03/09/2007

When owning or operating a vehicle in the UK, two essential topics frequently arise: Value Added Tax (VAT) and Road Tax. Whether you’re an individual purchasing a new car or a business managing an entire fleet, it’s absolutely crucial to understand how VAT interacts with various vehicle-related costs, including the often-misunderstood Road Tax, and what implications this might have on your overall motoring expenses. This comprehensive guide aims to demystify the intricacies of VAT as it applies to vehicles, providing clarity on everything from direct purchases to complex business scenarios and, crucially, its relationship with Vehicle Excise Duty.

Understanding these financial aspects is not just about compliance; it’s about making informed decisions that can significantly impact your budget. We’ll break down the fundamental concepts of VAT and Road Tax individually before delving into their often-confusing intersection, exploring how VAT applies to different vehicle transactions, and offering insights into what businesses can and cannot reclaim. Our goal is to provide you with a robust understanding, ensuring you navigate the UK’s vehicle taxation landscape with confidence.

- What is VAT (Value Added Tax)?

- What is Road Tax (Vehicle Excise Duty - VED)?

- Is VAT Charged on Road Tax? The Definitive Answer

- Understanding VAT on Vehicle Purchases and Related Costs

- VAT and Vehicle Leasing or Hire

- Road Tax Exemptions: Do They Affect VAT?

- Can You Reclaim VAT on Road Tax Payments?

- VAT on Cars for Businesses: A Deeper Dive

- Essential Record Keeping for VAT on Cars

- Conclusion

- Frequently Asked Questions (FAQs)

What is VAT (Value Added Tax)?

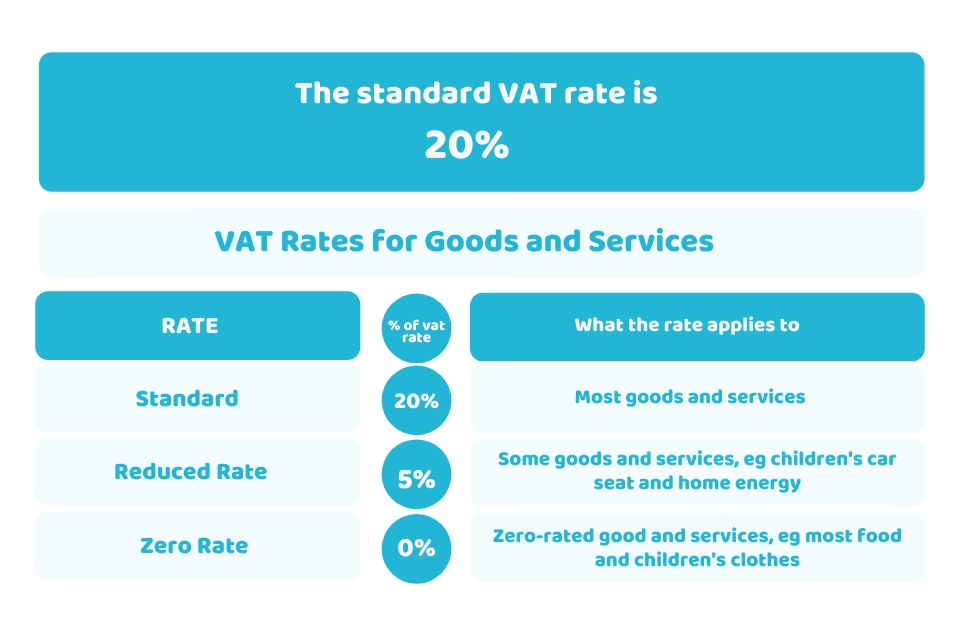

VAT, or Value Added Tax, is a consumption tax applied to the sale of most goods and services in the United Kingdom. It is a fundamental part of the UK’s tax system and plays a significant role in nearly all commercial transactions. The standard VAT rate in the UK is currently 20%, although certain items and services may be subject to a reduced rate (5%) or a zero rate (0%), while others are entirely exempt from VAT. When you purchase goods or services, VAT is generally included in the price you pay. Businesses, particularly those registered for VAT, act as tax collectors on behalf of His Majesty's Revenue and Customs (HMRC), charging VAT on their sales and, in turn, often reclaiming VAT on their purchases. This system ensures that the tax is ultimately borne by the end consumer.

While VAT is pervasive, its application can vary significantly depending on the nature of the transaction. In the context of vehicles, its interaction with various costs, from the initial purchase price to ongoing maintenance and even specific taxes, can be particularly nuanced, leading to common misunderstandings.

What is Road Tax (Vehicle Excise Duty - VED)?

Road Tax, officially referred to as Vehicle Excise Duty (VED), is a statutory tax imposed on vehicles driven or parked on public roads in the UK. Unlike VAT, VED is a direct government levy, not a consumption tax collected by businesses. The amount of Road Tax payable is determined by several factors, including the vehicle’s CO₂ emissions, its fuel type, and the date it was first registered. Generally, cars with higher emissions incur higher charges, aligning with the government’s broader objectives of promoting environmental sustainability and discouraging the use of more polluting vehicles. This tax is paid annually, biannually, or monthly, ensuring that vehicles using the public road network contribute to its upkeep and environmental initiatives.

It’s important to distinguish VED from other motoring costs. It is a tax on the vehicle itself for its use of the roads, separate from the cost of fuel, insurance, or vehicle maintenance. Its structure is designed to incentivise the purchase and use of cleaner, more efficient vehicles.

Is VAT Charged on Road Tax? The Definitive Answer

Here’s the critical question that causes frequent confusion: Is VAT applied to Road Tax (Vehicle Excise Duty) in the UK? The definitive answer is a resounding no — VAT is not charged directly on Road Tax. VED is a government-imposed statutory tax, and like other direct taxes such as Income Tax, Corporation Tax, or Council Tax, it falls entirely outside the scope of VAT. This means that when you receive your annual Road Tax bill, you will not see VAT added on top of the stated amount. The payment you make for VED is purely the tax itself, without any additional VAT component.

The confusion often arises because VAT is applicable to many other services and transactions associated with owning and operating a vehicle. While Road Tax itself is VAT-exempt, other related costs—from the purchase of the vehicle to its servicing and accessories—almost certainly will include VAT. It is this broader context of vehicle expenses that often leads people to mistakenly believe VAT is levied on VED.

While there is no VAT on Road Tax, VAT is a significant component when purchasing, leasing, or maintaining a vehicle in the UK. Its application varies considerably between new and used vehicles, and also depending on whether the vehicle is for private or business use.

VAT on New Vehicle Purchases

When purchasing a brand-new vehicle in the UK, VAT is a substantial part of the total cost. The following vehicle-related costs typically include VAT at the standard rate of 20%:

- The Sale Price of a New Car: VAT is charged at 20% on the total purchase price of the vehicle. This is usually included in the advertised price, but it’s crucial to be aware that a fifth of what you’re paying goes directly to HMRC.

- Delivery and Registration Fees: Any charges levied by the dealership for delivering the car to you or handling the initial registration process are generally subject to VAT.

- Vehicle Accessories and Modifications: If you opt for additional features, upgrades, or customisations at the point of sale (e.g., upgraded alloys, a premium sound system, or a towing bar), VAT will apply to these additions.

- Warranties, Service Packages, and Roadside Assistance Plans: Many dealerships offer optional extras like extended warranties, pre-paid service plans, or roadside assistance. VAT is also charged on the cost of these services.

For VAT-registered businesses, there may be opportunities to reclaim some or all of the VAT paid on a new vehicle purchase, provided the vehicle is used exclusively for business purposes, without any private use. This is a strict rule, and businesses must adhere to HMRC’s guidelines meticulously to qualify.

VAT on Used Vehicle Purchases: The Margin Scheme and Beyond

The situation for used vehicles differs considerably from new ones. In most private sales between individuals, VAT is not applicable, as the seller is not typically a VAT-registered business. However, when buying a used vehicle from a dealership or a professional trader, VAT rules come into play, often under a special scheme:

- VAT Margin Scheme: This is the most common method used by VAT-registered dealers for second-hand vehicles. Under this scheme, VAT is not applied to the entire sale price of the vehicle. Instead, VAT is only charged on the dealer’s profit margin (the difference between what they paid for the car and what they sell it for). This means the buyer effectively pays less VAT than if standard VAT were applied to the full price. The invoice for a car sold under the margin scheme will typically not show the VAT amount separately.

- Standard VAT: Occasionally, a dealer might sell a nearly-new or demonstrator model that was purchased with VAT shown separately on the invoice (e.g., a car previously used as a company car where VAT was reclaimed by a business). In such rarer cases, the dealer may apply standard VAT (20%) to the full sale price. The invoice will clearly show the VAT amount separately.

In both scenarios for used vehicle sales, it’s important to remember that the Road Tax portion, being a statutory government tax, remains VAT-exempt. The VAT, if applicable, relates solely to the vehicle’s sale price or the dealer’s margin on that sale.

VAT and Vehicle Leasing or Hire

Leasing or hiring a vehicle introduces another context where VAT on Road Tax might cause confusion. When you lease a vehicle, you are essentially paying for its use over a period rather than purchasing it outright. Let’s clarify how VAT typically applies in these situations:

- Lease Payments: The monthly or periodic lease payments you make to the leasing company will typically include VAT. This is because the leasing company is providing a service (the use of the vehicle) which is subject to VAT.

- Road Tax within Lease Costs: If the leasing company pays the Road Tax (VED) on your behalf and then charges it back to you as part of the overall lease cost or as a separate line item on your invoice, VAT may appear to be added to the amount related to VED. However, this is not because VAT is charged on VED itself. Instead, it’s because the leasing company is providing a bundled service that includes the administration and payment of the VED, and that entire bundled service falls under their VAT regulations. They are effectively passing on the cost of a non-VATable item as part of a VATable service. For VAT-registered businesses, the VAT on the lease payments (excluding any specific VED pass-through that is clearly shown as non-VATable) can often be reclaimed, subject to HMRC’s rules on business vs. private use.

It’s essential to scrutinise lease agreements and invoices carefully to understand which components are subject to VAT and which are not. While the VED itself is never VATable, the way it’s administered and charged back by a third party might make it appear so within a larger, VATable service.

Road Tax Exemptions: Do They Affect VAT?

Several categories of vehicles are exempt from Road Tax (VED) in the UK. While these exemptions mean you won't pay the annual VED charge, it's important to understand how this interacts with VAT:

- Electric Vehicles (EVs): Fully electric vehicles registered after 1 April 2017 currently qualify for zero Road Tax. This is a key government incentive to encourage the adoption of greener transport.

- Classic Cars: Vehicles manufactured and registered over 40 years ago (on a rolling basis) are typically exempt from VED.

- Vehicles for Disabled People: Certain mobility-related vehicles used by or for disabled individuals may be exempt from Road Tax.

- Charitable Vehicles: Vehicles used exclusively for specific charitable purposes may also qualify for VED exemption.

- Public Sector Vehicles: Vehicles used by emergency services such as police, ambulance, and fire services are tax-exempt.

Crucially, while these vehicles may avoid Road Tax, it’s important to note that VAT could still apply to other related costs. For example, VAT will be charged on the purchase price of a new electric vehicle, as well as on servicing, parts, accessories, and charging equipment. The VED exemption only applies to the Road Tax itself, not to the broader ecosystem of vehicle-related goods and services.

Can You Reclaim VAT on Road Tax Payments?

Since VAT on Road Tax does not exist in the traditional sense—because VED is a statutory tax and not a VAT-able supply—you cannot reclaim VAT on your Road Tax payments. Businesses often inquire about this, particularly if they operate a fleet of vehicles. The simple truth is, if no VAT was charged on the payment in the first place, there is nothing to reclaim. This is a fundamental distinction from other business expenses where VAT is clearly itemised.

However, businesses may still be eligible to reclaim VAT on a variety of other legitimate vehicle-related expenses, provided they are VAT-registered and the expenses relate to business use. These include:

- Fuel Purchases: VAT can often be reclaimed on fuel used for business journeys.

- Vehicle Servicing and Repairs: VAT charged on maintenance, servicing, and repair work for business vehicles is generally reclaimable.

- Leasing and Hire Costs: As mentioned, VAT on lease payments for business vehicles can typically be reclaimed, although rules may vary depending on private use.

- New Vehicle Purchases: If a new vehicle is purchased solely for business use (e.g., a pool car with no private use, or a vehicle for a driving school), the VAT paid on the purchase price may be reclaimable.

Always maintain meticulous records and consult HMRC guidance or a tax professional to ensure compliance and maximise eligible VAT recovery.

VAT on Cars for Businesses: A Deeper Dive

Navigating the complexities of VAT on car expenses can be particularly challenging for businesses in the UK. Beyond the direct question of Road Tax, understanding the broader VAT rules applicable to buying, selling, and operating business vehicles is essential for compliance and optimising VAT recovery. This section provides an in-depth understanding of these rules, which are crucial for any business managing a fleet or even just a single company car.

Defining a 'Car' for VAT Purposes

For VAT purposes, the definition of a 'car' is specific and critical, as it determines how VAT is applied and reclaimed. HMRC defines a car as any motor vehicle with three or more wheels, typically used on public roads, and primarily constructed or adapted for carrying passengers. However, there are several key exceptions where a vehicle is not considered a 'car' for VAT purposes, which can allow for different VAT treatment:

- Vehicles designed to carry one person or 12 or more people (e.g., minibuses).

- Caravans, ambulances, and prison vans.

- Vehicles over 3 tonnes in unladen weight.

- Special purpose vehicles such as ice cream vans and hearses.

- Vehicles with a payload of one tonne or more (e.g., most vans and pick-up trucks).

Understanding this distinction is vital because vehicles falling under these exceptions are often treated more favourably for VAT purposes, allowing businesses to reclaim VAT on their purchase where they might not for a standard 'car'.

Reclaiming VAT on Car Purchases for Business Use

In general, VAT on the purchase of a car is not recoverable unless the vehicle is used exclusively for business purposes without any private use. This is a very strict rule from HMRC. Even a small amount of private use, such as an employee using a company car for personal errands on a weekend, can disqualify the business from reclaiming the VAT on the purchase. However, there are specific situations where VAT can be reclaimed:

- Stock in Trade: If the vehicle is part of the stock in trade of a motor dealer or manufacturer, meaning it is bought with the sole intention of being sold on, the VAT paid on its purchase can be reclaimed.

- Commercial Use: If the vehicle is primarily used as a taxi, for driving instruction, or for self-drive hire (e.g., a car rental company), the VAT paid on its purchase is generally reclaimable. These are considered 'qualifying cars' for VAT purposes because their very nature is commercial.

It is paramount for businesses to accurately classify their vehicles and their intended use to ensure compliance with these rules and avoid potential penalties from HMRC.

VAT When Buying Cars to Sell On

For VAT-registered motor dealers, reclaiming VAT on cars bought to sell is relatively straightforward. When a dealer purchases a vehicle that is intended for resale, the invoice will detail the VAT amount paid. This VAT can then be reclaimed on the dealer's next VAT Return. To ensure full compliance and avoid issues during an HMRC audit, it is crucial for dealers to maintain accurate and comprehensive records of these transactions. Furthermore, for cars to qualify for this VAT reclaim, they must be genuinely intended for sale within a reasonable timeframe, typically within 12 months of purchase. This prevents businesses from reclaiming VAT on vehicles that are then held for extended periods or used for non-qualifying purposes.

VAT on Imported Cars

When importing cars into the UK, businesses must use the Notification of Vehicle Arrivals (NOVA) system within 14 days of the vehicle arriving. This system helps HMRC track vehicles entering the country for registration and taxation purposes. There are specific exceptions to this requirement, such as for cars with very small engines (below 49cc or 7.2 kilowatts if electric) or those using certain secure registration schemes. If circumstances change and a secure registration scheme can no longer be used, NOVA must be completed promptly.

For cars imported from outside the UK to Great Britain, or from outside the EU to Northern Ireland, VAT must be paid through customs. This import VAT can subsequently be reclaimed on your next VAT Return, similar to VAT on domestic purchases. For cars brought from the EU into Northern Ireland, these transactions are accounted for as an 'acquisition' on your VAT Return, where you 'self-account' for the VAT (declaring both output and input tax). Proper documentation and timely submission via the NOVA system are essential for smooth import processes and VAT recovery.

VAT on Business Cars Not for Resale

Even if a business does not sell cars, it can still reclaim VAT on certain vehicles used for specific business purposes, provided they fall outside the strict 'car' definition or are used in specific ways. For example, VAT can often be reclaimed on:

- Vehicles used for daily rental to customers (e.g., a van rental company).

- Vehicles used for test drives by potential customers.

- Courtesy cars provided to customers while their own vehicles are being serviced.

However, a critical caveat applies: if a vehicle is used privately at all, such as by an employee for personal travel on weekends or during holidays, then VAT must be paid back to HMRC, either through a specific 'output tax' adjustment or by restricting the initial input tax claim. HMRC provides detailed guidance (e.g., VAT Notice 700/57) on calculating the amount of VAT to pay back in such scenarios, which often involves a 'scale charge' based on the vehicle's CO2 emissions.

Margin Scheme for Second-Hand Cars

When dealing specifically with second-hand cars, a different set of VAT rules applies for VAT-registered dealers if they use the Margin Scheme. This scheme is designed to prevent 'double taxation' on used goods. It allows dealers to account for VAT only on the difference between the purchase price and the selling price of the vehicle (the profit margin), rather than the full selling price. This is particularly beneficial for dealers as it reduces the amount of VAT they owe.

When You Can Use the Margin Scheme

The Margin Scheme can be used for eligible second-hand cars. A vehicle is considered second-hand if it has been driven on the road for business or pleasure purposes or is otherwise suitable for further use. This includes most used cars purchased from private individuals or from other dealers who also sold them under the Margin Scheme.

When You Cannot Use the Margin Scheme

The Margin Scheme cannot be used for:

- New cars.

- Imported cars (including those collected on your behalf from outside the UK/EU).

- Cars purchased on an invoice that separately shows VAT (i.e., cars where the previous owner reclaimed VAT or sold under standard VAT rules).

- Category A and B write-off cars or those subject to the End Of Life Directive.

- New means of transport purchased from EU countries into Northern Ireland.

- Cars bought from registered dealers in EU countries that were supplied to Northern Ireland not under a margin scheme.

- Cars already sold under the normal VAT rules.

- Cars where VAT was reclaimed by the dealer, or they were entitled to reclaim it, on the initial purchase.

Steps for Using the Margin Scheme

If you are a dealer using the Margin Scheme, the process involves a few key steps:

- Check the Rules: Always confirm that the vehicle you are buying or selling qualifies for the Margin Scheme.

- Work Out the Margin: Calculate the purchase price and the selling price of the vehicle. The gross margin is the selling price minus the purchase price.

- Calculate VAT Due: The VAT due is calculated by multiplying the gross margin by 1/6 (which is the VAT fraction for a 20% VAT rate). For example, if your margin is £600, the VAT due is £100.

- Keep Records: It is legally required to maintain a detailed stock book that tracks each item sold under the Margin Scheme individually. This stock book must show the purchase date, purchase price, sale date, and selling price for each vehicle. You must also keep copies of all purchase and sales invoices, even if they don't show VAT separately.

Essential Record Keeping for VAT on Cars

Keeping accurate and meticulous records is absolutely essential when dealing with VAT on car expenses, both for compliance with HMRC regulations and for effective financial management. This includes maintaining your normal VAT records, such as purchase and sales invoices, and also additional specific records for cars bought or sold under the Margin Scheme. For vehicles supplied on a sale or return basis, detailed records of transfers and sales are necessary. Any vehicle used privately by an employee that requires a VAT adjustment will also need careful record-keeping to justify the calculations.

HMRC can request to see these records at any time, and incomplete or inaccurate records can lead to penalties. Therefore, establishing a robust system for documentation, whether digital or physical, is a non-negotiable aspect of managing VAT on your vehicle fleet.

Conclusion

To summarise, the fundamental point to remember is that Road Tax (Vehicle Excise Duty) is not subject to VAT in the UK. This is a common misconception, primarily because VAT is applicable to so many other motoring-related services and costs. While you will never pay VAT directly on your VED bill, you will almost certainly encounter VAT in various other areas related to owning, operating, purchasing, or leasing a vehicle, particularly if you are a VAT-registered business.

Understanding the strict rules around reclaiming VAT on vehicle purchases, the nuances of the Margin Scheme for used cars, and the implications of private use for business vehicles is crucial. Always ensure you understand what is and isn’t VAT-inclusive when reviewing quotes, invoices, or financial statements for vehicles and associated services. When in doubt, consulting a qualified tax professional or referring to HMRC’s official guidance will provide the most accurate and up-to-date information for your specific circumstances.

Frequently Asked Questions (FAQs)

1. Is VAT included in car Road Tax payments?

No, VAT is not charged on Vehicle Excise Duty (Road Tax) in the UK. VED is a government-imposed statutory tax and falls outside the scope of VAT.

2. Do electric vehicles pay Road Tax or VAT?

Electric vehicles (fully electric cars registered after 1 April 2017) are currently exempt from Road Tax (VED). However, they are still subject to VAT on their purchase price, as well as on related services, parts, and accessories.

3. Can I reclaim VAT on Road Tax for business purposes?

No, since VED is not subject to VAT, there is no VAT component to reclaim. However, VAT on other vehicle expenses such as fuel, servicing, repairs, and eligible lease payments may be reclaimable for VAT-registered businesses.

4. What is the VAT Margin Scheme for used cars?

The VAT Margin Scheme allows VAT-registered dealers to account for VAT only on their profit margin (the difference between the sale price and purchase price) when selling eligible second-hand vehicles, rather than on the full selling price. This scheme cannot be used for new cars or cars where VAT was previously reclaimed.

5. When can a business reclaim VAT on a car purchase?

Generally, VAT on a car purchase is not reclaimable unless the car is used exclusively for business purposes with absolutely no private use. Exceptions include cars purchased as stock in trade by dealers, or cars primarily used for commercial purposes like taxis, driving instruction, or self-drive hire.

6. How does VAT apply to imported cars?

For cars imported from outside the UK to Great Britain or from outside the EU to Northern Ireland, VAT must be paid through customs upon import. This import VAT can then be reclaimed by VAT-registered businesses on their VAT Return. For cars brought from the EU into Northern Ireland, it is accounted for as an 'acquisition' on the VAT Return.

If you want to read more articles similar to VAT and Road Tax in the UK: A Comprehensive Guide, you can visit the Vehicles category.