10/05/2012

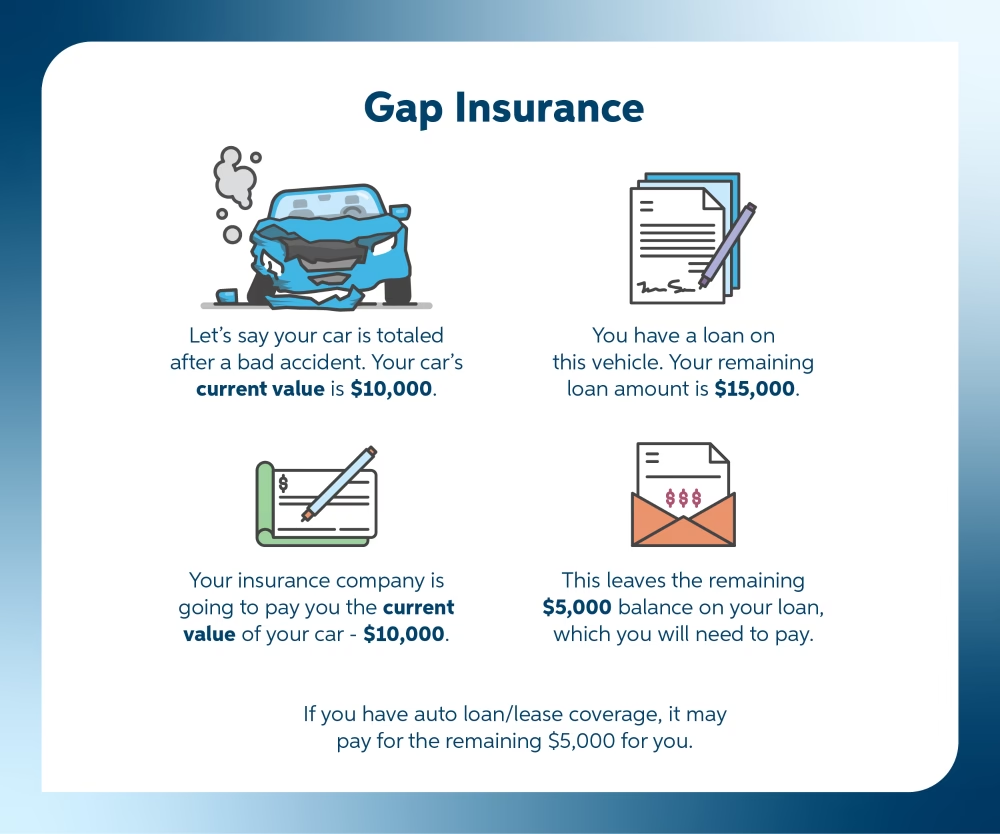

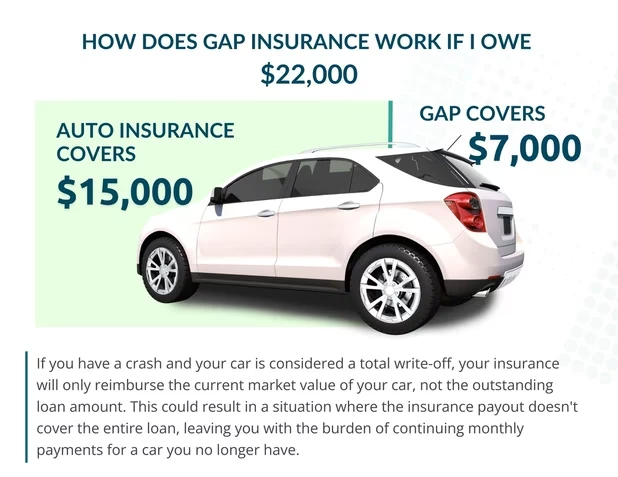

In the unfortunate event that your vehicle is declared a total loss due to theft, accident, fire, or flood, your standard motor insurance policy will typically pay out its current market value. This payout, while based on the vehicle's value at the time of the incident, often falls short of what you originally paid for the car or the outstanding balance on your finance agreement. This is where Guaranteed Asset Protection (GAP) insurance steps in, acting as a crucial financial safety net. GAP insurance bridges this gap, ensuring you're not left out of pocket. This article will guide you through understanding GAP insurance, how to contact providers, and the process of making a claim, with a particular focus on important policy details.

What is GAP Insurance?

GAP insurance, or Guaranteed Asset Protection insurance, is designed to cover the shortfall between your car insurer’s payout and either the original price you paid for your vehicle, the amount you still owe on a finance or lease agreement, or the cost to replace your car with one of the same standard. Essentially, it protects you against the rapid depreciation of your vehicle from the moment you drive it off the forecourt. While your motor insurer will compensate you for the vehicle's market value at the time of the loss, this value is almost always less than the initial purchase price or the remaining finance balance, especially in the early years of ownership.

Why You Might Need GAP Insurance

The primary reason to consider GAP insurance is to mitigate the financial impact of vehicle depreciation. New cars, in particular, can lose a significant percentage of their value within the first few years. If your car is stolen or written off, and your insurer pays out its current market value, you could face a substantial deficit. This deficit could mean you have to settle your finance agreement with money you don't have, or you won't be able to afford a comparable replacement vehicle. GAP insurance provides this essential cover, offering peace of mind and financial stability.

Types of GAP Insurance

There are several types of GAP insurance policies available, each offering slightly different benefits:

Invoice GAP Insurance

This policy covers the difference between your insurer's payout and the price you originally paid for the vehicle, as shown on your invoice. It's particularly beneficial if you bought your car outright or if your finance agreement has a low loan-to-value ratio.

Replacement GAP Insurance

If your car is written off, this policy will cover the cost of a brand-new replacement vehicle of the same make, model, and specification as your original car. This is ideal if you want to ensure you can replace your vehicle with an identical new one, regardless of price fluctuations.

Contract Hire GAP Insurance

For those who lease their vehicles, this policy covers the shortfall between your insurer's payout and the amount you owe to the leasing company to settle your contract early. It prevents you from being liable for outstanding lease payments.

Top-Up GAP Insurance

This is a variation that aims to top up your motor insurance payout by a percentage (often 25%), up to a certain limit. However, it's important to be aware of how these policies handle market value, as discussed below.

Understanding Market Value Clauses

A critical aspect of GAP insurance policies, particularly concerning payouts, is the presence of 'Market Value' clauses. It's crucial to understand these to avoid disappointment during a claim. Inferior GAP insurance policies often incorporate Market Value clauses, which can significantly reduce the amount you receive.

How Market Value Clauses Work

A common Market Value clause relates to the payout from your primary motor insurer. If your motor insurer's payout is less than what the GAP insurer's preferred valuation guide (e.g., Glass's Guide) states the car was worth, the GAP insurer may not cover the full difference they perceive as an underpayment by your motor insurer. This can lead to a reduced payout.

Furthermore, if you purchased a used car, a Market Value clause in an Invoice or Replacement GAP policy might allow the GAP insurer to revalue your vehicle at the time of purchase. If their valuation guide indicates the car was worth less than you paid, they may not cover the perceived 'overpayment' you made.

Policies to Avoid

Policies incorporating one or more Market Value clauses should generally be avoided. For instance, Top-Up GAP insurance policies, to the best of our knowledge, typically include a Market Value clause to prevent policyholders from 'profiting' from a write-off. If your motor insurance payout exceeds the 'Market Value' of your vehicle at the time of the claim (as defined by a guide like Glass's Guide), the Top-Up policy will pay out 25% of the Market Value, not 25% of the higher motor insurance payout. Policies that have dropped Market Value clauses from their Contract Hire, Invoice, and Replacement GAP offerings are generally more favourable.

How to Make a Claim on Your GAP Insurance Policy

Making a claim on your GAP insurance policy is designed to be a straightforward process, allowing you to focus on getting back on track. The general steps involved are:

- Notify Your Motor Insurer: First, you must report the incident (theft, accident, etc.) to your standard motor insurance provider. They will assess the damage or loss and determine if the vehicle is a total loss.

- Receive Settlement Offer: Once your motor insurer agrees the car is a total loss, they will make a settlement offer based on the vehicle's market value at that time.

- Contact Your GAP Insurer: With the settlement offer from your motor insurer in hand, you should then contact your GAP insurance provider. You will typically need to provide them with the settlement offer letter from your motor insurer, along with proof of your original purchase price or finance agreement details.

- GAP Insurer Assesses and Pays: The GAP insurer will review your claim and the documentation. If valid, they will pay out the difference between your motor insurer's settlement and the original purchase price, outstanding finance, or replacement cost, as per your policy terms.

It's essential to follow the specific claims procedure outlined in your GAP insurance policy documents. If you have any questions during this process, don't hesitate to contact their expert advisors.

How Do I Contact GAP Insurance?

If you need to contact your GAP insurance provider, the best course of action is to refer to your policy documents. These documents will contain all the necessary contact information, including:

- Customer Service Phone Number: For direct assistance and to discuss your policy or claim.

- Email Address: For sending documentation or making enquiries in writing.

- Website: Many providers have online portals where you can manage your policy, make claims, or find FAQs.

- Postal Address: For sending physical mail or formal documentation.

Most providers emphasize their commitment to helping you find the right policy and assisting with claims. If you're unsure about who your provider is, check your original purchase documents or your finance agreement. Many GAP insurance policies are sold alongside vehicle purchases, so the dealership or finance company may also be able to direct you.

Should You Buy Car GAP Insurance Online?

Purchasing GAP insurance online can be a convenient and competitive option. Many reputable providers offer their policies directly through their websites, allowing you to compare quotes and select the cover that best suits your needs. When buying online, ensure you are dealing with a regulated and trustworthy provider. Look for companies that are authorised and regulated by the Financial Conduct Authority (FCA) in the UK. Reading customer reviews and understanding the policy terms and conditions thoroughly before purchasing are crucial steps.

Frequently Asked Questions

What happens if my car is stolen or written off?

If your car is stolen or written off, your standard motor insurer will pay out its market value. GAP insurance then covers the difference between this payout and what you originally paid for the car, or what you owe on your finance, helping to avoid a financial shortfall.

What is a Market Value Clause?

A Market Value Clause in a GAP policy can reduce your payout. It might mean the GAP insurer uses a valuation guide to determine the car's worth, potentially leading to a lower payout if their valuation differs from your motor insurer's payout or your original purchase price.

How do I make a claim?

After your motor insurer has settled your claim for a total loss, contact your GAP insurer with your settlement offer. They will then process your claim based on your policy terms.

Is GAP insurance worth it?

GAP insurance can be very valuable, especially for new cars that depreciate quickly or if you have a finance agreement. It protects you from significant financial loss in the event of a total loss, providing essential peace of mind.

Can I get GAP insurance if I bought my car used?

Yes, you can typically get GAP insurance for a used car. However, be particularly mindful of Market Value clauses, as they can affect how a used car is valued at the time of purchase for policy purposes.

What if my motor insurer's payout is higher than what I owe?

GAP insurance only covers the shortfall. If your motor insurer's payout is sufficient to cover your outstanding finance or the cost of replacing your vehicle, you will not receive a payout from your GAP insurance, as there is no gap to cover.

In summary, understanding GAP insurance, its types, and the implications of policy clauses like Market Value is vital. By knowing how to contact your provider and initiate a claim, you can ensure you receive the financial protection you are entitled to, safeguarding yourself against the financial impact of vehicle depreciation and total loss.

If you want to read more articles similar to Understanding GAP Insurance Claims, you can visit the Insurance category.