21/06/2022

As a car owner in the UK, you're likely familiar with the essentials of car insurance. You pay your premiums, and in return, your insurer promises to cover you in the event of an accident, theft, or damage. But have you ever paused to consider what happens behind the scenes after your insurer pays out for a claim, especially when another party was at fault? This is where the often-overlooked yet incredibly important legal concept of subrogation comes into play. It's a fundamental principle that ensures fairness and efficiency within the insurance world, directly impacting how costs are managed and how claims are settled.

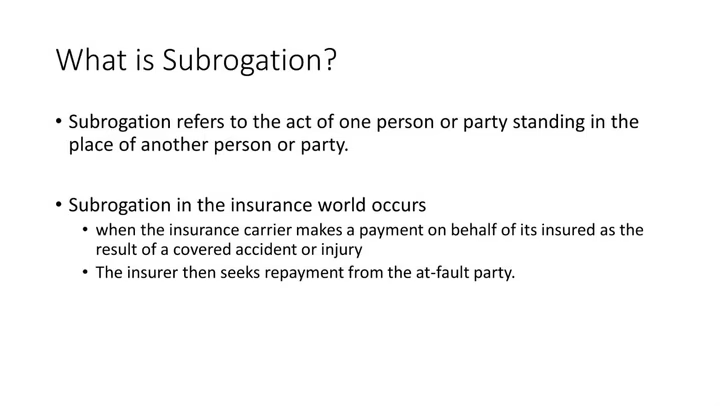

Subrogation is a legal mechanism that allows one party to step into the shoes of another, taking on their rights, remedies, or privileges. In the context of car insurance, it primarily means that once your insurer pays you for a loss, they acquire your right to pursue the responsible party for that same loss. It prevents you from being compensated twice for the same damage and ensures that the financial burden ultimately falls on the party legally responsible for the incident. Understanding subrogation isn't just for legal professionals; it offers valuable insight into your insurance policy and how claims are processed, which can empower you as a motorist.

- What Exactly is Subrogation?

- Why Subrogation Matters to UK Car Owners

- Types of Subrogation

- How Subrogation Works in Practice for Car Claims

- Benefits and Considerations of Subrogation

- Subrogation vs. Other Legal Concepts

- Frequently Asked Questions (FAQs)

- Does subrogation affect my No-Claims Bonus (NCB)?

- What if I've already been paid for damages by the at-fault party?

- Do I need to do anything during the subrogation process?

- Can my insurer subrogate if I caused the accident?

- What if the other party doesn't have insurance?

- Can I still claim for my uninsured losses (e.g., excess, personal injury) if my insurer subrogates?

- Conclusion

What Exactly is Subrogation?

At its core, subrogation is the substitution of one person or entity by another in respect of a debt or insurance claim, accompanied by the transfer of the rights and duties of the original creditor or claimant to the new one. Think of it as your insurer 'standing in your shoes' to recover the money they paid out to you from the person or company who caused the damage. This transfer of rights is crucial because it ensures that the person who was genuinely at fault is held accountable, rather than the insurance company simply absorbing the cost.

The concept is rooted in the principle of preventing unjust enrichment. Without subrogation, a policyholder could potentially recover damages from their insurer and then also from the at-fault party, resulting in them being compensated twice for the same loss. Furthermore, it allows insurers to recover their losses, which in turn helps to keep premiums more stable and fair for all policyholders. It's a cornerstone of the insurance industry, underpinning how claims are managed worldwide, including right here in the UK.

Why Subrogation Matters to UK Car Owners

For the average UK motorist, subrogation is most relevant in scenarios involving car accidents where another driver is to blame. Let's say you're involved in a collision, and the other driver is clearly at fault. Your car is damaged, and you need repairs. You file a claim with your own insurance company (perhaps under your comprehensive cover). Your insurer pays for the repairs to your vehicle. At this point, through subrogation, your insurer gains the right to pursue the at-fault driver (or their insurance company) to recover the money they paid out for your repairs.

This mechanism is vital for several reasons:

- Streamlined Claims Process: You get your vehicle repaired promptly by your own insurer, without having to wait for the at-fault party's insurer to agree to liability or for lengthy negotiations.

- Fairness: It ensures that the ultimate financial responsibility rests with the party who caused the damage, aligning with the principle of tort law.

- Cost Recovery: For insurers, it's a critical tool for recouping their losses, which contributes to the overall financial health of the insurance market and can indirectly influence premium levels.

- Protection of Your Rights: While your insurer takes over the right to claim for the damages they've paid, your rights for any uninsured losses (like your excess, personal injury, or loss of earnings) remain yours to pursue.

The Role of Car Insurance in Subrogation

Your car insurance policy contains clauses that grant your insurer the right of subrogation. This is usually a standard part of your terms and conditions. When you make a claim and your insurer indemnifies you (pays out your loss), you effectively transfer your right to sue the at-fault party to your insurer. This is a legal obligation once you accept the payout.

Consider a scenario: you're driving your car, and another driver runs a red light and crashes into you. Your car is a write-off. Your insurer pays you the market value of your vehicle. Simultaneously, they begin the subrogation process against the at-fault driver's insurance company to recover that payout. You, as the policyholder, don't need to get involved in this recovery process, as your insurer handles it on your behalf.

Beyond Accidents: Faulty Parts and Repairs

While most commonly seen in accident claims, subrogation can also apply in other automotive contexts, though less frequently. For example:

- If a new part installed during a repair turns out to be faulty and causes further damage, your insurer might cover the subsequent repairs. They could then subrogate against the part manufacturer or the garage that installed the faulty part to recover their costs.

- Should a warranty provider pay for a repair that was actually due to a third-party's negligence (e.g., a previous garage's poor workmanship causing a component failure), the warranty provider might subrogate against that negligent garage.

These scenarios highlight that subrogation isn't limited to vehicle collisions; it applies whenever one party pays for a loss that was ultimately the responsibility of another.

Types of Subrogation

In legal terms, subrogation generally falls into two main categories:

Legal Subrogation (or Equitable Subrogation)

This type of subrogation arises automatically by operation of law, without any express agreement between the parties. In the UK, this is the most common form of subrogation in insurance. Once an insurer pays a valid claim under the terms of the policy, the law automatically grants them the right to step into the policyholder's shoes to recover the loss from the responsible third party. There's no need for a specific clause in the policy or a separate agreement; it's an inherent right of the insurer.

Conventional Subrogation

This type of subrogation arises from an express agreement or contract between the parties. While less common in standard car insurance claims (where legal subrogation prevails), it might be seen in more complex financial arrangements or specific contractual agreements where one party agrees to pay a debt on behalf of another and, in return, is granted the right to pursue the original debtor. For example, if a finance company pays off a loan on a vehicle and then takes on the right to claim against a defaulting borrower, this would be a form of conventional subrogation.

How Subrogation Works in Practice for Car Claims

Let's break down the typical sequence of events in a car accident claim involving subrogation:

- The Incident: You're involved in an accident, and another driver is at fault.

- Reporting the Claim: You notify your own car insurance company of the incident and the damage to your vehicle.

- Assessment and Repair/Payout: Your insurer assesses the damage. If your car is repairable, they authorise repairs at an approved garage. If it's a write-off, they pay you the market value of your vehicle.

- The Subrogation Process Begins: Once your insurer has paid for the repairs or the vehicle's value, they will then initiate the subrogation process. They will contact the at-fault driver's insurance company to seek reimbursement for the costs they have incurred.

- Recovery: The two insurance companies will then negotiate. If liability is clear, the at-fault driver's insurer will reimburse your insurer. If there's a dispute over liability, it might lead to arbitration or, in rare cases, legal action between the insurers.

- No Direct Action from You: As the policyholder, you generally don't need to take any direct action against the at-fault party for the damages covered by your insurer. Your insurer handles this recovery process entirely.

It's important to cooperate fully with your insurer during this process. They may require information or statements from you to support their subrogation efforts. Failure to cooperate could, in extreme cases, impact your claim or future coverage.

Benefits and Considerations of Subrogation

Benefits:

- Reduced Financial Burden on Insurers: By recovering costs from responsible parties, insurers can manage their outgoings more effectively, which theoretically contributes to more stable insurance markets and competitive premiums.

- Justice and Accountability: It ensures that the party truly responsible for the damage bears the financial consequence, rather than the burden falling on innocent policyholders or the insurance collective.

- Efficient Claims Handling: It allows your insurer to pay your claim quickly, getting you back on the road sooner, without you having to directly pursue the at-fault party.

Considerations:

- Cooperation is Key: Your insurance policy will almost certainly include a clause requiring your cooperation in any subrogation efforts. This means providing statements, attending court if necessary (though rare), and not doing anything that might prejudice your insurer's ability to recover their costs.

- Avoiding Double Recovery: You cannot recover the same loss from both your insurer and the at-fault party. If you've already been paid by your insurer, your right to claim that specific loss from the at-fault party ceases.

- Impact on Excess: If your insurer successfully subrogates and recovers all costs from the at-fault party, they will typically reimburse you for any excess you paid towards your claim. This is a significant benefit for policyholders.

- No-Claims Bonus (NCB): While subrogation aims to recover costs, whether your NCB is affected depends on whether the claim is deemed 'fault' or 'non-fault'. If your insurer fully recovers their costs, your claim will often be classified as 'non-fault', protecting your NCB. However, if they cannot recover all costs (e.g., the other party is uninsured or untraceable), it may remain a 'fault' claim, impacting your NCB.

Subrogation vs. Other Legal Concepts

While subrogation involves the transfer of rights, it's distinct from other legal mechanisms:

| Mechanism | Description | Relevance to Car Owners |

|---|---|---|

| Subrogation | An insurer steps into your shoes to recover costs from the at-fault party after paying your claim. | Your insurer handles recovery; you get paid quickly and potentially your excess back. |

| Assignment of Rights | A complete transfer of a right (e.g., a debt) from one party to another. The original party no longer has the right. | Less common in standard claims; might occur in specific financial agreements related to vehicles. |

| Delegation | One party authorises another to perform an obligation on their behalf, but the original party remains responsible. | Not directly applicable to typical car insurance claims. More about contractual performance. |

Frequently Asked Questions (FAQs)

Does subrogation affect my No-Claims Bonus (NCB)?

Generally, if your insurer successfully recovers all their costs through subrogation, your claim will be classified as 'non-fault'. This means your NCB should not be affected. However, if they are unable to recover all costs (e.g., the at-fault party is uninsured or cannot be traced), the claim may remain 'fault', and your NCB could be impacted. Always check with your insurer for specifics regarding your claims history.

What if I've already been paid for damages by the at-fault party?

If you have already received compensation for your damages directly from the at-fault party or their insurer, you cannot then claim the same damages from your own insurer. Doing so would constitute 'unjust enrichment'. If your insurer pays you first, your right to claim from the at-fault party transfers to them.

Do I need to do anything during the subrogation process?

Typically, no. Your insurer handles the entire subrogation process. However, you have a contractual obligation to cooperate with your insurer. This might involve providing statements, answering questions, or supplying documents if requested. Your cooperation ensures your insurer has the best chance of recovering their costs.

Can my insurer subrogate if I caused the accident?

No. Subrogation only applies when another identifiable party is at fault for the damages your insurer has paid out for. If you caused the accident, your insurer will pay for the damages under your policy, but there will be no third party against whom they can subrogate to recover costs.

What if the other party doesn't have insurance?

If the at-fault party is uninsured, your insurer may still attempt to subrogate against them directly. However, recovering costs from an uninsured individual can be challenging and often unsuccessful. In such cases, your claim might be classified as 'fault' by your insurer, potentially affecting your NCB. Some policies offer uninsured driver cover, which can protect your NCB in such scenarios.

Can I still claim for my uninsured losses (e.g., excess, personal injury) if my insurer subrogates?

Yes. Subrogation only transfers your rights for the losses that your insurer has paid out for. Any uninsured losses, such as your policy excess, personal injury claims, loss of earnings, or other out-of-pocket expenses not covered by your policy, remain your right to pursue directly from the at-fault party or their insurer.

Conclusion

Subrogation, while a legalistic term, is a practical and essential component of the UK car insurance landscape. It’s the mechanism that allows your insurer to recover costs from the party responsible for your vehicle's damage, ensuring that the financial burden falls where it justly belongs. For you, the motorist, understanding subrogation means appreciating how your claims are managed efficiently, how your excess might be recovered, and how it contributes to the broader stability of insurance premiums. It underscores the importance of fully cooperating with your insurer after an incident, as their ability to subrogate effectively ultimately benefits the entire system and, indirectly, your own motoring costs.

If you want to read more articles similar to Subrogation: What UK Drivers Need to Know, you can visit the Insurance category.