14/04/2023

The FTSE 100 index, a cornerstone of the UK stock market, has certainly endured a tumultuous year. Despite hitting a new all-time high earlier in 2025, the journey has been far from smooth, with many of its constituent shares experiencing notable declines. However, as the dust begins to settle and early April's market mayhem subsides, a compelling question emerges for investors: could some of these shares potentially surge much higher in the future?

The FTSE 100: A Snapshot of the UK's Elite

Comprising the 100 largest companies listed on the London Stock Exchange by market capitalisation, the FTSE 100 is a globally recognised benchmark. These are typically well-established entities boasting strong brand recognition, significant economies of scale, and proven business models. They are also often reliable dividends payers, providing a steady income stream to investors.

In 2024, the index delivered a total return of 9.7%, marking its best performance since 2021, when it saw an impressive 18.4% return. While it underperformed the S&P 500, which posted a 25% total return in the same period, it's crucial to note the FTSE 100's historical resilience in more challenging economic climates. For instance, in 2022, when the S&P 500 fell, the UK's premier index managed to eke out a 1% gain.

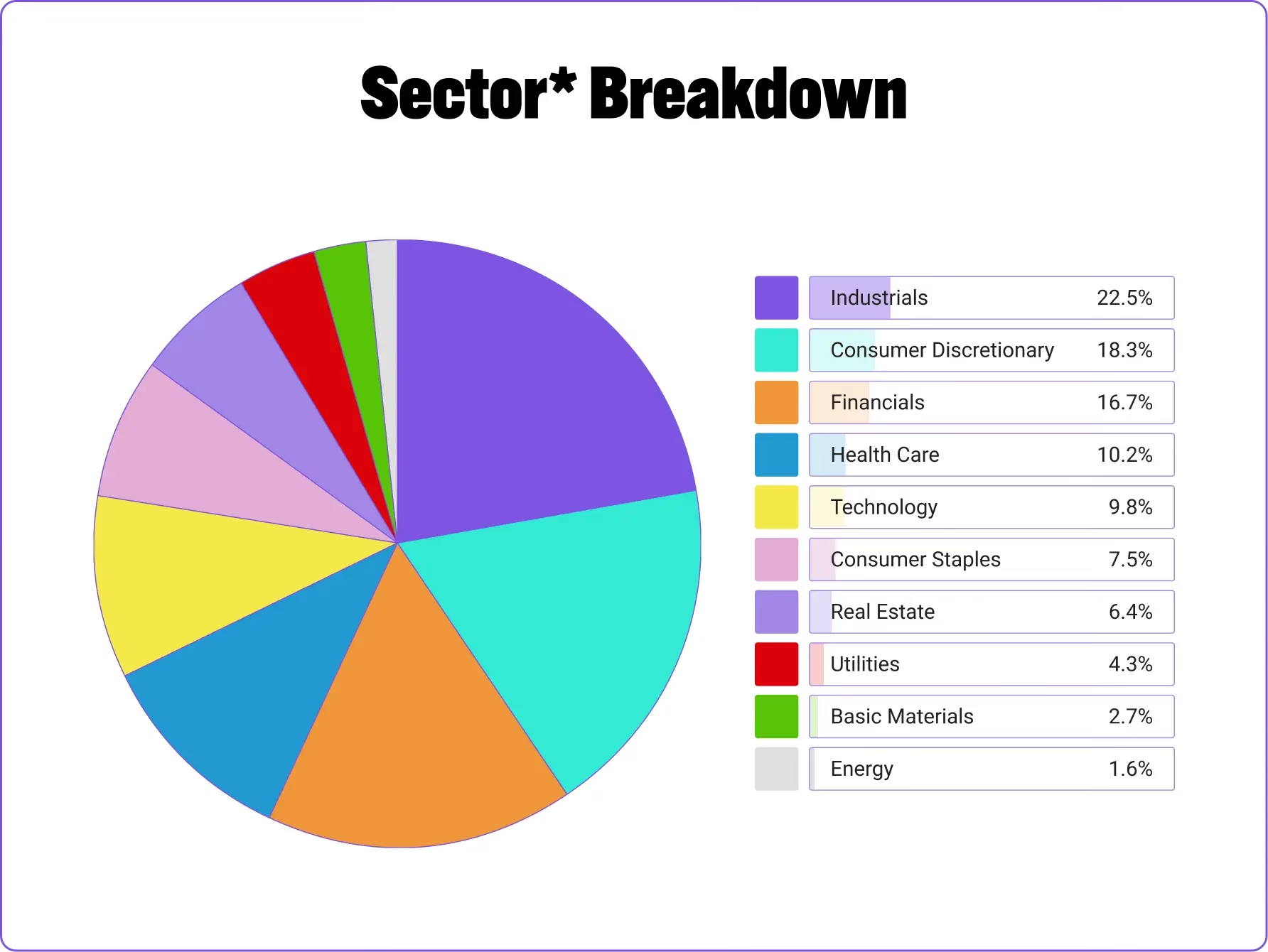

A distinctive characteristic of the FTSE 100 is its relatively low exposure to technology stocks compared to its US counterparts. Instead, it has a bias towards 'old economy' sectors such as raw materials, banking, and energy. Furthermore, approximately three-quarters of FTSE 100 corporate income is derived from overseas, making the index a significant play on global economic health, albeit with currency exchange rate considerations.

Potential Drivers for Future Upside

Despite the recent volatility, several factors suggest that the FTSE 100, or at least some of its components, could indeed experience significant upward movement.

1. Compelling Recovery Narratives

Some shares have been heavily 'beaten down' but are now showing signs of recovery, still trading well below their previous highs. Take Greggs (LSE: GRG) as a prime example. While its share price has climbed over 20% since early this month, it remains 23% below its year-start valuation. This doesn't guarantee a return to previous levels, as some falling shares continue their decline, but for fundamentally sound businesses, it presents an opportunity.

Greggs, with its strong brand, extensive network of over 2,600 shops, and compelling value proposition for budget-conscious consumers, appears to be undervalued by the market in the view of some analysts. Its recent trading update reported a 7% year-on-year sales growth for the first 20 weeks of the year, affirming the board's positive outlook. While increased wage costs and potential shifts in demand due to warmer weather pose risks, the underlying business strength could propel these shares higher.

2. Strong Growth Opportunities

Beyond recovery stories, there are companies that are already performing exceptionally well but possess significant further growth potential. Games Workshop (LSE: GAW) is a prime illustration. This company has been a long-time favourite among retail investors, and for good reason. Its share price is up 21% this year and a staggering 138% over five years, recently hitting an all-time high. Coupled with frequent dividends and a 3% yield, its appeal is clear.

While its price-to-earnings (P/E) ratio of 30 is not low, and risks like pricy products in a weak economy or concentrated manufacturing exist, Games Workshop's unique intellectual property (IP) and fiercely loyal fanbase provide massive competitive advantages. Recent trading updates confirm a strong start to 2025, leading to raised full-year expectations. Furthermore, the company continues to expand into high-profit margin areas such as licensing its IP. Media deals could further amplify the popularity of its game franchises, directly boosting profits and potentially propelling the share price upwards.

3. The Resurgence of 'Old Economy' Sectors

London's stock market has been held back in recent years by its bias towards traditional sectors. However, this weakness is increasingly being seen as a strength. Commodities, as real assets, become highly attractive during periods of persistent inflation, offering a hedge against rising prices. Similarly, the 'higher-for-longer' interest rate environment has provided a significant boost to bank profits.

Energy giants like Shell and BP alone account for roughly a fifth of all FTSE 100 profits. Analysts suggest that a 10% rise in oil prices could translate into a two percentage point rise in overall FTSE 100 profit growth, highlighting the significant leverage these sectors provide to the index's performance.

4. Favourable Political & Valuation Dynamics

The prolonged uncertainty following the 2016 Brexit referendum led global investors to attach a higher risk premium to UK equities, meaning they were only willing to buy them at a discount. However, calmer political waters in Britain and increased turbulence overseas suggest that this 'Brexit risk premium' may now be disappearing. With a general election date set, investors appreciate the increased certainty, with little significant macroeconomic difference between the main parties.

Crucially, UK stocks continue to trade near a record-low discount compared to other developed markets, despite paying twice the dividend available in many comparable markets. The FTSE 100's current price/earnings (P/E) multiple of 11.4 times is also well short of its long-run average of 12.8 times since 1987, suggesting attractive valuations relative to historical norms.

5. The Interest Rate Outlook

The Bank of England's latest cycle of rate increases, which concluded in August 2023, was relatively brief. There is a general expectation that the Bank of England has started, or will soon start, to cut interest rates. Lower interest rates typically make equities more attractive relative to bonds, providing a supportive backdrop for stock market performance as borrowing costs for businesses decrease and consumer spending potentially increases.

While the outlook presents several reasons for optimism, it's crucial to acknowledge the potential headwinds that could limit the FTSE 100's ascent.

1. Limited Exposure to Technology

The FTSE 100's low exposure to the technology sector, particularly the 'AI mania' gripping global markets, has been a significant factor in its underperformance compared to indices like the S&P 500. As enthusiasm for technology stocks wanes, this might become less of a disadvantage, but it remains a structural difference.

2. Slow Earnings Recovery Forecast

Despite recent positive sentiment, some forecasts paint a cautious picture for earnings. UBS Global Wealth Management, for instance, anticipates a further 3% decline in corporate profits this year, followed by only 5% growth in 2025. This slow recovery is attributed to factors such as softer commodity prices, disappointing sales to China, and risks to global growth stemming from higher trade tariffs, particularly under a new US administration.

3. Global Economic & Political Risks

Potential US headwinds, including the risk of a Trump presidency leading to increased tariffs and higher US bond yields, could dampen global growth and consequently impact FTSE 100 companies with significant international exposure. Furthermore, the spectre of stagflation – a combination of high inflation and stagnant economic growth – could also weigh on market sentiment and corporate profitability.

4. Sector Concentration Vulnerabilities

The FTSE 100's reliance on financials and energy sectors, while currently seen as a strength, also presents vulnerabilities. Earnings in these sectors could be at risk from sustained weak oil and gas prices or further significant falls in interest rates, which could compress bank profit margins.

5. Strong Pound Impact

While a strong pound indicates economic health, it can act as a headwind for the profits of FTSE 100 multinationals. Since a large proportion of their income is generated in foreign currencies, a stronger sterling reduces the value of these earnings when converted back into pounds.

Beyond the Blue Chips: The FTSE 250 and Beyond

Interestingly, some experts suggest that the baton of market success could yet pass from the FTSE 100 to the mid and small-cap companies of the FTSE 250. These domestically focused firms could benefit significantly from a stronger pound, as their money goes further when sourcing imports. Additionally, they are poised to gain from eventual interest rate cuts and a modestly improving domestic economic outlook.

Analysts at Killik & Co note that small and mid-caps are currently trading at significant discounts to large caps, identifying 'particular value' in UK small and mid-cap opportunities. UBS is also more optimistic on the FTSE 250, viewing it as well-positioned to benefit from targeted growth in domestic spending, infrastructure, and innovation, and offering a degree of insulation from currency and trade risks.

Expert Perspectives and Forecasts

The sentiment surrounding the FTSE 100 is evolving. Lucy Raitano of Reuters suggests that Britain's stock market might finally be shaking off years of underperformance. Bastien Bouchaud in Les Echos echoes this, stating that London's bias towards 'old economy' sectors is turning into a strength.

Lilia Peytavin from Goldman Sachs highlights the significant impact of commodity prices, noting that a 10% rise in oil prices translates into a two percentage point rise in FTSE 100 profit growth. Steve Magill of UBS Asset Management believes the Brexit risk premium has largely disappeared, contributing to a more positive outlook from global fund managers, as noted by Farah Elbahrawy and Naomi Tajitsu on Bloomberg.

UBS Global Wealth Management maintains a neutral stance on UK equities, forecasting the FTSE 100 to be slightly higher at approximately 8,200 by year-end 2025. They project an upside scenario of 9,800, contingent on higher commodity prices, better global growth, and a weaker sterling. Conversely, a pessimistic scenario warns of a retreat towards 6,600 if persistently high inflation forces the Bank of England to keep rates higher for longer, impacting valuations and growth.

They advise broad-based exposure to the UK market, with a tilt towards European sector preferences such as IT, consumer staples, and utilities, citing attractive relative value and positioning to benefit from falling inflation and lower interest rates.

FTSE 100 Performance: A Comparative View

To put the FTSE 100's performance into context, consider how a hypothetical £100 investment would have fared over the past decade compared to other major global indices:

| Index | £100 invested 10 years ago (approx.) |

|---|---|

| FTSE 100 | £177 |

| EuroStoxx 50 | £228 |

| Japan's TOPIX | £243 |

| S&P 500 | £455 |

This table illustrates that while the FTSE 100 has delivered positive returns, it has significantly lagged its international counterparts over the past decade. This gap highlights the potential for 'catch-up' if the current favourable conditions persist.

Frequently Asked Questions (FAQs)

What factors most influence FTSE 100 performance?

The FTSE 100 is influenced by a multitude of factors, including global economic growth, commodity prices (given its heavy weighting in energy and mining), interest rate expectations from the Bank of England, currency exchange rates (due to the international earnings of its constituents), and investor sentiment towards UK assets.

Is the FTSE 100 considered undervalued currently?

Based on its price-to-earnings (P/E) multiple of 11.4 times, which is below its long-run average of 12.8 times, and its high dividend yield compared to other developed markets, many analysts suggest the FTSE 100 trades at an attractive discount. However, this depends on individual company fundamentals and future earnings growth.

How does the FTSE 100 compare to other global indices?

Historically, the FTSE 100 has often lagged growth-oriented indices like the S&P 500, particularly during periods of high technology sector growth. However, it has demonstrated resilience in more adverse economic conditions and offers a distinct exposure to 'old economy' sectors and strong dividend payers, making it a valuable diversifier in a global portfolio.

The decision to invest depends on your individual financial goals, risk tolerance, and investment horizon. While there are compelling arguments for potential upside in the FTSE 100 due to attractive valuations, recovering businesses, and a favourable shift in sentiment, risks remain. It's always advisable to conduct thorough research or consult a financial advisor before making any investment decisions, remembering that capital is always at risk.

Conclusion

The FTSE 100 presents a complex yet intriguing picture for investors looking ahead. While it has faced its share of turbulence and structural headwinds, particularly its lower exposure to high-growth tech sectors, there are clear indications that some of its constituent shares could indeed move significantly higher. The confluence of compelling recovery stories, robust growth opportunities within established businesses, a potential resurgence of 'old economy' sectors, more favourable political and valuation dynamics, and the prospect of interest rate cuts all contribute to a cautiously optimistic outlook. However, global economic risks, a slow earnings recovery, and sector concentration vulnerabilities mean that careful selection and a balanced perspective remain paramount. As always, successful investing hinges on meticulous research and an understanding of the nuanced forces at play in the market.

If you want to read more articles similar to FTSE 100: Will UK Blue Chips Continue to Climb?, you can visit the Automotive category.