19/05/2017

The intricate dance of global oil demand is entering a new phase, marked by a projected slowdown in growth and significant shifts in consumption patterns. A recent report from the International Energy Agency (IEA) paints a compelling picture of a market on the cusp of change, with cleaner energy technologies and evolving consumer behaviours accelerating the transition away from traditional fossil fuels. While the overall demand for oil is expected to continue its upward trajectory in the coming years, the pace of this growth is set to decelerate dramatically, signalling a potential peak in demand before the end of the decade.

- The IEA's Medium-Term Outlook: A Forecast of Slowing Growth

- Key Drivers of Change: EVs, Biofuels, and Efficiency

- Petrochemicals and Aviation: Pillars of Support

- Geopolitical Ripples and Market Recalibration

- China's Role in the Shifting Demand Landscape

- Investment Trends: Meeting Demand vs. Net Zero Ambitions

- Spare Capacity and Market Balances

- Supply Capacity: A Tale of Two Halves

- Refining Sector Dynamics: Tightness and Divergence

- Key Takeaways and Future Considerations

The IEA's Medium-Term Outlook: A Forecast of Slowing Growth

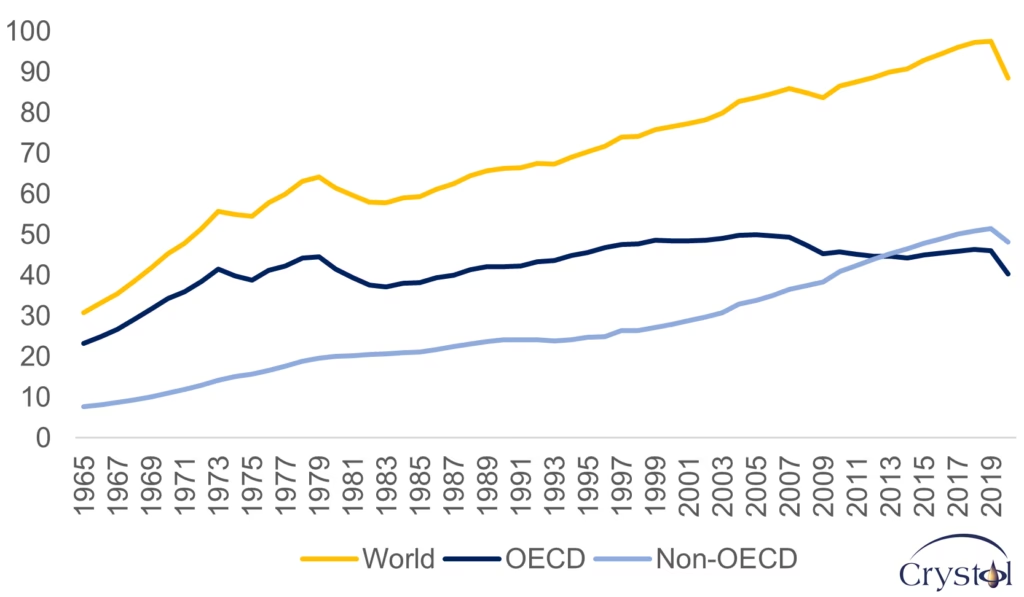

According to the IEA's 'Oil 2023' medium-term market report, global oil demand is predicted to rise by 6% between 2022 and 2028, reaching an estimated 105.7 million barrels per day (mb/d). This growth, while seemingly substantial, is underpinned by a stark deceleration in annual demand growth. From a robust 2.4 mb/d this year, the forecast anticipates this figure to dwindle to a mere 0.4 mb/d by 2028. This trend suggests that the world is inching closer to a point where oil consumption may plateau and eventually begin to decline.

Key Drivers of Change: EVs, Biofuels, and Efficiency

Several factors are contributing to this anticipated slowdown. Foremost among them is the burgeoning electric vehicle (EV) revolution. The rapid expansion of EV adoption, coupled with advancements in battery technology and government incentives, is directly impacting the demand for transport fuels. The report explicitly states that oil use for transport is projected to enter a period of decline after 2026. This decline is further bolstered by the increasing use of biofuels and a general improvement in vehicle fuel economy, both of which contribute to reducing overall oil consumption in the transportation sector.

“The shift to a clean energy economy is picking up pace, with a peak in global oil demand in sight before the end of this decade as electric vehicles, energy efficiency and other technologies advance,” stated IEA Executive Director Fatih Birol. He further emphasised the need for oil producers to adapt: “Oil producers need to pay careful attention to the gathering pace of change and calibrate their investment decisions to ensure an orderly transition.”

Petrochemicals and Aviation: Pillars of Support

Despite the projected decline in transport fuel demand, the overall growth in oil consumption is expected to be supported by other key sectors. The petrochemical industry, which uses oil as a feedstock for plastics and other materials, is forecast to experience robust demand growth. Similarly, the aviation sector, while facing its own sustainability challenges, is also anticipated to contribute to sustained oil consumption in the medium term. These sectors are crucial in offsetting the contraction observed in advanced economies, particularly as emerging and developing economies continue to expand their industrial and transportation networks.

Geopolitical Ripples and Market Recalibration

The global oil market has navigated a turbulent period in recent years. The COVID-19 pandemic and Russia's invasion of Ukraine have profoundly reshaped trade flows and highlighted the critical importance of energy security. The energy crisis triggered by the conflict in Ukraine has led to an unprecedented reshuffling of global oil trade. In the short term, production cuts by the OPEC+ alliance are expected to tighten global oil markets, potentially leading to higher prices. However, the report suggests that these strains are likely to ease in the following years as markets continue to recalibrate.

China's Role in the Shifting Demand Landscape

China, having lifted its stringent COVID-19 restrictions late last year, experienced a rebound in oil demand in the first half of 2023. However, the IEA forecasts a marked slowdown in China's demand growth from 2024 onwards. Despite this slowdown, the country's burgeoning petrochemical demand and overall consumption growth in emerging and developing economies are expected to play a pivotal role in sustaining global oil demand, even as advanced economies witness a contraction.

Investment Trends: Meeting Demand vs. Net Zero Ambitions

Global upstream investments in oil and gas exploration, extraction, and production are set to reach their highest levels since 2015, with an 11% year-on-year increase to USD 528 billion in 2023. While cost inflation will partially offset the impact of higher spending, the report suggests that this level of investment, if sustained, would be adequate to meet the forecast demand within the report's timeframe. However, this investment level significantly exceeds the amount required to align with a net-zero emissions pathway. This highlights a potential mismatch between current investment strategies and the urgent need for a transition to cleaner energy sources.

Spare Capacity and Market Balances

The report's projections are based on the assumption that major oil producers will continue with their plans to build up capacity, even as demand growth slows. This is expected to result in a spare capacity cushion of at least 3.8 mb/d, predominantly concentrated in the Middle East. Nonetheless, several factors could influence market balances in the medium term. These include uncertain global economic trends, the strategic decisions made by OPEC+, and the refining industry policies implemented in China.

Supply Capacity: A Tale of Two Halves

Oil-producing countries outside the OPEC+ alliance are expected to lead the increase in global supply capacity over the medium term. An anticipated rise of 5.1 mb/d by 2028 is largely attributed to production growth in the United States, Brazil, and Guyana. Within OPEC+, Saudi Arabia, the United Arab Emirates, and Iraq are at the forefront of capacity expansion plans. Conversely, African and Asian OPEC+ members are projected to face continuing production declines, and Russian output is expected to fall due to sanctions. Consequently, OPEC+ members are collectively projected to see a net capacity gain of only 0.8 mb/d over the forecast period.

Refining Sector Dynamics: Tightness and Divergence

The refining sector has experienced a reduction in global capacity overhang due to a series of closures, conversions to biofuel plants, and project delays since the pandemic. This, coupled with a sharp decrease in Chinese oil product exports and the disruption of Russian trade flows, contributed to record profits for the industry in the past year. While net refinery capacity additions by 2028 are expected to outpace the growth in demand for refined products, diverging trends among different product types mean that a recurrence of the tightness observed in middle distillates in 2022 cannot be entirely ruled out.

Key Takeaways and Future Considerations

The IEA's report underscores a significant shift in the global oil market. The key takeaways are:

| Factor | Impact on Oil Demand | Timeframe |

|---|---|---|

| Electric Vehicles | Declining demand for transport fuels | After 2026 |

| Petrochemicals | Strong demand support | Medium-term |

| Biofuels & Efficiency | Reduced consumption in transport | Ongoing |

| Global Economic Trends | Potential market uncertainty | Medium-term |

| OPEC+ Decisions | Influence on supply and prices | Ongoing |

Frequently Asked Questions:

Q1: When is global oil demand expected to peak?

According to the IEA report, global oil demand is expected to peak before the end of this decade, driven by the increasing adoption of electric vehicles, energy efficiency improvements, and other clean energy technologies.

Q2: Which sectors will continue to drive oil demand growth?

The petrochemical sector and the aviation industry are expected to provide the strongest support for oil demand growth in the coming years.

Q3: Will oil prices increase due to production cuts?

Production cuts by the OPEC+ alliance could lead to tighter global oil markets and potentially higher prices in the coming months, although the report suggests these strains may ease in the following years.

Q4: How will electric vehicles impact oil demand?

Electric vehicles, alongside biofuels and improved fuel economy, are projected to cause a decline in the demand for oil used in transport fuels after 2026.

Q5: Is current oil investment aligned with climate goals?

While current investment levels are sufficient to meet forecast demand, they exceed the amount needed to achieve net-zero emissions, indicating a need for a recalibration of investment strategies towards cleaner energy sources.

The evolving landscape of global oil demand presents both challenges and opportunities. As cleaner energy technologies mature and gain wider adoption, the reliance on fossil fuels is set to diminish. For oil producers and the broader energy industry, understanding these shifts and adapting investment strategies will be crucial for navigating the transition to a more sustainable energy future. The coming years will be a critical period for observing how these trends unfold and shape the global energy mix.

If you want to read more articles similar to Global Oil Demand: A Shifting Landscape, you can visit the Automotive category.