19/03/2011

In the intricate world of business finance, certain acronyms stand out as beacons of a company's financial health. Among the most prominent is EBITDA – Earnings Before Interest, Taxes, Depreciation, and Amortisation. Often hailed as a robust indicator of operational profitability, EBITDA provides a clear snapshot of a business's capacity to generate cash from its core activities, before the impact of financing decisions, tax policies, or non-cash expenses. However, the term isn't always as straightforward as it seems. Just as there are different lenses through which to view a company's performance, there are variations of EBITDA, each serving a distinct purpose. This article delves into the critical differences between 'Standard EBITDA' and 'Restated EBITDA' (often referred to as 'EBITDA Retraité' or 'Reconstituted EBITDA' in some European contexts), helping you understand why these distinctions matter for business owners, investors, and financial analysts in the UK.

- Understanding Standard EBITDA: The Core Operational Metric

- Introducing Restated EBITDA: A Deeper Dive for Valuation

- Key Differences: Standard vs. Restated EBITDA

- EBITDA vs. Operating Profit: A Crucial Distinction

- The Gross Operating Result (RBE): An Adjusted View of Profit

- When and Why to Calculate These Metrics

- Key Financial Ratios Derived from EBITDA

- Limitations of EBITDA

- Conclusion

- Frequently Asked Questions (FAQs)

Understanding Standard EBITDA: The Core Operational Metric

Standard EBITDA is a widely used financial metric that provides a clear picture of a company's operational profitability. It is a key 'Intermediate Management Balance' (SIG - Solde Intermédiaire de Gestion in French, indicating its role in breaking down the profit and loss account) that highlights the wealth generated purely from a business's primary activities. Its power lies in its ability to strip away factors that can obscure core performance, such as how a company is financed (interest), its tax burden, and the accounting treatment of its assets (depreciation and amortisation).

What Standard EBITDA Represents

At its heart, Standard EBITDA reflects the gross cash flow generated by the company's operating cycle. It focuses solely on revenue and the direct costs associated with generating that revenue, deliberately excluding:

- Exceptional Expenses: One-off costs that don't relate to regular operations.

- Financing Costs: Interest paid on loans, which relates to the company's capital structure, not its operational efficiency.

- Investment and Amortisation Policies: Depreciation and amortisation are non-cash expenses reflecting the wear and tear or obsolescence of assets. While crucial for accounting, they don't represent actual cash outflows in the period they are expensed, nor do they reflect the operational performance itself.

- Taxes: The company's tax burden, which is influenced by government policy and accounting adjustments, not core operations.

By excluding these elements, Standard EBITDA confirms or refutes the viability of the company's business model based purely on its operational efficiency. It's a measure of raw, unlevered, and untaxed operating cash flow.

How Standard EBITDA is Calculated

Standard EBITDA can be calculated in a couple of primary ways, typically derived from the company's Profit and Loss (P&L) statement for a given period, usually a financial year:

Method 1: From Turnover (Revenue)

This is perhaps the most common approach, starting from the top line of the P&L:

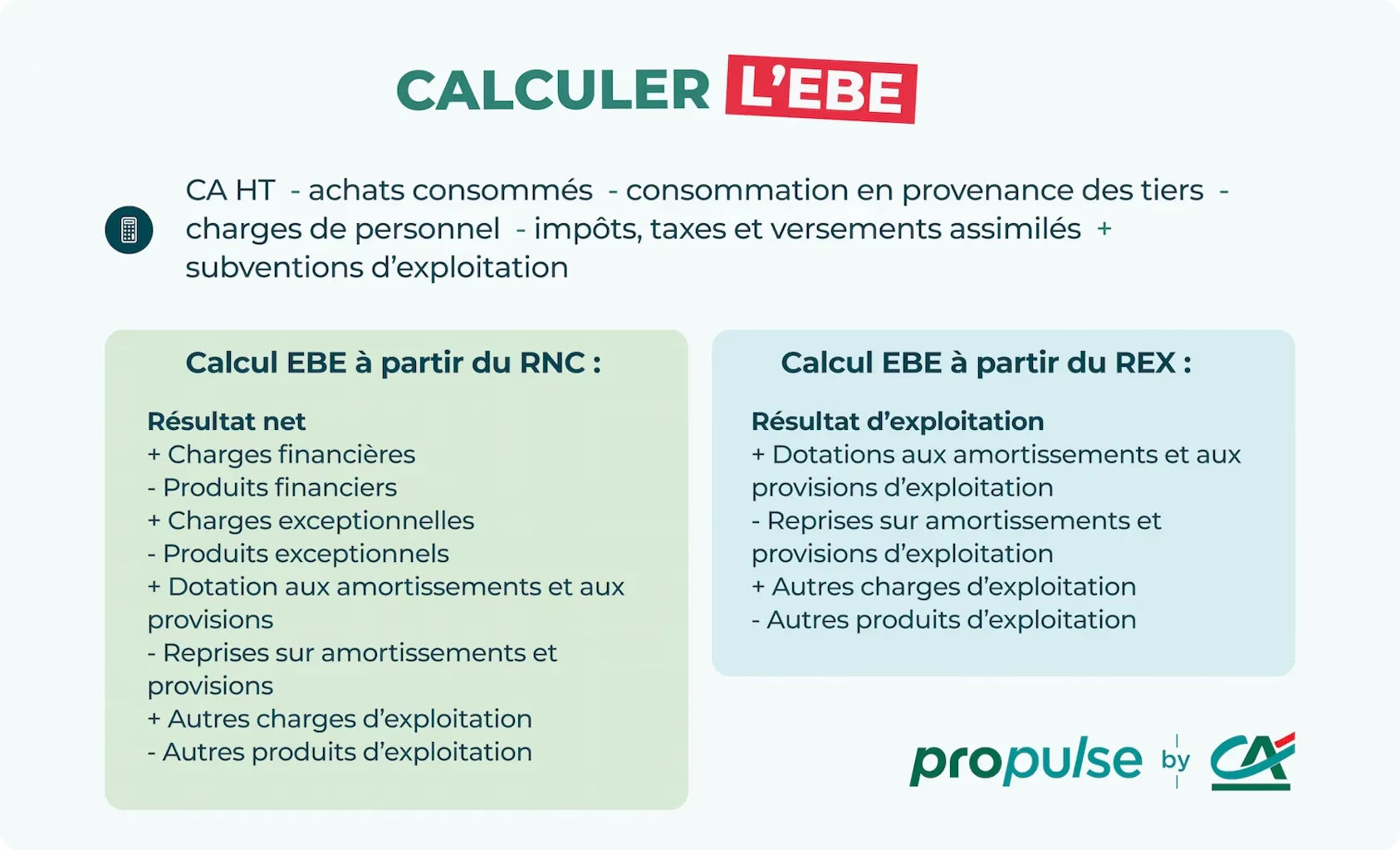

EBITDA = Turnover - Consumed Purchases - Third-Party Consumption + Operating Subsidies - Staff Costs - Taxes and Duties

- Turnover: Total sales revenue generated from the company's core operations.

- Consumed Purchases: The cost of raw materials and goods consumed in the production or sale process.

- Third-Party Consumption: Expenses for services from external providers (e.g., rent, utilities, professional fees).

- Operating Subsidies: Government grants or subsidies received for operational purposes.

- Staff Costs: Wages, salaries, social security contributions, and other employee-related expenses.

- Taxes and Duties: Operational taxes, but *not* income tax.

Method 2: From Value Added

This method builds upon the concept of 'Value Added', which represents the wealth created by the company through its own activities:

EBITDA = Value Added + Operating Subsidies - Taxes and Duties - Staff Costs

- Value Added: Turnover - Consumed Purchases - Third-Party Consumption. It's the contribution of the company's production to the economy.

- The remaining components are as described above.

Interpreting Standard EBITDA

A positive EBITDA indicates that the company's core operations are generating sufficient cash to cover its direct operating costs, suggesting a fundamentally healthy business model. Conversely, a negative EBITDA (sometimes referred to as an 'insufficiency of gross operating surplus') means that the company's turnover isn't even covering its direct operational expenses, indicating a significant challenge in its core business viability.

Introducing Restated EBITDA: A Deeper Dive for Valuation

While Standard EBITDA offers a robust view of operational performance, it doesn't always tell the whole story, especially when a business is being valued for sale or acquisition. This is where 'Restated EBITDA' (or 'EBITDA Retraité' / 'Reconstituted EBITDA') comes into play. This adjusted figure aims to provide a more accurate and comparable measure of a company's true earning potential, by eliminating the impact of specific expenses that are discretionary or unique to the current owner/management.

What Restated EBITDA Represents

Restated EBITDA is a crucial metric for evaluating and financing a company, particularly in mergers and acquisitions (M&A). Its primary purpose is to normalise the earnings, removing any biases introduced by the current owner's personal financial decisions or administrative policies. It seeks to answer the question: "What would the company's operational earnings be if it were run by a new, purely financially motivated owner?"

This adjusted figure often includes elements that a Standard EBITDA calculation would typically exclude, or it may re-add expenses that were previously considered operational but are, in fact, discretionary. It aims to represent the true 'surplus' available to service the owner's remuneration, personal debts, and other non-core expenses that might be run through the business.

How Restated EBITDA is Calculated

The calculation of Restated EBITDA is more complex and often requires close collaboration with an accountant, as it involves making specific adjustments to the reported figures. It typically starts from the net profit and adds back various items:

Restated EBITDA = Net Profit + Provisions + Amortisation + Salaries (including owner's discretionary salary) + Specific Charges (Expenses) + Various Benefits (e.g., personal use of company vehicles, excessive travel expenses, non-business related entertainment)

- Net Profit: The bottom line profit after all expenses, including interest and taxes.

- Provisions: Amounts set aside for future liabilities or losses.

- Amortisation: Non-cash expense for intangible assets.

- Salaries: Crucially, this often includes the owner's salary, especially if it's considered above market rate or includes a significant discretionary component.

- Specific Charges/Benefits: This is where the 'restatement' truly happens. It involves identifying and adding back any expenses that are not strictly necessary for the operation of the business but are incurred for the benefit of the current owner or related parties. Examples include:

- Excessive rent paid to an owner-related entity.

- Personal expenses charged to the company (e.g., luxury car for personal use, private health insurance).

- Non-market rate salaries paid to family members who are not actively involved in the business.

- One-off legal fees unrelated to core operations.

The idea is to arrive at a figure that reflects the underlying profitability of the business itself, unburdened by the specific administrative or personal financial policies of the current management. The allocation of this 'restated' surplus is then left to the discretion of a potential acquirer, who can decide how to structure their own remuneration and expenses.

Key Differences: Standard vs. Restated EBITDA

The distinctions between Standard and Restated EBITDA are fundamental, stemming from their differing purposes. While Standard EBITDA is about pure operational performance, Restated EBITDA is about valuation and comparability, stripping out owner-specific biases.

Here's a comparative overview:

| Feature | Standard EBITDA | Restated EBITDA |

|---|---|---|

| Primary Purpose | Assess core operational profitability and cash flow. | Normalise earnings for valuation and comparability (often for M&A). |

| Focus | Operational efficiency, excluding financing, tax, non-cash items. | True underlying earnings, free from owner-specific discretionary expenses. |

| Calculation Starting Point | Turnover or Value Added. | Net Profit (or Operating Profit), then adding back various items. |

| Key Inclusions/Exclusions | Includes operational revenue and direct operational costs. Excludes interest, taxes, depreciation, amortisation, exceptional items. | Includes all Standard EBITDA components, PLUS adds back owner's discretionary salaries, personal expenses, non-recurring costs, non-market rate related party transactions. |

| Complexity of Calculation | Relatively straightforward from P&L. | More complex, requires careful analysis and often accountant input to identify and justify adjustments. |

| User Base | Internal management, analysts, general investors. | Potential buyers, investors for M&A, business brokers, banks for acquisition finance. |

| Reflects | Raw operational cash generation. | A "normalised" profit figure, as if run by a purely commercial entity. |

The critical takeaway is that Standard EBITDA tells you how well the business runs day-to-day, while Restated EBITDA tells you what a buyer could realistically expect to earn from the business, independent of the current owner's personal choices.

EBITDA vs. Operating Profit: A Crucial Distinction

It's important not to confuse EBITDA with Operating Profit (also known as Operating Income or Earnings Before Interest and Taxes - EBIT). While both are profitability metrics, they serve different purposes and capture different aspects of a company's performance.

Here’s how they differ:

| Metric | Definition | Key Exclusions/Inclusions | What it Shows |

|---|---|---|---|

| EBITDA | Earnings Before Interest, Taxes, Depreciation, and Amortisation. | Excludes interest, taxes, depreciation, amortisation, and often exceptional items. | Gross operational cash flow; the ability to generate cash from core operations. |

| Operating Profit (EBIT) | Earnings Before Interest and Taxes. | Includes depreciation and amortisation. Excludes interest and taxes. | Profitability from core operations *after* accounting for the cost of assets (depreciation/amortisation). |

Operating Profit gives a more complete picture of a company's operational performance because it accounts for the cost of assets used in production through depreciation and amortisation. A company with significant capital expenditure will have a lower Operating Profit than its EBITDA, reflecting the wear and tear on its assets. EBITDA, by excluding these non-cash charges, can sometimes make a capital-intensive business appear more profitable than it truly is when considering the necessary reinvestment in assets.

The Gross Operating Result (RBE): An Adjusted View of Profit

The term 'Gross Operating Result' (RBE - Résultat Brut d'Exploitation) is another related financial indicator, often encountered in European accounting practices, which represents a further adjustment of the Operating Profit. Its aim is to provide insight into a company's investment policy and the age of its assets.

Calculation and Purpose of RBE

The RBE is typically calculated by taking the Operating Profit and adding back provisions and depreciation/amortisation:

RBE = Operating Products - Operating Charges (excluding provisions and depreciation/amortisation)

Or, more commonly, it's seen as Operating Profit adjusted for these non-cash items. The crucial insight from RBE comes from analysing the level of depreciation and amortisation:

- Low Depreciation/Amortisation: If these figures are low, it might imply that the company's machinery and assets are old and have been fully amortised for a long time. While this might lead to a higher immediate RBE (as less is deducted), it can also signal a lack of recent investment and potentially a weakening competitive position in the long term. The company might be prioritising immediate profitability over sustainable growth and innovation.

- High Depreciation/Amortisation: Conversely, high depreciation and amortisation indicate that the company is actively investing in new production assets. This might temporarily lower the Operating Profit and RBE (as more is deducted), but it signifies a commitment to modernisation and long-term competitiveness. These investments are crucial for future profitability and market relevance.

The RBE, therefore, serves as an indicator of a company's investment strategy. A positive RBE, especially when accompanied by healthy depreciation figures, suggests a balanced approach to profitability and long-term investment.

When and Why to Calculate These Metrics

The calculation of EBITDA, in both its standard and restated forms, is not just an academic exercise; it's a practical necessity for various business scenarios:

- Annual Financial Reporting: Standard EBITDA is a core component of intermediate management balances, offering a detailed breakdown of a company's annual performance.

- Forecasting and Budgeting: Businesses often project their EBITDA to set financial targets and assess future viability.

- Seeking Financing: Banks and investors heavily scrutinise a company's EBITDA when assessing loan applications or investment opportunities. A strong EBITDA signals a healthy cash-generating capacity, which is crucial for debt repayment. It's an indispensable figure in any robust business plan.

- Business Valuation and Sale: When a company is being bought or sold, Restated EBITDA becomes paramount. It helps potential buyers understand the true, normalised earning power of the business, allowing for fair valuation multiples. For instance, in specific industries like the acquisition of a retail business such as a newsagent or convenience store (akin to the 'tabac' example provided), EBITDA is often adjusted based on industry-specific benchmarks and coefficients (e.g., 2 to 4.5 times EBITDA) to determine a fair selling price. This process also considers the intangible value of the management team and customer relationships.

- Performance Analysis: EBITDA allows for comparison between companies, even those in different industries or with varying capital structures, by stripping away non-operational influences.

Key Financial Ratios Derived from EBITDA

EBITDA is not just a standalone figure; it's a foundation for other powerful financial ratios that offer deeper insights into a company's performance:

- Profitability Rate (EBITDA Margin):

EBITDA / Turnover (excluding VAT)

This ratio shows how much operational cash profit a company generates for every pound of sales. A higher percentage indicates greater operational efficiency. - Gross Profitability Rate:

EBITDA / Invested Capital

This ratio assesses the return generated on the capital invested in the business, highlighting how effectively assets are being utilised to generate operational earnings before finance costs and taxes.

Limitations of EBITDA

While incredibly useful, it's important to remember that EBITDA is not a panacea for financial analysis. It has limitations:

- Ignores Capital Expenditure: By excluding depreciation and amortisation, EBITDA doesn't account for the ongoing need to replace or upgrade assets. A high EBITDA might be misleading if the company is not reinvesting sufficiently in its infrastructure.

- Ignores Debt Servicing: It excludes interest payments, so it doesn't show whether a company can cover its debt obligations. A company can have a high EBITDA but still struggle if it has significant debt.

- Ignores Taxes: It doesn't account for the tax burden, which is a real cash outflow.

- Can Be Manipulated: Aggressive accounting practices can sometimes inflate EBITDA figures, making it crucial to scrutinise underlying financial statements.

Therefore, EBITDA should always be used in conjunction with other financial metrics, such as net profit, cash flow from operations, and debt-to-equity ratios, for a holistic view of a company's financial health.

Conclusion

Understanding the nuances of EBITDA is paramount for anyone involved in business finance. Standard EBITDA serves as an excellent barometer of a company's core operational strength, revealing its ability to generate cash from its primary activities. Restated EBITDA, on the other hand, provides a refined and normalised view of earnings, crucial for accurate business valuation and attracting investment, particularly in the context of mergers and acquisitions. By appreciating the specific purpose and calculation of each, you gain a far more sophisticated understanding of a business's true financial standing and future potential. Whether you're a business owner, an investor, or a financial professional, mastering these distinctions is a powerful step towards making more informed and strategic decisions.

Frequently Asked Questions (FAQs)

Q1: Why is EBITDA considered a 'cash flow' proxy if it's not actual cash flow?

EBITDA is often referred to as a cash flow proxy because it strips out non-cash expenses like depreciation and amortisation, as well as non-operational items like interest and taxes. This leaves a figure that is closer to the cash generated from core operations before these specific deductions. However, it's not a true cash flow statement because it doesn't account for changes in working capital (like inventory or accounts receivable/payable) or capital expenditures, which are real cash movements.

Q2: Can a company have a positive EBITDA but still be losing money?

Yes, absolutely. A company can have a positive EBITDA but still report a net loss. This happens if the interest expenses on its debt, its tax burden, or significant depreciation and amortisation charges (which are excluded from EBITDA) are high enough to outweigh the positive operational earnings. It highlights why looking at Net Profit and cash flow statements is also crucial.

Q3: When is Restated EBITDA most commonly used?

Restated EBITDA is most commonly used during the valuation process for the sale or acquisition of a business. It's particularly relevant for privately owned companies where the owner's personal expenses or discretionary decisions might be intertwined with the business's finances. It helps potential buyers see the true, underlying profitability without these owner-specific adjustments.

Q4: Is a higher EBITDA always better?

Generally, a higher EBITDA is seen as a positive sign, indicating strong operational performance and cash generation. However, it's not always "better" in isolation. It needs to be considered in context with the industry, the company's capital structure, and its reinvestment needs. For instance, a high EBITDA achieved by neglecting necessary capital expenditure might lead to long-term problems. Also, comparing EBITDA across different industries can be misleading due to varying capital intensity.

Q5: What are 'Intermediate Management Balances' (SIGs)?

Intermediate Management Balances (Solde Intermédiaire de Gestion or SIGs in French accounting) are a series of financial indicators derived from the Profit and Loss account that provide a step-by-step breakdown of a company's performance. They start from revenue and progressively deduct different categories of expenses to arrive at various levels of profit. EBITDA is one of these key balances, along with Commercial Margin, Value Added, Operating Profit, Financial Profit, Current Profit Before Tax, Exceptional Profit, and Net Profit. They help financial analysts understand the different layers of a company's profitability.

If you want to read more articles similar to Standard vs. Restated EBITDA: What's the Difference?, you can visit the Automotive category.