21/08/2021

In the evolving landscape of car ownership and leasing, a lesser-known but increasingly popular option for obtaining a new vehicle is the salary sacrifice scheme. While not universally available – typically offered as part of an employer’s benefits package – it presents a unique pathway to a brand-new car, often with considerable financial advantages. For many, it’s a compelling alternative to traditional leasing or outright purchase, allowing monthly payments for the car to be deducted from your salary *before* tax is applied. This pre-tax deduction is where the primary financial appeal lies, potentially leading to significant savings compared to funding a car yourself after your income has already been taxed. But how exactly does it work, and what are the crucial tax implications you need to understand before diving in?

- What is a Salary Sacrifice Car Scheme?

- Understanding Benefit-in-Kind (BIK) Tax

- The Electric Advantage: Why EVs Shine in Salary Sacrifice

- Is a Salary Sacrifice Car Scheme Worth It for You?

- Potential Pitfalls and Considerations

- Calculating Your Potential Savings

- Impact on Pensions and National Insurance

- Frequently Asked Questions (FAQs)

- Conclusion

What is a Salary Sacrifice Car Scheme?

At its core, a salary sacrifice car scheme is a formal agreement between you, your employer, and a third-party vehicle supplier. Instead of you paying for a car directly from your net income, your employer facilitates the payment by deducting a pre-agreed monthly amount from your gross salary. This effectively lowers your taxable income, meaning you pay less Income Tax and National Insurance (NI) contributions. It's vital to distinguish this from a traditional 'company car' where the employer pays for and is responsible for the vehicle; with salary sacrifice, while your employer facilitates the payment, you are the one responsible for the car and its running costs.

The beauty of this arrangement is that your gross pay is reduced by the cost of the car, and then tax and NI are calculated on that lower amount. This immediately provides a saving on your tax liabilities. However, it's not a completely tax-free ride, as the benefit of having a car through this scheme is still subject to a specific tax known as Benefit-in-Kind (BIK).

Understanding Benefit-in-Kind (BIK) Tax

Even though you contribute to the cost of the car via salary sacrifice, the UK tax authorities view the use of the vehicle as a 'benefit' provided by your employer. Consequently, this benefit is taxed under the Benefit-in-Kind (BIK) system, similar to how traditional company cars are taxed. This additional tax is typically charged monthly and is calculated based on several key factors:

- The P11D Value of the Car: This is the car's list price, including VAT, delivery charges, and any optional extras, but excluding the first year's Vehicle Excise Duty (VED) and registration fee.

- The Car's CO2 Emissions: This is arguably the most significant factor, as lower emissions lead to lower BIK rates.

- Your Personal Income Tax Bracket: The BIK charge is applied at your marginal tax rate (e.g., 20% for basic rate taxpayers, 40% for higher rate, 45% for additional rate).

The BIK percentage rate is determined by the car's CO2 emissions. The lower the emissions, the lower the percentage. This is where the landscape for electric vehicles (EVs) truly shines, offering substantial tax advantages.

The Electric Advantage: Why EVs Shine in Salary Sacrifice

For those considering a salary sacrifice car, electric vehicles, including Battery Electric Vehicles (BEVs) and Plug-in Hybrid Electric Vehicles (PHEVs), represent the most cost-effective choice. The UK government has actively incentivised the adoption of greener transport through significantly lower BIK rates for low-emission vehicles. This makes EVs, which might otherwise seem more expensive upfront, surprisingly affordable through a salary sacrifice scheme.

Let's look at the BIK rates:

| Vehicle Type | CO2 Emissions (g/km) | BIK Rate (2024-25 Tax Year) | Outlook |

|---|---|---|---|

| Battery Electric Vehicle (BEV) | 0 | 2% | Locked until April 2025, modest increases thereafter but remains lowest. |

| Plug-in Hybrid Electric Vehicle (PHEV) | 1-50 (with significant electric range) | From 5% (depending on electric range) | Reduced rates compared to ICE, increasing over time. |

| Petrol/Diesel Car | 51+ | Over 20% (up to 37%) | Highest rates, increasing with higher emissions. |

As you can see, the difference is stark. A 2% BIK rate on an EV compared to 20%+ on a petrol or diesel car translates to substantial monthly savings. This makes the transition to an electric vehicle not just environmentally sound but also a financially savvy move, aligning with the government's 2035 target to phase out petrol and diesel car sales.

Is a Salary Sacrifice Car Scheme Worth It for You?

Beyond the tax advantages, salary sacrifice schemes offer a host of benefits that can make them highly appealing. One of the most significant is the ability to obtain a brand-new car, which you might not otherwise be able to afford. New cars generally boast superior reliability, enhanced safety features, and are often cheaper to run in terms of maintenance compared to older models. Furthermore, you benefit from a manufacturer warranty and direct support from the vehicle provider should any issues arise.

Most salary sacrifice agreements are designed as all-inclusive packages. This typically means that the single monthly fee covers Vehicle Excise Duty (VED), comprehensive insurance, roadside assistance, and even routine maintenance and servicing. This simplifies car ownership immensely, as your only direct day-to-day running cost out of your own pocket would be fuel – or the cost of charging if you opt for an EV. Unlike personal leasing contracts or PCP finance, there's usually no initial payment or large deposit required, allowing you to get into a new car straight away without a significant upfront outlay.

If you select a car that aligns with the scheme's financial benefits, especially an EV, the overall costs can be considerably lower than if you were to fund, insure, and maintain a car yourself. This convenience and potential for savings make salary sacrifice a compelling option for many.

Potential Pitfalls and Considerations

While the benefits are clear, it's crucial to acknowledge the downsides of salary sacrifice schemes to make an informed decision. One of the primary drawbacks stems directly from the BIK tax. If you choose a car with higher CO2 emissions, such as a large SUV, a powerful sports car, or a hot hatch, the BIK penalty can negate much of the salary sacrifice saving, potentially making it more expensive than funding the car yourself.

Another common limitation is choice. You're restricted to the vehicles available through your employer's scheme, which might not include the exact make, model, or specification you truly desire or need. While many schemes offer a wide range, it's not the same as having the entire market at your disposal.

Once you enter into a salary sacrifice agreement, you are typically locked in for the duration of the contract, which is usually between two and four years. Breaking this contract can incur significant early termination fees, unless you leave your job, in which case you will generally have to return the car. Because the cost is deducted from your salary, there's less financial flexibility if your circumstances change and you find yourself struggling to make payments.

It's also important to consider the impact on your net salary. While the scheme aims to save you money on tax, your take-home pay will be lower. This reduced net income could potentially affect your ability to obtain mortgages, personal loans, or other forms of credit, as lenders assess your affordability based on your declared income. Finally, as the car is leased, you will have to return it at the end of the contract term. You'll then need to either enter into a new salary sacrifice agreement or find an alternative method to acquire your next vehicle.

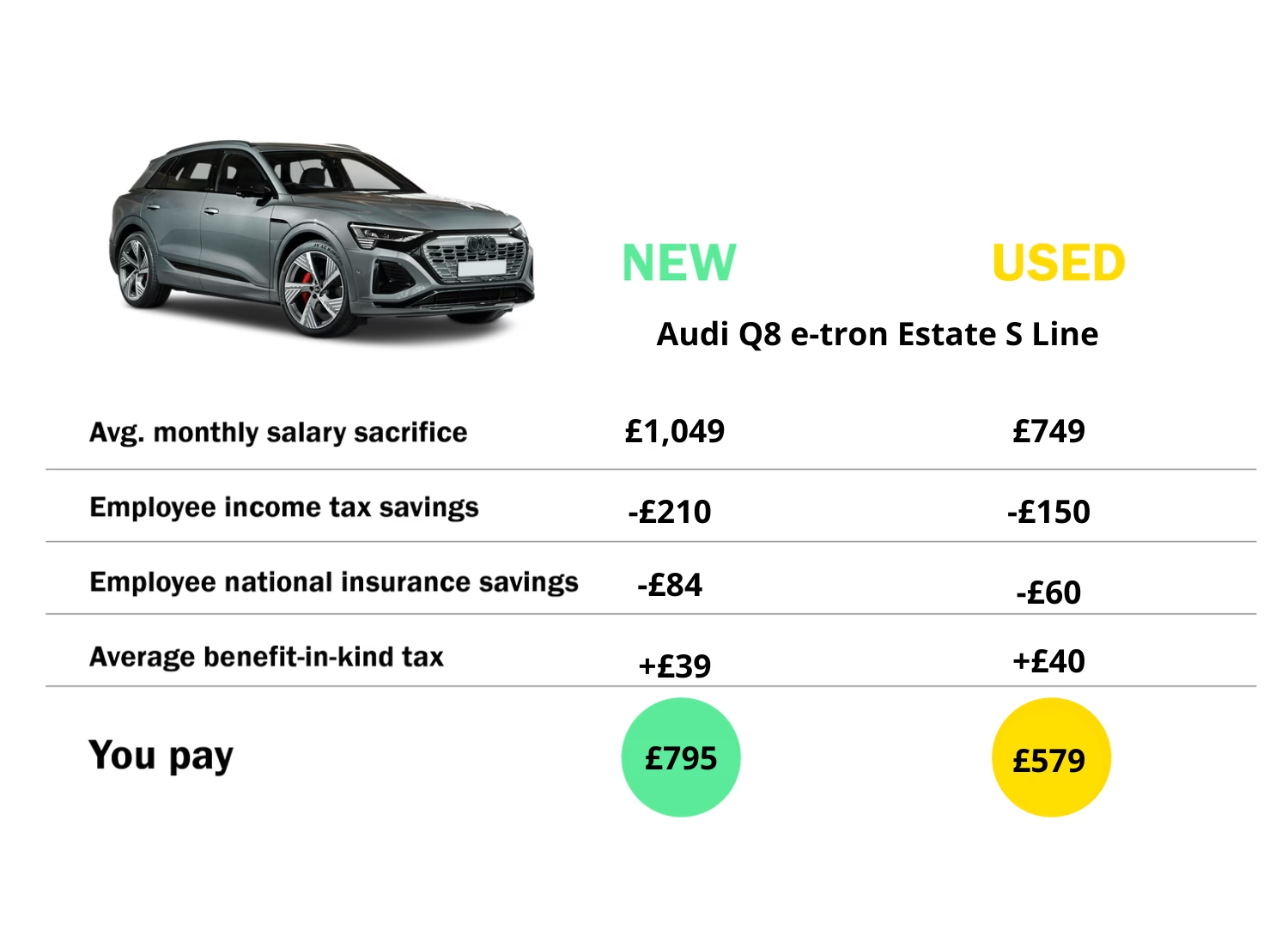

Calculating Your Potential Savings

Determining the exact savings from a salary sacrifice car scheme requires careful calculation tailored to your specific circumstances and the scheme offered by your employer. Once you have access to the list of available vehicles, their lease rates, and the included benefits, you can begin to work out the true monthly cost and potential savings. Remember to factor in the monthly BIK tax for the entire duration of the contract, as these rates can periodically increase (though for EVs, they remain low).

To get a clear picture, you also need to calculate what you would spend on a comparable car if you were funding it yourself. This includes:

- Monthly finance payments (PCP, HP, personal lease)

- Insurance premiums

- Vehicle Excise Duty (VED/road tax)

- Servicing and maintenance costs

- MOT tests (for cars over three years old)

- Breakdown cover

- Any initial deposit or upfront payment

By comparing the all-inclusive salary sacrifice cost (including BIK) with your estimated self-funded costs, you can ascertain the true financial benefit. Always ensure your employer's scheme provider gives you a transparent and accurate overview of all anticipated costs before you commit.

Impact on Pensions and National Insurance

One common concern with salary sacrifice is its effect on pensions and National Insurance contributions. When you sacrifice a portion of your salary, your gross pay is reduced, which in turn means both you and your employer pay less National Insurance Contributions (NICs). While this is part of the saving mechanism, it could potentially have a minor impact on certain State Benefits that are linked to your NI contribution history. It’s always advisable to check with the Department for Work and Pensions if you have specific concerns about this.

Regarding pensions, the situation is generally more favourable. While your take-home pay is lower, most well-structured salary sacrifice schemes for cars ensure that your pensionable earnings are based on your *pre-sacrifice* salary. This means your pension contributions (both yours and your employer's) and, crucially, your future pension benefits are typically not adversely affected. Your employer should ensure that their payroll provider records the sacrificed salary as a 'notional permanent pensionable allowance' and that contributions are calculated on your original, higher salary. This protection is a key element that makes salary sacrifice attractive without compromising long-term financial security.

Frequently Asked Questions (FAQs)

Can I choose any car I want?

No, you are generally limited to the range of vehicles offered through your employer's chosen scheme provider. While the selection is often broad, it won't be as extensive as the entire car market.

What happens if I leave my job?

If you leave your employment, you will typically have to return the car. Most schemes have early exit clauses to cover this, but it's essential to understand any associated fees or procedures beforehand.

Does salary sacrifice affect my mortgage application?

Potentially, yes. Lenders assess your affordability based on your net income. A reduced gross salary means a lower net take-home pay, which could influence the amount you can borrow for a mortgage or other loans. It's wise to discuss this with a financial advisor or lender if you're planning a significant financial application.

Are all running costs included in the scheme?

Most comprehensive schemes include VED, insurance, maintenance, and breakdown cover. However, fuel/charging costs are almost always your responsibility. Always check the specifics of your employer's scheme carefully to understand what is and isn't included.

Will my BIK tax rate change during the contract?

BIK rates are set by the government and can change over time. While the rates for EVs are currently very low and set to increase only modestly in the coming years, it's possible your BIK liability could increase slightly during a multi-year contract, affecting your overall monthly cost.

Conclusion

A salary sacrifice car scheme can be an excellent way to acquire a new vehicle, particularly an electric vehicle, offering significant tax and National Insurance savings, bundled convenience, and often no upfront deposit. The attractive low BIK rates for EVs make them a standout choice, aligning financial prudence with environmental responsibility. However, it's not a one-size-fits-all solution. Understanding the BIK tax implications, the potential impact on your net salary and future finances, and the contractual obligations are crucial. By carefully evaluating your personal circumstances, the specific scheme offered by your employer, and performing a thorough cost comparison, you can determine if a salary sacrifice car truly stacks up as the right choice for your next set of wheels.

If you want to read more articles similar to Salary Sacrifice Cars: Tax & Savings Explained, you can visit the Cars category.