burden during an already stressful time.

What If You're Unhappy? Complaining About Your GAP Insurer

Should you find yourself dissatisfied with how your GAP insurer handles your case, or if they fail to address your concerns in a fair and timely manner, do not hesitate to complain. Details on how to lodge a formal complaint should be clearly outlined in your policy document. Always follow the insurer's internal complaints procedure first, as this is often the quickest way to resolve issues.

If you have exhausted the insurance company's complaints procedure and your claim or complaint remains unresolved, you have the right to contact the Financial Ombudsman Service (FOS). The FOS is an independent service that helps resolve disputes between consumers and financial businesses. You typically have a six-month window from the time you reach a 'deadlock' with your insurer (i.e., they send you a final response to your complaint) to make a complaint to the FOS.

Frequently Asked Questions About GAP Insurance

Can you get GAP insurance for a used car?

Yes, absolutely. While GAP insurance is most commonly associated with new cars due to their rapid initial depreciation, you can certainly obtain GAP cover for a used car. The principle remains the same: it covers the difference between your comprehensive insurer's payout and the original purchase price or outstanding finance. However, it's worth noting that new cars typically depreciate faster in their first few years than used cars. Therefore, while beneficial, the 'gap' for a used car might be smaller or develop at a different rate compared to a brand new vehicle.

A GAP insurance premium is the cost you pay for your GAP insurance policy. Like any insurance premium, it's the fee charged by the insurer for providing you with the agreed-upon coverage. The premium amount can vary significantly based on several factors, including the type of GAP insurance you choose (e.g., Finance, Vehicle Replacement), the value of your vehicle, the length of the policy, and the specific provider. It's a one-off payment for the entire policy term, unlike standard car insurance which is typically paid annually or monthly. It's important to remember that for your GAP insurance to pay out, you must maintain a fully comprehensive standard car insurance policy. GAP insurance will only activate if your car is declared a total loss (stolen and not recovered, or written off) by your primary insurer.

In conclusion, while the thought of your car being stolen or written off is never pleasant, understanding the financial safeguards available can provide significant comfort. GAP insurance serves as a vital safety net, protecting your investment and ensuring you're not left in a precarious financial situation due to vehicle depreciation. By carefully considering your individual circumstances and exploring the various types of cover available, you can make an informed decision to protect your automotive future.

If you want to read more articles similar to Bridging the Gap: Your Guide to Car Insurance, you can visit the Insurance category.