04/10/2016

The relationship between international oil prices and currency exchange rates, particularly the US Dollar (USD), is a topic of considerable interest and extensive academic scrutiny. For decades, economists and market analysts have sought to understand the dynamic interplay between these two pivotal global economic indicators. The prevailing view, supported by a substantial body of literature, suggests a two-way causality between the USD exchange rate and crude oil prices. This means that not only can fluctuations in the dollar affect oil prices, but changes in oil prices can also influence the value of the US dollar.

Historically, this connection has been explained through various transmission channels. For instance, when the USD weakens, oil, which is predominantly priced in dollars, becomes cheaper for holders of other currencies. This increased affordability can stimulate demand, leading to higher oil prices. Conversely, a stronger USD makes oil more expensive for international buyers, potentially dampening demand and putting downward pressure on prices. Furthermore, oil-producing nations often adjust their currency valuations in response to oil price movements, creating a feedback loop.

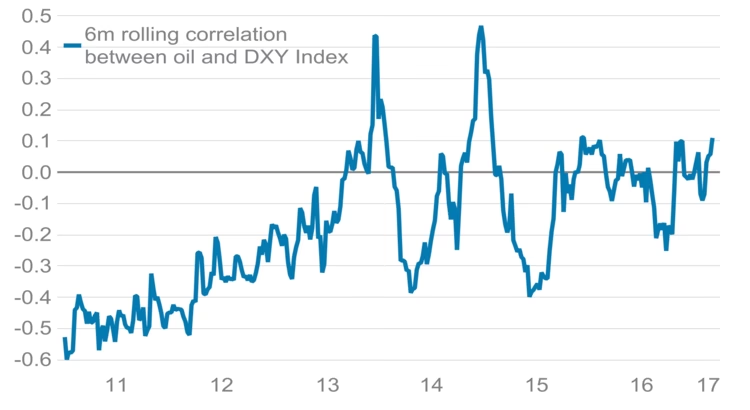

However, the clarity of this co-movement became less apparent in the wake of the 2008-2009 Global Financial Crisis (GFC). The period following the GFC was characterised by significant volatility in international oil prices, making the traditional correlations less predictable. This unpredictability has prompted researchers to delve deeper, employing more sophisticated analytical tools to distinguish between mere co-movements and genuine causal relationships.

Understanding Causality: Beyond Simple Correlation

It is crucial to differentiate between correlation and causation. While two variables might move in tandem, it doesn't necessarily mean one directly causes the other. Recent academic research, as highlighted by studies such as Beckmann et al. (2020) and Kilian and Zhou (2019), has moved beyond simple correlation analysis to explore the underlying causal links using advanced econometric techniques.

A significant portion of this research employs Granger-type analyses, often within Vector Autoregression (VAR) frameworks. These methods aim to assess whether past values of one variable can predict future values of another. Studies like Iwayemi and Fowowe (2011) and Ji et al. (2020) have used these approaches to examine the short-term responses of oil prices to exchange rate shocks and vice versa.

Some researchers further distinguish between short-run and long-run interconnections, utilising cointegration analyses (e.g., Chaudhuri and Daniel, 1998). Cointegration suggests that while two variables may drift apart in the short term, they tend to move back together in the long run, indicating a stable long-term relationship.

Advanced Methodologies: Capturing Complexity

Recognising the limitations of traditional methods, a second wave of studies has adopted more complex, nonlinear approaches. These include:

- Time-Frequency Approaches: These methods, such as those used by Tiwari et al. (2013), allow researchers to examine relationships across different time horizons and frequencies, revealing how the connection might vary depending on the timescale considered.

- Copula Functions: Utilised by Reboredo (2012) and Ji et al. (2019a), copulas are statistical tools that model the dependence structure between variables, allowing for a more nuanced understanding of how they interact, even when their marginal distributions are complex.

- Volatility Spillover Approaches: Techniques like Generalized Autoregressive Conditional Heteroskedasticity (GARCH) processes (Ding and Vo, 2012) and dynamic spillover frameworks (Albulescu et al., 2019) are employed to analyse how volatility in one market (e.g., currency markets) spills over into another (e.g., oil markets).

These advanced methods often reveal that the intensity of the nexus between oil prices and exchange rates can vary significantly over specific periods, often intensifying during times of economic stress or geopolitical uncertainty.

The Innovation of Time-Varying Causality

While the aforementioned methods offer valuable insights, traditional Granger-type analyses can be sensitive to the chosen estimation period and are influenced by the presence of heteroskedasticity (non-constant variance). Nonlinear approaches, while powerful, sometimes focus more on co-movement than direct causality and may lack the predictive power of classic tests.

To address these limitations, newer methodologies have emerged, such as the time-varying causality approach pioneered by Shi et al. (2018, 2020). This innovative method offers several advantages:

- No Data Differencing Required: It employs robust econometric techniques that can handle variables with different integration and cointegration properties without needing to difference or detrend the data, preserving more information.

- Dating Economic Turbulences: This approach can pinpoint specific periods of economic turbulence and detect real-time shifts in the direction of causality between variables.

- Precise Location of Causality Episodes: It can accurately identify the start and end dates of causality episodes, providing a detailed timeline of the relationship.

- Robustness to Conditions: Similar to methods used for financial bubble detection, this test is easily implemented under both homoskedastic and conditional heteroskedastic conditions, enhancing its reliability.

- Policy Intervention Support: Its good detection rate and ability to signal changes early allow for more effective and timely policy interventions.

- Flexibility: The technique can be adapted for various methods that capture time-varying relationships, including forward expanding-window tests, Markov-switching Granger causality, and rolling-window Granger causality tests.

Research by Shi et al. (2018, 2020) indicates that their recursive evolving method offers superior performance in finite samples compared to other existing techniques. For comparative purposes, a rolling-window test is often used alongside these newer approaches.

Robustness Checks: Ensuring Reliability

To ensure the findings are reliable and not dependent on specific data choices or methodologies, researchers often conduct extensive robustness analyses. In the context of the USD real exchange rate (USD REER) and crude oil prices (like West Texas Intermediate – WTI), these checks might include:

- Using Different Exchange Rate Indicators: Employing both broad (e.g., 60 economic partners) and narrow (e.g., 27 economic partners) measures of the USD REER to see if the relationship holds across different definitions of the dollar's value.

- Alternative Oil Price Benchmarks: Using different crude oil price indices, such as the Brent Crude Index, instead of WTI, to confirm that the results are not specific to a particular oil benchmark.

- Controlling for Economic Policy Uncertainty (EPU): Given the known interaction between oil prices and US economic policy uncertainty (as documented by Baker et al., 2016, and explored by various other studies), researchers may orthogonalise oil prices with respect to US EPU. This process removes the influence of EPU from oil prices, allowing for a clearer assessment of the direct relationship between oil prices and the USD REER. Studies by Aloui et al. (2016), Antonakakis et al. (2014), Kang and Ratti (2013), Kang and Wang (2018), Roubaud and Arouri (2018), and Shahzad et al. (2019) have shown how oil price shocks affect EPU, and conversely, how US EPU influences the oil-exchange rate nexus (Albulescu et al., 2019), with Akram (2020) also assessing the impact of geopolitical uncertainty. By controlling for EPU, researchers can isolate the specific impact of the USD exchange rate on oil prices, and vice versa.

Key Findings and Emerging Trends

Recent studies, such as Wen et al. (2018), have investigated the time-varying causality between crude oil prices and the USD exchange rate using alternative tests. While finding a predominantly one-way causal relationship running from crude oil prices to the USD exchange rate, these studies also note important nuances. For example, the intensity of this causality has been observed to increase after certain periods, such as post-2012. Furthermore, a short-lived period of causality running from the USD REER to WTI prices was identified during the 2008-2009 GFC, underscoring the dynamic and context-dependent nature of this relationship.

Conclusion: A Complex and Evolving Relationship

In summary, the US Dollar exchange rate and global oil prices are intrinsically linked. While the precise nature and direction of causality can vary over time and under different economic conditions, the evidence suggests a significant and often bidirectional relationship. Sophisticated econometric tools, particularly those capable of capturing time-varying effects, are essential for accurately understanding this complex interplay. As global economic landscapes continue to evolve, ongoing research will undoubtedly shed further light on this critical economic nexus.

Frequently Asked Questions:

- Does a weaker dollar always mean higher oil prices? Not necessarily. While a weaker dollar often makes oil cheaper for non-dollar buyers, stimulating demand, other factors like supply levels, geopolitical events, and global economic growth also significantly influence oil prices.

- Can oil prices affect the value of the US dollar? Yes, they can. Higher oil prices can lead to increased revenues for oil-exporting countries, potentially strengthening their currencies relative to the dollar. Conversely, a strong dollar can make oil imports cheaper for the US, but the overall impact depends on various economic factors and trade balances.

- What is the main takeaway regarding the USD-oil price link? The relationship is complex, often bidirectional, and changes over time. Recent research highlights the importance of using advanced econometric methods to capture these dynamic interactions accurately.

- Why is understanding this relationship important? It is crucial for policymakers, investors, and businesses as it impacts inflation, trade balances, energy costs, and overall economic stability globally.

If you want to read more articles similar to USD Exchange Rate and Oil Prices: A Deep Dive, you can visit the Automotive category.