10/01/2002

Navigating the world of car purchases can often feel like a labyrinth, and a significant part of that complexity revolves around the Value Added Tax, or VAT. In the United Kingdom, this tax typically adds a substantial 20% to the cost of most goods and services, and cars are no exception. While it might appear to be an unavoidable expense, the reality is often more nuanced. There are specific circumstances where you might be exempt from paying VAT altogether, or perhaps only have to pay a reduced amount. Understanding these intricacies is crucial for making informed decisions and avoiding unexpected financial burdens. This guide aims to demystify VAT on cars, offering clarity on who pays, when you can reclaim it, and how it applies to both new and used vehicles.

Understanding VAT in the UK

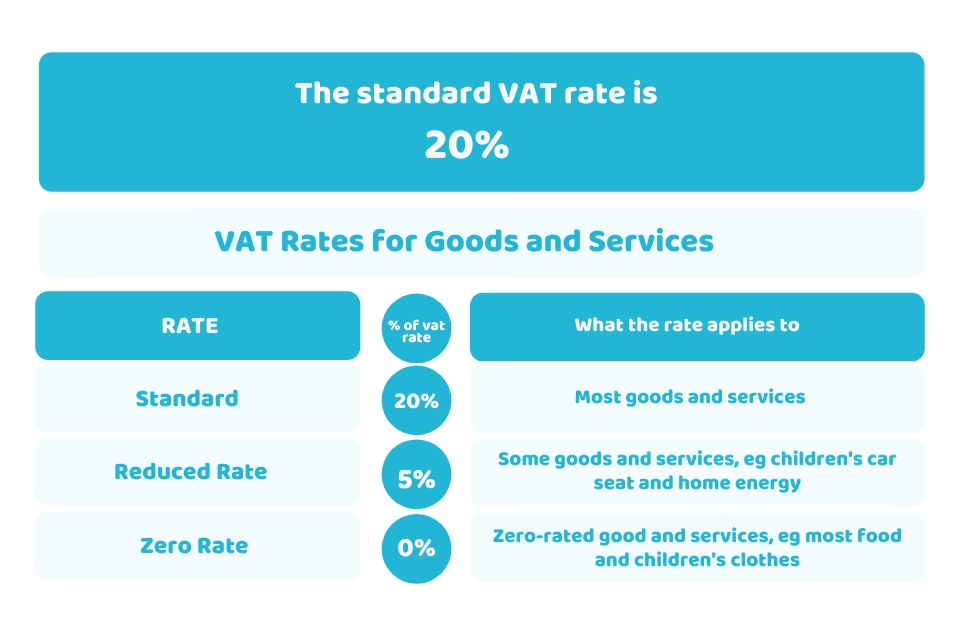

Value Added Tax (VAT) is a consumption tax levied on most goods and services sold within the UK. For cars, the standard rate is 20%. This tax is applied to the cost of the vehicle itself, as well as associated expenses like delivery, pre-sale inspections, and the fitting of number plates. Even any optional extras you choose will have VAT added to their price. While VAT is often itemised separately on an invoice, it is ultimately paid as part of the total purchase price. Therefore, when budgeting for a new car, it's essential to factor in this additional 20% to get an accurate picture of the final cost.

Who Pays VAT on Cars?

In the UK, the 20% VAT charge applies to the purchase of most new cars. This holds true whether you are buying the vehicle outright with cash, through a finance agreement, or via a lease. However, this is not a universal rule, and several exceptions exist:

VAT-Registered Businesses

If you are a VAT-registered business or an individual who operates a business and is registered for VAT, you may be eligible to reclaim some or all of the VAT paid on a car. This is typically possible if the vehicle is used predominantly for business purposes. For example:

- Taxi Drivers: Taxi drivers can usually reclaim the full VAT on a car if it is primarily used for their work.

- Solely Business Use: For other businesses, reclaiming VAT requires proving that the car will be used exclusively for business purposes. This means there can be no private use whatsoever, and the vehicle cannot even be accessible for private use (e.g., parked at an employee's home overnight). This strict criterion can make it challenging to reclaim the full VAT on a car purchase.

Light Commercial Vehicles (Pick-up Trucks)

Pick-up trucks that are classified as light commercial vehicles (similar to vans) have a different VAT treatment. If the vehicle's carrying capacity for cargo exceeds 1,000kg, VAT-registered buyers can reclaim a portion of the VAT paid.

Drivers with Disabilities

Individuals who are wheelchair users and require a specially adapted vehicle for their personal use may be exempt from paying VAT on the purchase of such a vehicle. However, there are specific conditions that must be met, and a formal application process, including filling out a designated form, is required before the purchase can be made VAT-free.

VAT on New Cars vs. Used Cars

The application of VAT differs significantly between new and used cars:

VAT on New Cars

As mentioned, VAT is charged at 20% on the price of new cars. This tax is applied to the base cost of the vehicle and any additional costs, such as delivery, preparation, and accessories. The VAT is typically shown separately on the invoice, although it is paid as part of the overall transaction.

VAT on Used Cars

The situation with used cars is more varied:

- Private Sales: If you buy or sell a used car privately, between two individuals, VAT does not apply.

- Dealer Sales - Margin Scheme: The most common scenario when buying a used car from a dealer is the VAT second-hand margin scheme. Under this scheme, the dealer only pays VAT on the profit margin they make from the sale – the difference between the price they bought the car for and the price they are selling it for. The VAT rate is effectively calculated as one-sixth of this profit margin. While this VAT is included in the car's advertised price, it is not itemised separately on the invoice.

- Dealer Sales - Standard VAT: In some cases, a dealer might choose to charge 20% VAT on the full selling price of a used car. This is less common as it usually results in a higher tax charge compared to the margin scheme, making the car more expensive for the buyer.

It's always advisable to clarify with the dealer how VAT is being applied to the used car you are interested in purchasing.

When Do You Pay VAT on Selling a Car?

The rules for charging VAT when selling a car depend on whether VAT was applicable on your purchase and if you reclaimed it:

- Cars previously subject to VAT reclaim: If you are selling a car on which you previously claimed VAT back (e.g., a car used for a driving school or a company pool car), you will need to account for VAT on the total selling price.

- Cars purchased with VAT but not reclaimed: If you bought a car and paid VAT, but were not eligible to reclaim it, there is no requirement to charge VAT when you sell it. This type of sale is considered VAT-exempt. Consequently, you cannot reclaim any VAT paid on costs associated with selling the car, such as auction fees.

- Cars purchased without VAT: If you acquired a car without paying VAT (e.g., a second-hand purchase from a private individual or a dealer using the margin scheme), and you sell it under the same scheme, you only account for VAT on the profit margin. You do not charge VAT on the full selling price, and no VAT will be shown on your sales invoice.

VAT on Car Running Costs

Beyond the purchase price, VAT also affects the running costs of a vehicle. Here's a look at common expenses:

Car Leasing

When it comes to car leasing, businesses are generally only permitted to reclaim 50% of the input tax incurred on the leasing costs. This restriction applies regardless of the car's value. However, this 50% limit does not apply if the vehicle is used exclusively as a taxi, for self-drive hire, or for driving instruction purposes.

Car Fuel

For most motor expenses, you can claim back the VAT in full, provided you have valid VAT invoices. Car fuel, however, has special rules, particularly concerning private use. If you reclaim VAT on fuel that is also used for private motoring, you must pay a VAT 'scale charge'. This charge is a fixed amount determined by the car's CO2 emission band and is not directly related to the actual amount of private mileage. It's a common oversight on VAT returns and is often one of the first things HMRC inspectors look for.

Businesses should calculate whether it is financially beneficial to reclaim VAT on fuel. If the amount of VAT you can reclaim on fuel is less than the VAT payable on the scale charge, it may be more advantageous to opt out of reclaiming VAT on fuel altogether to avoid the scale charge. If an employee is fully compensated by the company for any private fuel used, no scale charges are due. However, output VAT must be charged on the amount paid by the employee to the company. While you can choose to apply scale charges to some cars and not others, this can significantly complicate VAT record-keeping.

Car Parking

You are permitted to reclaim the VAT incurred on business-related car parking expenses, including parking at your business premises.

Mileage Allowance

When you pay employees a fixed mileage allowance for business travel (e.g., the 45p per mile rate), this rate is designed to cover various costs, including fuel, repairs, insurance, and depreciation. Crucially, businesses are allowed to reclaim the VAT on the fuel element of these payments. Many businesses overlook this, but it's a potential area for VAT recovery. To identify the fuel element, HMRC provides advisory fuel-only mileage rates. You can reclaim the VAT by multiplying the fuel-only rate by 20 and dividing by 120. If you haven't reclaimed this VAT in the past, you can go back up to three years to make a retrospective claim.

Frequently Asked Questions

Is VAT charged on road tax?

No, VAT is not charged on vehicle excise duty, commonly known as road tax. This is a separate government charge.

Do I have to pay VAT on my car?

Generally, yes, 20% VAT is included in the price of new cars purchased in the UK. However, VAT-registered businesses may be able to reclaim some or all of it if the car is used exclusively for business. Drivers with disabilities purchasing specially adapted vehicles may also be exempt.

Do you pay VAT when selling a car?

It depends. If you previously reclaimed VAT on the car, you must charge VAT on the selling price. If you bought the car with VAT but didn't reclaim it, you don't need to charge VAT on sale. If you bought the car without VAT (e.g., private sale), you only account for VAT on the profit margin if selling under the margin scheme.

Do I have to charge VAT on car parking?

If you are providing car parking as a business service, then yes, you will need to charge VAT on the parking fees, unless you are specifically exempt. Businesses can reclaim VAT on their own business car parking expenses.

Conclusion

Understanding Value Added Tax on cars in the UK can indeed be a complex undertaking. However, by grasping the fundamental principles and common scenarios, you can navigate these financial waters with greater confidence. Remember that VAT treatment differs for new and used vehicles, impacting how it's calculated and paid. Crucially, depending on your specific circumstances, such as being a VAT-registered business or a qualifying individual with a disability, you may be entitled to reclaim some or all of the VAT paid. Always ensure you conduct thorough research and don't hesitate to ask questions to dealers or consult with tax professionals before making significant vehicle purchases to ensure you are making the most informed decisions and avoiding any unforeseen costs.

If you want to read more articles similar to VAT on Cars: A Comprehensive Guide, you can visit the Automotive category.