22/05/2005

Modifying your car can be an incredibly rewarding experience, enhancing performance, aesthetics, or both. However, when it comes to insurance, things can quickly become a complex maze, especially with modifications that aren't immediately visible, such as an Engine Control Unit (ECU) remap. You've declared your visual modifications, which is a sensible start, but the prospect of remapping brings a new set of questions regarding detection and the potential impact on your policy. The core of your concern revolves around whether an insurance inspection, particularly one involving an ECU diagnostic check, can uncover an undeclared remap. Let's delve into the intricacies of this issue and explore the realities of detection.

The straightforward answer is yes, an insurance company can absolutely detect an ECU remap, particularly if they suspect foul play or during a thorough investigation following a significant claim. While a routine MOT or a basic garage diagnostic might not flag it, insurers have various methods and reasons to dig deeper. Understanding these methods and the severe consequences of non-disclosure is crucial before proceeding with any performance modifications that alter your vehicle's factory specifications.

Understanding ECU Remapping

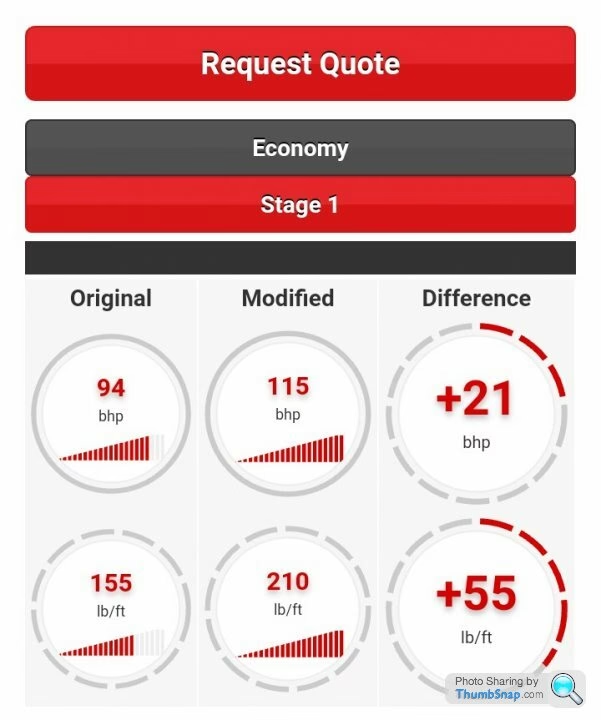

Before we discuss detection, it's important to clarify what an ECU remap entails. Your car's ECU is essentially its brain, controlling various engine functions like fuel injection, ignition timing, turbo boost, and more. A remap involves altering the software within the ECU to change these parameters, typically to increase horsepower and torque, improve fuel efficiency, or remove speed limiters. This process can significantly change the vehicle's characteristics beyond its factory-tuned state.

Why Insurers Care About Remaps

From an insurer's perspective, an ECU remap significantly alters the risk profile of your vehicle. A more powerful car is generally considered to be at a higher risk of being involved in an accident, potentially leading to more severe damage and higher claim costs. Furthermore, altered engine parameters can affect the vehicle's reliability and longevity, which also concerns insurers. Non-disclosure of such a fundamental change means the insurer is assessing a risk that is fundamentally different from the one they've actually insured, leading to potential policy invalidation.

Methods of Detection: Can They Really Tell?

While you might think a remap is a 'hidden' modification, there are several ways an insurance company, or a specialist they employ, can detect it. It's not always about a simple plug-in diagnostic; often, it's a combination of factors and a graduated approach to investigation.

Routine Diagnostic Checks vs. Forensic Analysis

A standard garage diagnostic tool, often used for routine servicing or fault finding, might not immediately highlight a remap. These tools typically read fault codes and live data, which may appear normal even with modified software. However, this is where the nuance lies. Insurers aren't relying on your local garage's basic scanner when a claim arises.

- Altered Software Signatures: ECUs have unique software identifiers and checksums. When a remap is performed, these signatures change. Specialist diagnostic equipment, far more advanced than a standard OBD-II scanner, can often detect these discrepancies by comparing the current software against the original manufacturer's specifications.

- Flash Counters: Many modern ECUs incorporate 'flash counters' or similar mechanisms. Every time the ECU's software is rewritten (flashed), this counter increments. Even if a remapper attempts to return the ECU to 'stock' software, the flash counter might reveal that the ECU has been tampered with multiple times. This is a tell-tale sign of modification.

- Performance Discrepancies: If your car is involved in an accident and its performance characteristics (speed, acceleration) are significantly beyond what's expected for a stock model, it can raise a red flag. While not direct evidence of a remap, it can certainly prompt a deeper investigation.

- Physical Inspection of the ECU: In some cases, especially with older vehicles or certain types of 'chip tuning', the ECU itself might show physical signs of tampering, such as solder marks or changed components.

- Accident Reconstruction & Telematics Data: In serious accidents, forensic engineers might be brought in. They can analyse data from the car's own systems (if available) or even reconstruct the accident based on physical evidence, potentially highlighting performance characteristics inconsistent with a stock vehicle. If you have a black box (telematics) fitted, this data can also be used to show driving behaviour inconsistent with a standard vehicle's capabilities.

- Whistleblowers & Social Media: This is an often-overlooked but significant risk. If you've discussed your remap online, on forums, or even told friends who then have a falling out with you, information can easily reach your insurer. Insurers do conduct background checks and may even monitor social media in the event of a claim.

The Risk of Non-Disclosure: Why It's Not Worth It

The potential savings on your premium by not declaring a remap are dwarfed by the catastrophic consequences if your insurer discovers the modification after a claim. Here's what you could face:

- Policy Invalidation: This is the most common and severe consequence. Your insurer can declare your policy void from the outset, meaning it was effectively never in force.

- Refusal to Pay Claims: If your policy is invalidated, any claim you make, regardless of fault, will be refused. This means you would be personally liable for all damages, including repairs to your own vehicle, third-party vehicle damage, property damage, and potentially millions in personal injury compensation.

- Recovery of Paid Claims: Even if they initially pay out a claim before discovering the remap, they have the right to recover those funds from you.

- Difficulty Obtaining Future Insurance: Having a voided policy or a history of non-disclosure will make it extremely difficult and expensive to obtain insurance in the future. You will have to declare this to every subsequent insurer, and many may refuse to quote or charge exorbitant premiums.

- Criminal Charges: In severe cases, particularly if non-disclosure is deemed fraudulent, you could face criminal prosecution for insurance fraud, leading to fines, a criminal record, and even imprisonment.

Consider the scenario where you're involved in a serious accident. The costs could easily run into tens of thousands, if not hundreds of thousands, especially if there are injuries involved. Is saving a few hundred quid on your premium worth the risk of financial ruin and a criminal record?

Declaring Your Remap: The Sensible Approach

While Admiral's response suggests a significant premium increase or refusal, it's always better to be upfront. Many specialist insurers cater specifically to modified vehicles and performance cars. They understand the enthusiast market and can provide tailored policies, albeit at a higher cost reflecting the increased risk. It's crucial to get quotes from these specialist providers rather than just mainstream insurers who may not be equipped to underwrite modified vehicles.

Here's a comparison of the risks involved:

| Action | Potential Outcome (Declaring Remap) | Potential Outcome (Not Declaring Remap) |

|---|---|---|

| Premium Cost | Higher premium, potentially significant. | Lower initial premium (illusion of saving). |

| Policy Validity | Policy remains valid, full cover. | Policy at risk of being invalidated. |

| Claim Payout | Claims paid out as per policy terms. | Claims likely to be refused; personal liability for all costs. |

| Future Insurance | No negative impact on insurance history. | Difficulty obtaining future insurance; higher premiums. |

| Legal Consequences | None. | Risk of insurance fraud charges. |

| Peace of Mind | Complete peace of mind knowing you're covered. | Constant worry about detection, especially after an incident. |

Frequently Asked Questions

Let's address some common queries surrounding ECU remapping and insurance.

Q: Is an ECU remap illegal in the UK?

A: No, an ECU remap itself is not illegal in the UK, provided it doesn't cause the vehicle to breach emissions regulations or other roadworthiness standards (e.g., noise limits). However, it is a modification that must be declared to your insurance company. Failure to declare it is where the legal and financial problems arise, as it constitutes a breach of your insurance contract.

Q: Will my MOT detect an ECU remap?

A: Generally, no. An MOT test focuses on the vehicle's roadworthiness, safety, and emissions. While an emissions test might fail a poorly executed remap that increases pollutants, the MOT test itself isn't designed to detect software modifications or 'flash counts' in the ECU. It's not an investigative diagnostic for modifications.

Q: What if I buy a car that's already remapped? Am I still liable?

A: Yes, absolutely. When you purchase a vehicle, it becomes your responsibility to ensure all modifications are declared to your insurer, regardless of whether you carried them out. It's crucial to ask the seller about any modifications, and ideally, get a pre-purchase inspection from a reputable mechanic who can check for signs of remapping or other alterations. If you're unsure, declare it as 'potentially modified' or seek expert advice. Ignorance is not a valid defence with insurers.

Q: Are all remaps detectable, even if the tuner tries to hide it?

A: While some advanced tuners might employ techniques to make detection harder (e.g., resetting flash counters, mimicking OEM software versions), a determined and forensic investigation by an insurer's specialist will likely uncover the remap. The financial stakes for insurers in large claims mean they are prepared to invest in such investigations. It's incredibly difficult to completely erase all digital footprints of an ECU rewrite.

Q: What if I flash the ECU back to stock before an inspection or claim?

A: This is a common misconception. While you might be able to load the original software back onto the ECU, the 'flash counter' discussed earlier will still show that the ECU has been written to multiple times. This alone can be enough evidence for an insurer to prove tampering. Furthermore, if the original software was not properly backed up, or if the remapping process altered hardware components (e.g., through 'chip tuning'), simply flashing back to stock might not be possible or effective.

Conclusion: Honesty is the Only Policy

While the temptation to save money on insurance premiums is understandable, particularly for a young driver with a powerful car, the risks associated with not declaring an ECU remap are simply too high. The financial and legal ramifications of an invalidated policy following a serious incident could be life-altering. Insurers are becoming increasingly sophisticated in their detection methods, and the 'hidden' nature of a remap offers little protection when they have a financial incentive to investigate. Always declare all modifications to your insurer. If your current provider is unwilling to cover you, seek out specialist insurers who understand and cater to the modified car market. It's a small price to pay for genuine peace of mind and the assurance that you are fully covered should the worst happen.

If you want to read more articles similar to ECU Remap & Insurance: Will They Know?, you can visit the Automotive category.