04/09/2011

As we navigate through the middle of 2025, the global crude oil market presents a puzzling paradox: prices are climbing, even as the OPEC+ alliance has announced a production increase set to commence in July. Brent crude, for instance, saw a notable dip in May, yet the overarching trend shows resilience, with WTI crude futures briefly approaching $62.50 per barrel. This counterintuitive rally is not a simple matter of supply and demand, but rather a complex interplay of market sentiment, the pre-pricing of bearish news, and, crucially, the renewed escalation of global geopolitical risks. Understanding this delicate balance is key to comprehending the current landscape of the oil market.

- The Supply Conundrum: OPEC+ Walks a Fine Line

- Disparate Demand Signals: A Mixed Global Picture

- Geopolitical Currents and Trade Winds: The Hidden Hand Behind the Rally

- Unpacking Recent Price Movements: The May 2025 Context

- Structural Changes in the Oil Market: A New Phase

- Navigating Volatility: A Forward Look

- Frequently Asked Questions

- Why did OPEC+ increase production if prices were already rising in mid-2025?

- How do tariffs, particularly from the U.S., impact global oil prices?

- Is the rise of Electric Vehicles (EVs) significantly affecting global oil demand in 2025?

- What are Natural Gas Liquids (NGLs) and why are they important to the future of oil supply?

- Will crude oil prices continue to rise throughout the rest of 2025?

The Supply Conundrum: OPEC+ Walks a Fine Line

The supply side of the equation is dominated by the strategic manoeuvres of OPEC+. At its June 2 meeting, the group agreed to raise output by 411,000 barrels per day (bpd) starting in July. While this was largely anticipated by the market, leading to a muted immediate price reaction, the more significant revelation was the extension of the voluntary 1.7 million bpd cuts – originally slated to conclude in 2024 – all the way through to the end of 2025. This decision critically reinforced the market’s medium-term narrative of a tight supply, effectively offsetting the impact of the near-term increase.

This marks the third consecutive month of OPEC+ pushing for production hikes, seemingly signalling confidence in a global economic recovery and a desire for market stability. However, a deeper look reveals a far more strategic calculus. Firstly, the output boost appears less about meeting burgeoning demand and more about a calculated effort to defend market share, particularly against the burgeoning output from U.S. shale producers and other non-OPEC sources. Saudi Arabia, a key player, seems to be pivoting from its traditional 'price stability via cuts' approach to a 'volume-based defence' strategy, aiming to preserve its long-term dominance.

Secondly, despite a broad consensus within the bloc, Russia expressed reservations about further increases, hinting at underlying internal divisions regarding the future price trajectory. Coordinating diverse interests across such a vast alliance remains a persistent challenge. OPEC+ also continues to utilise a compensation mechanism for members who overproduce, an attempt to foster transparency and discipline. Yet, this mechanism also highlights persistent issues with compliance, an aspect closely scrutinised by global markets.

Beyond OPEC+, other supply dynamics are also at play. In the United States, oil rig counts have notably declined for five consecutive weeks, hitting a 3.5-year low. This signals that producers are reacting to earlier weaker prices and rising operational costs, leading to a slowdown in shale growth. Concurrently, wildfires in Canada have led to partial shutdowns in oil sands production, further amplifying North American supply risks and bolstering market concerns about tightening output.

Disparate Demand Signals: A Mixed Global Picture

The demand landscape presents a mixed and uneven picture. In the United States, the onset of the peak driving season is triggering a predictable seasonal rebound in gasoline consumption. Data from gas station sales and traffic flow indicates an improving demand trend. Similarly, in the Middle East, extreme heat is driving up oil demand for power generation, offering marginal support to global consumption figures.

However, this optimistic trend is far from universal. China, the world’s largest crude importer, experienced stagnation in transportation and port throughput in April. More concerningly, gasoline and diesel sales saw year-over-year declines, and refinery run rates decreased. While China’s broader economy remains steady, its oil consumption is clearly losing steam. This slowdown is attributable to several factors, including the accelerating adoption of Electric Vehicles, ongoing price wars delaying new car purchases, and a broader industrial restructuring aimed at higher efficiency and less energy intensity. Chinese refiners are proactively cutting output, which has helped to draw down fuel inventories. However, this largely reflects short-term rebalancing rather than a genuine resurgence in demand, signalling persistent structural weakness in domestic consumption.

In India, despite robust economic growth, oil consumption has fallen short of bullish expectations. India's service-led economy consumes less energy per unit of GDP compared to China’s manufacturing-heavy model. This means that even with significant economic expansion, India’s marginal contribution to overall global oil demand may be relatively limited.

Perhaps the most significant catalyst behind oil’s recent resilience and unexpected rally lies in the escalating geopolitical risks. The renewed escalation of the Russia-Ukraine conflict has reignited fears of severe supply chain disruption, creating an immediate premium on crude prices due to heightened uncertainty.

Adding another layer of complexity, a proposal in the U.S. Senate to impose a staggering 500% tariff on countries importing Russian oil has dramatically altered global trade dynamics. This potential policy shift has generated far more immediate upside pressure on prices than the modest OPEC+ supply bump. Furthermore, the broader tariff policy of the Trump administration continues to cast a long shadow over the energy market. While core U.S. PCE inflation eased in April, trade volumes slumped sharply due to tariff-related disruptions. For example, steel tariffs doubled in a matter of weeks, underscoring the unpredictable nature of U.S. trade policy. More broadly, trade talks between the U.S. and key partners remain at a stalemate, with U.S.-China relations particularly strained. This uncertainty doesn’t merely affect goods flows; it poses latent risks to the energy market and price formation mechanisms, contributing significantly to price volatility.

Unpacking Recent Price Movements: The May 2025 Context

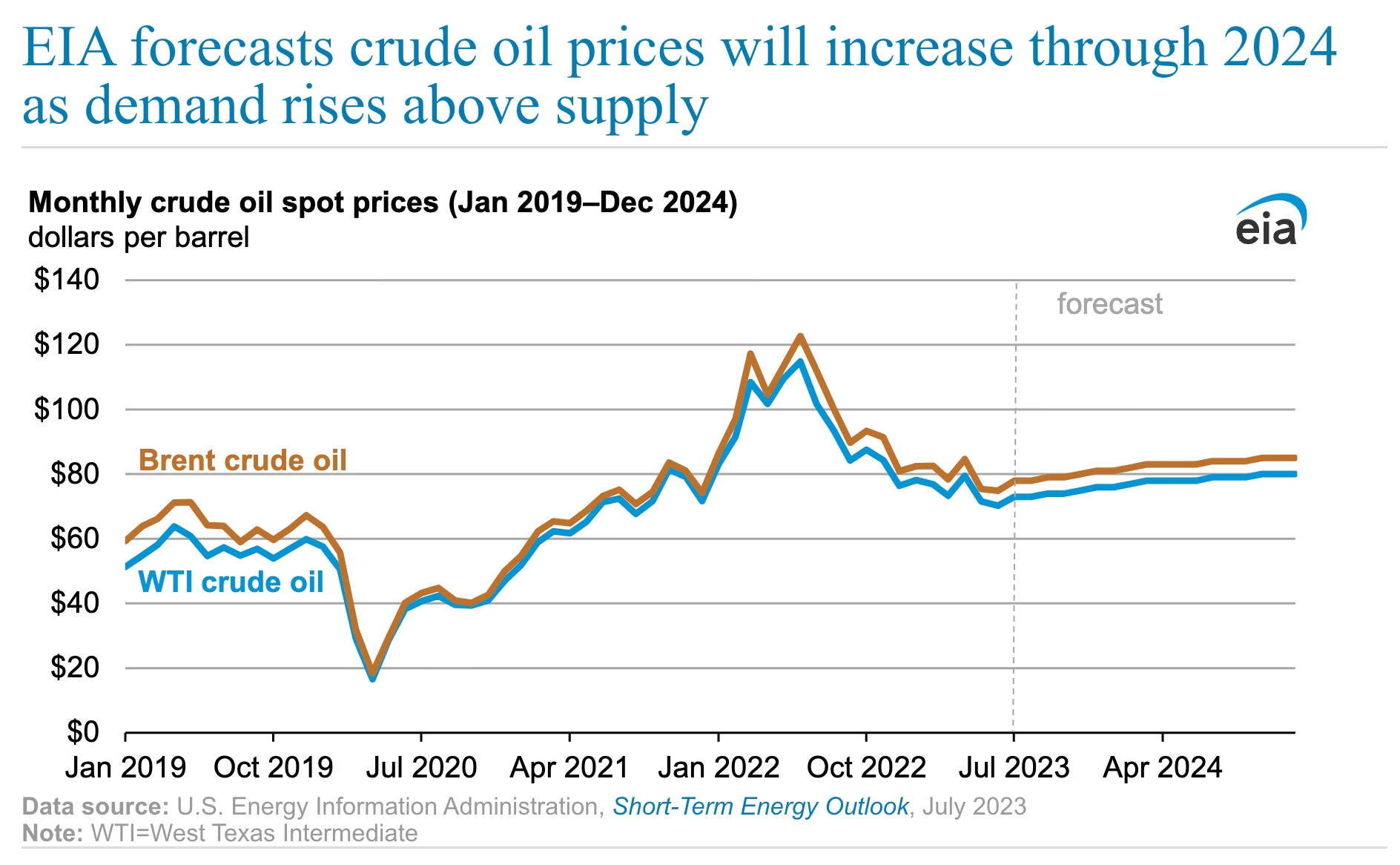

The month of May 2025 offered a sharp illustration of the market’s inherent contradictions. Brent crude oil prices actually decreased in May, averaging USD64.5/bbl month-on-month, a decline of USD3.7/bbl compared to April’s average. This marked the lowest point for oil prices since May 2021. This sell-off was primarily driven by the escalating U.S. tariffs and larger-than-expected OPEC+ output hikes, which collectively eroded the fuel demand outlook.

Global liquids demand in May increased only marginally by 0.3 MMb/d month-on-month, reaching 102.6 MMb/d. This minor increase, primarily from the Middle East and India, was largely offset by similar levels of demand decline in Japan and the United States. On the supply front, OPEC 9 production (excluding Iran, Venezuela, Libya) remained relatively stable, with a marginal increase of approximately 0.3 MMb/d to 27.4 MMb/d. Notably, eight OPEC+ members agreed to accelerate their production output hike, planning to increase cumulative volumes by an additional ~0.4 MMb/d in June.

Non-OPEC production (excluding U.S. shale) witnessed a slight decline of 0.3 MMb/d month-on-month, averaging 62.1 MMb/d in May, with major declines observed in Brazil, Canada, Kazakhstan, and China. U.S. shale production levels remained virtually unchanged month-on-month, averaging 9.2 MMb/d, with the number of active rigs standing at 553, down by twelve units compared to April 2025. Combined production levels in Iran, Venezuela, and Libya averaged 5.6 MMb/d during May 2025, showing no significant change in volumes.

Commercial inventories globally increased by approximately 97 million barrels in May, mainly driven by an increase in non-OECD inventories. Overall, inventories have remained relatively steady at around 4.5 billion barrels over the last six months. The prevailing market sentiment, amidst a weaker global economic outlook and declining oil demand, was further complicated by OPEC+'s decision for a second consecutive monthly production increase for June. This decision came despite falling benchmark crude oil prices in April and May, highlighting the bloc's complex strategy. Concurrently, stricter enforcement of sanctions on Venezuela, Iran, and Russia may counterbalance some of the production increases, adding another layer of uncertainty.

Structural Changes in the Oil Market: A New Phase

Beyond the immediate fluctuations, the global oil market is undoubtedly undergoing significant structural changes. The International Energy Agency (IEA) in its 'Oil 2025' medium-term outlook, suggests that global oil supply increases are set to far outpace demand growth in the coming years. This report highlights that the key drivers of supply and demand growth over the past 15 years are beginning to fade.

China, which has spearheaded global oil demand growth for over a decade, is now projected to see its consumption peak in 2027. This shift is primarily due to a surge in electric vehicle sales and the continued deployment of high-speed rail and trucks running on natural gas. Simultaneously, U.S. oil supply growth is expected to decelerate as companies prioritise capital discipline over aggressive expansion, although the United States remains the single largest contributor to non-OPEC supply growth.

Between 2024 and 2030, global oil demand is forecast to increase by a modest 2.5 million bpd, reaching a plateau of around 105.5 million bpd by the end of the decade. In contrast, global oil production capacity is forecast to surge by more than 5 million bpd to 114.7 million bpd by 2030. This growth will be dominated by robust gains in natural gas liquids (NGLs) and other non-crude liquids. This strategic shift towards higher non-crude capacity is driven by strong global demand for Petrochemicals feedstocks and the development of liquid-rich gas resources.

Despite OPEC+ beginning to unwind production cuts, the IEA report finds that increased output from the United States, Canada, Brazil, Guyana, and Argentina is projected to be more than sufficient to cover the growth in global demand. This suggests a comfortably supplied oil market through 2030, assuming no major supply disruptions, though significant uncertainties persist due to rising geopolitical risks and heightened trade tensions.

The accelerating sales of electric cars, which hit a record 17 million in 2024 and are on track to surpass 20 million in 2025, are a major factor keeping a peak in global oil demand on the horizon. By the end of the decade, electric vehicles are set to displace a total of 5.4 million bpd of global oil demand. The replacement of oil with natural gas and renewables for power generation in the Middle East, particularly Saudi Arabia, is also expected to temper global oil demand growth.

The petrochemical industry is poised to become the dominant source of oil demand growth from 2026 onwards, projected to consume one in every six barrels of oil by 2030. Since petrochemicals are largely produced from non-refined products like NGLs, these trends will increasingly impact the refining sector. The report forecasts net refinery capacity far exceeding demand for refined products by 2030, likely leading to more capacity shutdowns.

Key Factors Influencing Mid-2025 Oil Prices

| Factor Category | Specific Influence | Impact on Prices |

|---|---|---|

| Supply Dynamics | OPEC+ extended cuts (1.7m bpd) | Upward pressure (long-term tight supply narrative) |

| OPEC+ production increase (411k bpd) | Downward pressure (short-term supply boost) | |

| Declining US oil rig counts | Upward pressure (slower shale growth) | |

| Canadian wildfires (supply disruptions) | Upward pressure (North American supply risks) | |

| Demand Dynamics | US peak driving season | Upward pressure (seasonal gasoline demand) |

| Middle East heat (power generation) | Upward pressure (marginal support) | |

| China's slowing oil consumption (EVs, restructuring) | Downward pressure (structural weakness) | |

| India's moderate oil demand growth | Neutral to slightly downward (less energy-intensive growth) | |

| Geopolitical Factors | Russia-Ukraine conflict escalation | Significant upward pressure (supply chain disruption fears) |

| US 500% tariff proposal on Russian oil imports | Significant upward pressure (fresh trade complexity) | |

| Broader US trade policy/tariffs | Uncertainty, potential downward pressure (slumped trade volumes) | |

| Market Sentiment | Pre-pricing of bearish news | Offsetting negative fundamentals |

| Heightened volatility | Erratic price movements |

In the short term, oil prices appear supported by seasonal demand and the ongoing geopolitical risks, demonstrating a degree of downside resilience. However, over a longer horizon, OPEC+'s gradual easing of cuts could lead to increasing supply pressure into 2025 and beyond. While sanctions and cost challenges continue to cap output in countries like the U.S., Iran, and Venezuela, the pace and tone of global supply largely remain in the hands of OPEC+.

On the demand side, seasonal strength aside, China’s slowdown and India’s underperformance have fostered greater caution regarding the long-term consumption outlook. When coupled with the rising weight of geopolitical tension and trade barriers, the result is an increasingly volatile oil market. The crude market has entered a new phase characterised by heightened volatility, with sentiment swinging rapidly between competing narratives: geopolitical risks, macroeconomic uncertainties, and evolving supply-demand dynamics. For many analysts, this environment suggests a 'sell the rally' strategy, particularly for short-term price spikes driven more by sentiment or headlines than solid fundamentals.

Future Outlook and Strategic Considerations

Demand Projections: While renewable energy is undeniably on the rise, oil is expected to remain a significant energy source in the near to medium term, especially in industries where alternatives are not yet viable. However, technological advancements in energy storage and electric transportation could accelerate the shift away from oil, potentially reducing long-term demand more swiftly than anticipated.

Supply Considerations: Underinvestment in new oil projects, driven by lower prices or environmental concerns, could lead to future supply shortages, potentially pushing prices upwards. Conversely, enhanced recovery techniques could increase supply from existing fields, affecting overall supply dynamics.

Price Volatility: Ongoing uncertainties, including persistent geopolitical tensions and uneven global economic recovery patterns, are highly likely to contribute to continued price volatility. Additionally, countries may utilise strategic petroleum reserves to stabilise domestic markets, which can influence global supply and price levels.

Strategies for Stakeholders

For Investors: In a volatile market, diversification of portfolios can serve as a hedge against oil price fluctuations. Furthermore, the growing opportunities in renewable energy sectors present increasingly attractive alternative investment avenues.

For Policymakers: Developing comprehensive energy policies that balance economic growth with environmental sustainability is paramount for national energy security. Engaging in international collaboration and dialogues to manage oil supply and promote market stability benefits all stakeholders globally.

For Industry Players: Oil companies must adapt and innovate by investing in renewable energy and developing cleaner technologies. Enhancing operational efficiency is also crucial to reduce costs and improve competitiveness within a volatile market landscape.

Frequently Asked Questions

Why did OPEC+ increase production if prices were already rising in mid-2025?

OPEC+ announced a production increase primarily as a strategic move to defend market share against non-OPEC producers like U.S. shale. While it adds short-term supply, the simultaneous extension of long-term voluntary cuts reinforces a 'tight supply' narrative, which, combined with geopolitical risks, allows prices to climb despite the immediate increase.

How do tariffs, particularly from the U.S., impact global oil prices?

U.S. tariffs, such as the proposed 500% tariff on Russian oil imports or broader trade tariffs, introduce significant uncertainty and can disrupt global trade flows. This uncertainty creates an immediate risk premium on oil prices, as markets anticipate potential supply restrictions or demand slowdowns due to economic friction. Even if not directly on oil, tariffs can impact overall economic activity and, consequently, oil demand.

Is the rise of Electric Vehicles (EVs) significantly affecting global oil demand in 2025?

Yes, the accelerating adoption of Electric Vehicles is a major factor in the structural changes of oil demand. The IEA forecasts that EVs will displace 5.4 million bpd of global oil demand by 2030, and China's oil consumption is expected to peak by 2027 largely due to EV sales and shifts in transportation methods. While the immediate impact is gradual, the long-term trend is significant.

What are Natural Gas Liquids (NGLs) and why are they important to the future of oil supply?

Natural Gas Liquids (NGLs) are hydrocarbons that are often extracted alongside natural gas. They include ethane, propane, butane, and natural gasoline. The IEA forecasts that growth in global oil production capacity by 2030 will be dominated by NGLs and other non-crude liquids. This is crucial because NGLs are increasingly used as feedstocks for the petrochemical industry, which is becoming the dominant source of oil demand growth, shifting the focus away from traditional crude refining.

Will crude oil prices continue to rise throughout the rest of 2025?

The outlook for the remainder of 2025 suggests continued volatility. While short-term prices may be supported by seasonal demand and geopolitical risks, the long-term picture indicates potential rising supply pressure from OPEC+ gradually easing cuts and robust non-OPEC+ growth. However, persistent geopolitical tensions, trade barriers, and an uneven global economic recovery will likely contribute to significant price fluctuations, making a sustained, linear rise unlikely without major unforeseen supply disruptions.

If you want to read more articles similar to Mid-2025 Oil Price Surge: Geopolitics & Shifting Sands, you can visit the Automotive category.