18/08/2024

Experiencing a car accident can be incredibly stressful, and the aftermath often brings a bewildering array of questions. One of the most perplexing situations arises when your vehicle is deemed a 'total loss' or 'write-off' by your insurance company. This isn't just a term; it's a pivotal moment that dictates the future of your vehicle and your claim. Understanding what happens when your car is damaged to this extent, from both the consumer's and the insurer's perspective, is crucial for navigating the process with greater ease and less anxiety.

The immediate steps after an accident are often instinctive: ensure safety, exchange details, and crucially, report the incident to your insurance provider. This initial contact sets in motion a detailed assessment process. Your insurer will typically assign a claims handler who may then dispatch a company or independent adjuster (also known as an appraiser or vehicle damage assessor) to inspect your damaged car. Depending on the severity, you might initially be asked to provide one or two repair estimates yourself. However, for more significant damage, a professional assessment is almost always required to determine the vehicle's fate.

What Defines a 'Total Loss' or 'Write-Off'?

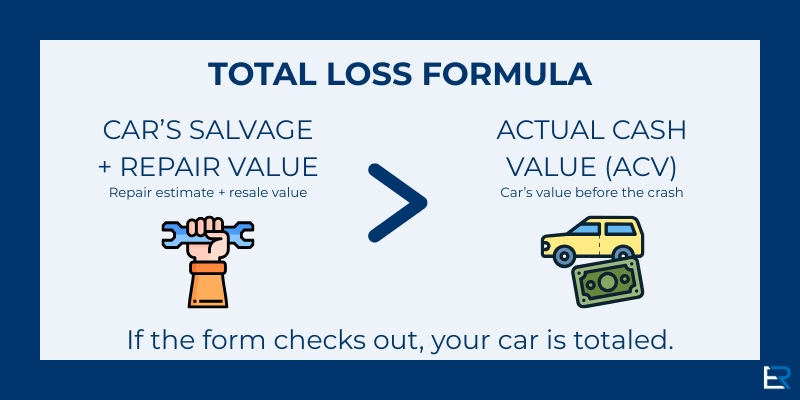

In the UK, a vehicle is declared a 'total loss' or 'write-off' when the cost of repairing the damage exceeds a certain percentage of its pre-accident market value. While the exact percentage can vary slightly between insurers, it's commonly around 60-70% of the vehicle's market value, though it can sometimes be as high as 100%. The key principle is that it's uneconomical for the insurer to repair the vehicle. Essentially, if fixing the car costs more than replacing it, it's written off.

The decision to write off a vehicle isn't arbitrary; it's based on a careful evaluation of several factors:

- Vehicle Age: Older cars generally have lower market values, making them more susceptible to being written off even with moderate damage.

- Mileage: High mileage typically reduces a vehicle's market value.

- Pre-Accident Condition: The general condition of your car before the incident (e.g., bodywork, interior, service history) directly impacts its market value.

- Severity of Damage: The extent and nature of the damage are paramount. Structural damage, damage to safety features (like airbags), or extensive engine/transmission damage often lead to a write-off.

It's important to be transparent with your adjuster about any significant improvements or upgrades you've made to your vehicle, such as a new transmission, upgraded infotainment system, leather seating, or a sunroof. While these might seem like standard features, they can significantly influence the vehicle's actual cash value (ACV) and, consequently, the threshold for a write-off. Be sure to highlight any specific trim packages or engine sizes, as these also play a role in accurate valuation.

The Assessment and Valuation Process

Once the inspection is complete, the adjuster will compile a comprehensive report, including photos of the damage and an estimate of the repair costs. Crucially, they will also determine the actual cash value (ACV) of your vehicle just before the accident. This valuation is typically based on industry guides such as Glass's Guide or CAP HPI, which provide data on similar vehicles sold in your region. This information, comparing repair costs to the ACV, forms the basis of the 'repairable vs. write-off' decision.

If your vehicle is deemed a total loss, the adjuster will contact you to discuss the valuation and the next steps. Do not hesitate to ask for a detailed breakdown of how the ACV was calculated and to review the repair estimate. It's your right to understand the figures involved.

Understanding UK Write-Off Categories

When a vehicle is written off in the UK, it's assigned a specific category based on the extent and type of damage. These categories dictate whether the vehicle can ever return to the road. Since October 2017, the categorisation system changed from Category C and D to Category S and N. The current categories are:

| Category | Description | Return to Road? |

|---|---|---|

| Category A (Scrap) | Vehicle is so severely damaged it cannot be repaired and must be crushed. No parts can be salvaged. | No |

| Category B (Break) | Vehicle is severely damaged and cannot be repaired. Parts can be salvaged for use in other vehicles, but the body shell must be crushed. | No (Vehicle itself) |

| Category S (Structural Damage) | Vehicle has sustained damage to its structural frame or chassis, making it unsafe to drive. It can be repaired professionally and returned to the road, but must pass a new MOT test before being used. | Yes (After repair & MOT) |

| Category N (Non-Structural Damage) | Vehicle has sustained non-structural damage (e.g., to the body panel, electrics, or interior). It can be repaired and returned to the road without a new MOT, though an MOT is still required if its existing one has expired. | Yes (After repair) |

Prior to October 2017, Category C was for repairable structural damage (similar to Cat S), and Category D was for repairable non-structural damage (similar to Cat N). If you're dealing with an older write-off, you might still encounter these terms.

Why Do Insurers Take Possession of 'Write-Offs'?

This is a common point of confusion and frustration for many claimants. If your vehicle is declared a total loss, the insurer will typically pay you 100% of its market value (minus any applicable excess) and, in return, take possession of the vehicle. This raises questions like: "Why don't they take a 99% interest if they repair up to that point?" or "Why aren't they shareholders in repaired vehicles?"

The answer lies in the fundamental principle of insurance: indemnity. Insurance aims to put you back in the financial position you were in just before the loss occurred, no better, no worse. It's not designed for you to profit from a claim, nor for the insurer to gain an ongoing stake in your property. When your car is written off, the insurer effectively buys it from you for its pre-accident market value. By paying you the full value, they assume ownership of the damaged asset. This allows them to recover some of their costs by selling the salvage (the damaged vehicle) to salvage yards or dismantlers, who will either break it for parts (Cat B), repair it (Cat S or N), or crush it (Cat A).

If an insurer were to retain a share in every repaired vehicle, it would create an incredibly complex and impractical system, transforming them into a part-owner of millions of vehicles, constantly tracking their resale value. The current system of paying out the market value and taking possession of the salvage is the most straightforward and traditional way to uphold the principle of indemnity in a total loss scenario.

Your Options as a 'Total Loss' Victim

While the insurer typically takes possession of a written-off vehicle, there are sometimes options, particularly for Category S or N write-offs. The question arises: "Would it not be better for a 'total loss' victim to elect to accept only 99% of the market value, and to retain the vehicle for repairing (Category S or N), or for spares and scrap (Categories A & B) to mitigate inevitable losses experienced by the 'total loss' claimant?"

In reality, accepting 99% of the market value and keeping the car is not a standard option for Category A or B write-offs, as these vehicles are deemed unroadworthy and must be destroyed or dismantled. However, for Category S and N vehicles, it is often possible to "buy back" the salvage from your insurer. If you choose this route:

- The insurer will deduct the salvage value (what they would have received for selling the car to a salvage yard) from your payout.

- You will receive a lower payout, but you retain ownership of the damaged vehicle.

- If it's a Category S vehicle, you will need to have it professionally repaired to a roadworthy standard and then pass a new MOT test before it can be legally driven on public roads. This can be costly and complex.

- For Category N, you will also need to arrange repairs, but a new MOT is not specifically required due to the write-off status (though your existing MOT must still be valid).

- Be aware that a vehicle declared Category S or N will have this recorded against its history, which can significantly reduce its future resale value. Many buyers are wary of written-off vehicles.

While retaining the vehicle might seem appealing, especially if you have the skills or resources to repair it cheaply, it's crucial to weigh the financial implications carefully. The reduced payout, potential repair costs, and diminished resale value can sometimes outweigh the perceived benefits. The "inevitable losses" experienced by a total loss claimant often stem from the fact that the ACV payout may not be enough to replace the vehicle with an identical one, especially if you had recently invested in it or if its true value to you was higher than the market average. This is a challenge inherent in the indemnity principle, as insurance doesn't cover sentimental value or the inconvenience of finding a replacement.

Payouts, Excess, and Lienholders

When your vehicle is declared a total loss, the insurer will pay out the agreed market value. However, this payment is always subject to your policy's excess (the fixed amount you agreed to pay towards any claim). This excess will be deducted from your total payout. For example, if your car is valued at £5,000 and your excess is £250, you would receive £4,750.

Furthermore, if you have outstanding finance on your vehicle (a loan or lease agreement), the lienholder (the finance company) has the first right to the payment. The insurer will pay the finance company directly, and if there's any remaining money, it will be paid to you. If the payout is less than your outstanding finance, you will be responsible for covering the shortfall to the finance company – this is where Gap Insurance can be invaluable, as it covers the difference between the insurer's payout and the outstanding finance.

Frequently Asked Questions About Total Loss Claims

Q: What if I disagree with the insurer's valuation of my vehicle?

A: You have the right to dispute the valuation. Gather evidence to support your claim for a higher value, such as recent sales of identical or similar vehicles in your area, receipts for recent maintenance, upgrades, or unique features. Present this information to your insurer and be prepared to negotiate. If an agreement cannot be reached, you can escalate the complaint through the insurer's internal complaints procedure, and if still unresolved, refer it to the Financial Ombudsman Service (FOS).

Q: Can I keep a written-off car?

A: For Category A and B write-offs, no – these must be destroyed or dismantled. For Category S and N, yes, you can often 'buy back' the salvage from your insurer. They will deduct the salvage value from your payout. You then take responsibility for repairs and, for Category S, an MOT retest.

Q: How long does a total loss claim take?

A: The timeline can vary significantly. Once the vehicle has been inspected and declared a write-off, the valuation and payout process usually takes a few days to a couple of weeks, assuming no disputes. However, the initial assessment and decision can take longer, especially if there are delays in inspecting the vehicle or gathering necessary information.

Q: Do I still have to pay my excess if my car is written off?

A: Yes, your policy's excess is a standard deduction from your payout, regardless of whether the car is repaired or written off. However, if the accident was not your fault and the other party's insurer accepts liability, you may be able to reclaim your excess from them.

Q: What is 'Gap Insurance' and do I need it?

A: Gap Insurance (Guaranteed Asset Protection) covers the 'gap' between your insurer's payout for a total loss and the amount you still owe on your car finance agreement, or the original purchase price. If you bought your car on finance, or it's a new car, it can be a valuable policy to prevent you from being in negative equity after a write-off.

Resolving a physical damage claim, particularly a total loss, can be a demanding experience. Remember to be thorough, ask plenty of questions, keep detailed records of all communications, and understand your rights. By doing so, you can navigate the process more effectively and ensure the best possible outcome for yourself.

If you want to read more articles similar to Navigating a Total Loss Car Claim in the UK, you can visit the Insurance category.