19/05/2015

Becoming a parent to a newly licensed driver is a significant milestone, often accompanied by a new set of anxieties and responsibilities. Among the most pressing concerns is the financial aspect of ensuring your young driver is safe and legally covered on the road. While the question of "How much does a car repair cost?" is a general one, for parents of L and P plate drivers, this question takes on a more specific and often more substantial dimension. The introduction of a young driver into your household isn't just about teaching them to navigate traffic; it's also about understanding and managing the associated expenses, particularly when it comes to vehicle upkeep and insurance.

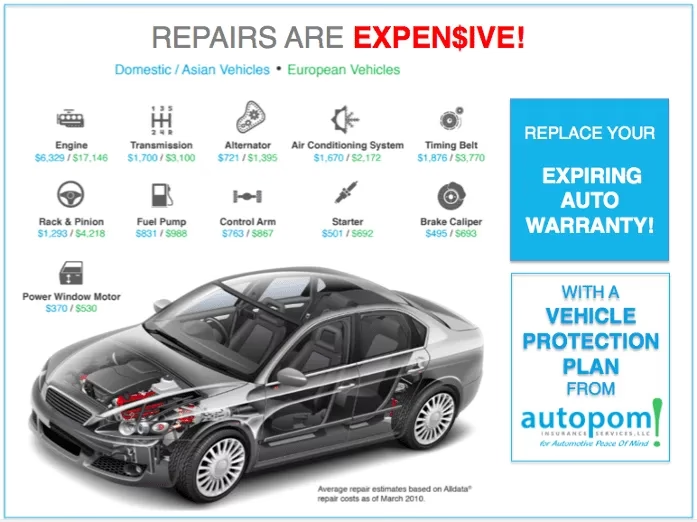

The Price Tag of Vehicle Repairs

Let's address the core of the inquiry: the cost of car repairs. The reality is that the price of fixing a vehicle can vary wildly, depending on the nature of the problem, the make and model of the car, and where you choose to have the work done. However, a general ballpark figure can be helpful. According to insights from bodies like the Australian Securities and Investments Commission (ASIC), the average vehicle repair job can set you back around $3,000. This figure, while an average, highlights the significant financial commitment that car ownership entails, especially when unexpected issues arise. For a new driver, who may be less experienced in identifying potential problems or may inadvertently cause minor damage, this average repair cost becomes a crucial figure to consider.

Understanding the Impact on Car Insurance

When an L or P plate driver gets behind the wheel, one of the immediate financial considerations is car insurance. This is an area where premiums can see a noticeable increase. Insurers often view younger drivers, particularly those under 25, as higher risk due to their limited driving experience. This elevated risk translates directly into higher car insurance premiums. It's not uncommon for insurers to charge more if you're adding a driver under 25 to your existing policy or taking out a new policy specifically for them. Key Factors Influencing Insurance Premiums for New Drivers:* Age: Drivers under 25 typically face higher premiums. * Driving Experience: Limited experience equates to perceived higher risk. * Vehicle Type: The make, model, and age of the car can affect costs. * Location: Where the car is primarily driven and parked can play a role. * Driving Record: Any previous accidents or traffic violations (even as a named driver) can impact the premium.

The Crucial Role of Third-Party Insurance

Beyond your own vehicle's protection, understanding the cost of damage to others is paramount. This is where third-party car insurance becomes not just important, but essential. If you or your child were to cause damage to another person's vehicle or property and you lack third-party cover, you would be personally liable for the full cost of repairs. ASIC's figure of $3,000 for an average repair job underscores the potential financial burden. Ensuring that your third-party cover is adequate and specifically accounts for your child as a driver is critical to avoid potentially crippling expenses.

Preparing for Excesses

Another aspect of car insurance that new drivers need to be aware of is the concept of excesses. Insurers often implement higher excesses for L and P plate drivers. An excess is the amount you agree to pay towards a claim before the insurer steps in. This can include a general excess and, specifically for younger drivers, an under-25s excess. It is vital that both you and your child understand precisely what these excesses are. Knowing the financial commitment you'll need to make in the event of a claim can help manage expectations and prevent surprises. Understanding Your Policy Excesses:

| Type of Excess | Description |

|---|---|

| General Excess | The standard amount you pay towards a claim. |

| Under-25s Excess | An additional amount charged by insurers for drivers under 25. |

| Young Driver Excess | Similar to under-25s excess, specifically for inexperienced drivers. |

| Named Driver Excess | An excess that may apply if a specific named driver (often a young one) causes a claim. |

Calculating Kilometres and Usage

For those who opt for usage-based insurance, such as pay-as-you-drive policies, the introduction of a new driver can significantly alter the cost calculation. It's essential to accurately assess how your child will use the car. Consider the following: * Purpose of Use: Will they be commuting to school, work, or social activities? * Distance Covered: How many kilometres do you anticipate they will drive weekly or monthly? * Parking Location: Where will the car be parked, especially overnight? Areas with higher crime rates might increase risk. * New Risks: Does their driving introduce any new risks, such as driving in unfamiliar areas or at night? By meticulously calculating projected kilometres and understanding the usage patterns, you can better estimate the impact on your insurance premiums and potentially find the most cost-effective solution.

Choosing the Right Individual Policy

If your L or P plater is looking to secure their own car insurance policy, it's crucial they understand the different types of cover available. While comprehensive insurance offers the broadest protection, it often comes with the highest premium. Depending on their budget and risk appetite, they might consider: * Third Party Fire and Theft: Covers damage to your car if it's stolen or damaged by fire, and also covers damage to other people's property. * Third Party Property Only: This is the most basic level of cover, protecting against damage to other people's vehicles or property, but not your own car. While more cover is generally better, the ultimate decision on the type of policy often rests with the individual driver. Your role as a parent is to educate them on the implications of each option, helping them to make an informed choice that balances cost with necessary protection.

Frequently Asked Questions

Q1: How much does a typical car repair cost for a new driver?A1: The average vehicle repair can cost around $3,000, but this can vary significantly based on the issue. For new drivers, minor incidents might lead to repairs for things like bumper scuffs or mirror replacements, which can range from a few hundred to over a thousand dollars. Q2: Will my car insurance premium increase if I add my child as a driver?A2: Yes, it is highly probable that your car insurance premium will increase. Insurers typically charge more for drivers under 25 due to their limited experience. Q3: What is an excess, and why is it higher for young drivers?A3: An excess is the amount you pay towards a claim. Insurers often impose higher excesses on young or inexperienced drivers because they are statistically more likely to be involved in an accident. Q4: Is third-party insurance really necessary?A4: Absolutely. Third-party insurance is essential to cover damage you might cause to other people's vehicles or property. Without it, you would be personally liable for these costs, which can be substantial. Q5: What's the cheapest car insurance option for a new driver?A5: Generally, third-party property damage insurance is the cheapest option. However, it offers the least amount of protection for the driver's own vehicle. It's important to weigh the cost savings against the level of cover required. In conclusion, while the question of car repair costs is broad, for parents of new drivers, it encompasses a wider financial landscape. From the potential $3,000 average repair bill to the increased insurance premiums and the crucial need for adequate third-party cover, understanding these costs is vital. By being informed and proactive, you can help your young driver navigate the road safely and responsibly, without unexpected financial shocks.

If you want to read more articles similar to New Driver Car Costs Revealed, you can visit the Automotive category.