25/05/2026

Finding yourself involved in a car accident can be a truly jarring experience, even more so when the incident wasn't your fault. In the immediate aftermath, it's easy to feel overwhelmed and unsure of the correct steps to take. However, understanding your rights and the proper procedures is paramount to ensuring a smooth claims process, protecting your interests, and getting your vehicle back on the road without unnecessary financial burden. This detailed guide is designed to equip you with all the essential knowledge for handling a non-fault car accident in the UK, from the crucial moments at the scene to dealing with insurers, understanding 'write-offs', and recovering additional costs.

Your actions immediately following an accident can significantly impact the outcome of any potential insurance claim. Remaining calm and following a structured approach will not only help you manage the situation effectively but also ensure you gather all necessary evidence to support your position. Remember, while the shock might be intense, a clear head is your best asset.

- Immediate Steps After a Non-Fault Accident

- Understanding Your Insurance Policy: Comprehensive vs. Third Party

- Claiming for Uninsured Losses

- What if the Other Driver is Uninsured or Can't Be Identified?

- Vehicle Repairs and Insurance Write-Offs

- Non-Fault vs. At-Fault Claims: A Clear Distinction

- Frequently Asked Questions

- Q: Can I lose my no-claims bonus if the accident wasn't my fault?

- Q: What exactly are 'uninsured losses'?

- Q: Do I have to use my insurer's approved repairer?

- Q: What if the other driver refuses to give me their details?

- Q: What happens if my car is declared an insurance write-off?

- Q: How do I prove the accident wasn't my fault?

- Final Thoughts

Immediate Steps After a Non-Fault Accident

Even if you're certain the accident wasn't your fault, there are critical steps you must take at the scene. These actions are designed to protect your position and gather the necessary information for your insurance provider.

- Do Not Admit Fault: This is perhaps the most crucial piece of advice. Never admit liability at the scene of an accident, regardless of how clear-cut you believe the situation to be. Admitting fault could prejudice your claim and make it incredibly difficult for your insurer to recover costs from the other party. Stick to factual observations.

- Exchange Details: It is a legal requirement to exchange details with any other drivers involved. Obtain their full name, address, phone number, vehicle registration number, and insurance details (insurer name and policy number). If possible, also note the make, model, and colour of their vehicle.

- Gather Witness Information: Look for any independent witnesses who saw the accident occur. Their testimony can be invaluable in corroborating your account. Ask for their name, phone number, and email address. If they're willing, ask if they can provide a brief statement of what they observed.

- Take Photographs: Modern smartphones make this incredibly easy. Take multiple photographs of the accident scene from various angles. Capture the position of all vehicles involved, damage to all vehicles, road markings, traffic signs, weather conditions, and any relevant debris. The more photographic evidence you have, the stronger your claim will be.

- Report to Your Insurer: You should inform your insurance provider about the accident straight away, even if you do not initially intend to make a claim. Most policies have a clause requiring you to notify them of any incident involving your vehicle, regardless of fault. This ensures they are aware and can offer guidance.

- Contact the Police (If Necessary): If anyone is injured, or if the other driver fails to stop or refuses to provide details, you must contact the police. If you can't show your insurance certificate or cover note at the scene when required by police due to injury, you must present these documents at a police station within seven days.

Understanding Your Insurance Policy: Comprehensive vs. Third Party

The type of motor insurance policy you hold will dictate the initial path your non-fault claim takes. It's essential to understand the difference between comprehensive and third-party policies in this context.

Comprehensive Insurance

If you have a comprehensive policy, you typically claim from your own insurer. They will arrange for the repairs to your vehicle (minus any excess) and then seek to recover their costs from the at-fault driver's insurance company. This is usually the quickest way to get your vehicle repaired and back on the road.

One common concern with a non-fault claim on a comprehensive policy is the potential impact on your no-claims bonus. While your insurer will endeavour to recover all costs from the other party's insurer, if they are unsuccessful for any reason (e.g., the other driver is uninsured or untraceable), you may indeed lose some or all of your no-claims bonus. However, once costs are fully recovered, your no-claims bonus should be reinstated. It's always wise to check your policy's specifics regarding protected no-claims bonuses.

Third Party Insurance

With a third-party policy, your own insurer will not cover the cost of repairs to your vehicle if the accident wasn't your fault. Instead, you will need to make a claim directly against the other driver and their insurance company. Your insurer's role in this scenario is primarily to deal with any claims made against you by the other party for damage or injury they sustained.

To claim from the other driver, you should inform them in writing of your intention to do so, providing details of the accident. If they were driving a company vehicle, you should also inform the company. It's also crucial to inform your own insurer that you have initiated this process. The other driver is obligated to report the accident to their insurer. You can verify if the other driver has valid insurance by contacting the Motor Insurance Database (MID).

Policy Comparison for Non-Fault Claims

Here's a quick comparison of how comprehensive and third-party policies generally handle non-fault claims:

| Feature | Comprehensive Policy (Non-Fault Claim) | Third Party Policy (Non-Fault Claim) |

|---|---|---|

| Initial Repair Costs | Covered by your insurer (minus excess). | You pay for your own repairs, then claim back. |

| No-Claims Bonus Impact | May be affected if costs aren't recovered; usually reinstated. | Generally unaffected as you claim from third party. |

| Claim Process | Your insurer handles recovery from other party. | You claim directly from other driver/insurer. |

| Uninsured Losses | Can claim from other driver's insurer. | Can claim from other driver's insurer. |

| Speed of Repair | Generally faster, as your insurer initiates. | Can be slower, dependent on third party's insurer. |

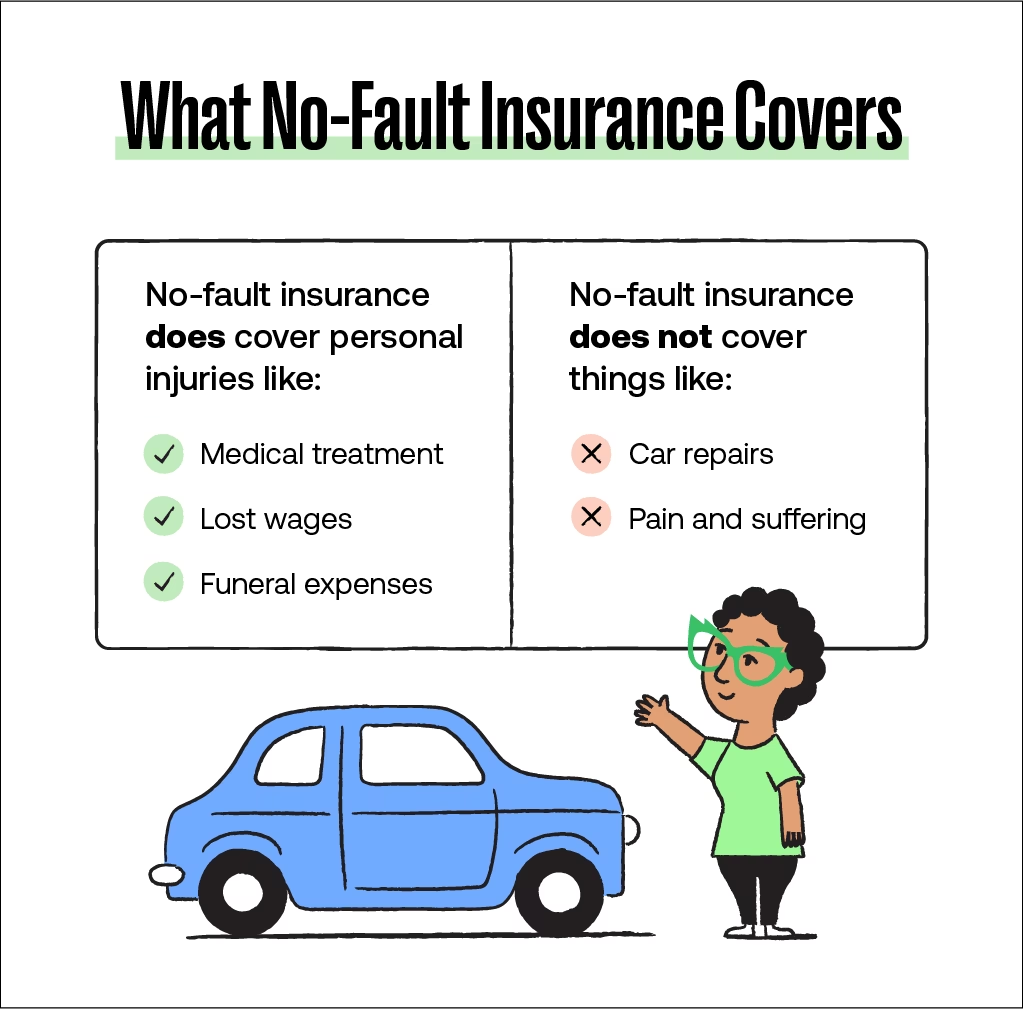

Claiming for Uninsured Losses

Even if your vehicle repairs are covered, there are often other costs incurred as a result of an accident that was not your fault. These are known as uninsured losses and can include a range of expenses not covered by your own insurance policy. You are entitled to claim these directly from the at-fault driver's insurer.

Common examples of uninsured losses include:

- Policy Excess: The amount you paid as an excess on your own comprehensive policy for repairs.

- Alternative Transport: The cost of hiring a replacement vehicle, using public transport, or taxi fares while your car is being repaired. It's important that any hired vehicle is similar in class to your own to justify the cost.

- Loss of Earnings: If you had to take time off work due to injuries or to deal with the aftermath of the accident.

- Personal Injuries: Compensation for any physical or psychological injuries you sustained.

- Damage to Personal Belongings: Items in your car that were damaged, such as a laptop, mobile phone, or child car seat.

- Travel Costs: Expenses incurred for medical appointments or visiting repair garages.

To claim for uninsured losses, you must keep all receipts and records of these expenses. You can either seek to recover these yourself by writing to the other driver's insurer or, often, your own insurer or a claims management company can assist you with this aspect of the claim. Some individuals opt to use a 'credit hire' company, which provides a replacement vehicle on credit, with the understanding that the cost will be recovered from the at-fault party's insurer.

What if the Other Driver is Uninsured or Can't Be Identified?

This is a particularly frustrating scenario, but there are still avenues for recourse, especially if the accident wasn't your fault.

- If You Have Comprehensive Cover: Your own comprehensive policy should cover the damage to your vehicle, even if the other driver is uninsured or flees the scene. You will still have to pay your excess, but your insurer will handle the repairs.

- The Motor Insurers Bureau (MIB): This organisation plays a crucial role in compensating victims of uninsured and untraced drivers in the UK. If the driver is uninsured, or if they cannot be identified (e.g., a hit-and-run), the Motor Insurers Bureau (MIB) may be able to settle your claim for personal injuries and property damage. This also includes cases where the driver has insurance but has breached their policy conditions (e.g., driving without a valid MOT or licence). However, be aware that you generally won't be able to claim from the MIB if you were an injured passenger of an uninsured driver and you knew, or reasonably should have known, that they weren't insured.

Vehicle Repairs and Insurance Write-Offs

Once liability is established and your claim is progressing, the next step is typically getting your vehicle repaired or, in some cases, declared a 'write-off'.

Repairing Your Vehicle

Your insurer will likely want to send an assessor to inspect your vehicle before any repairs begin. They may recommend or require you to use one of their approved repairers, or they might ask you to obtain several estimates from garages of your choice for their approval. While using an approved repairer can be convenient, you usually have the right to choose your own repairer, though you might need your insurer's approval for the chosen garage and their quote.

In some instances, if repairs significantly improve the condition of your vehicle beyond its pre-accident state (e.g., replacing old, worn tyres with brand new ones), your insurer might apply a 'betterment' clause, meaning you may have to contribute a small portion of the repair cost. This is less common for standard repairs but can occur.

When Your Car is a Write-Off

An insurance write-off occurs when your insurer determines that the cost of repairing your vehicle is uneconomical relative to its market value. This doesn't necessarily mean the car is irreparable, just that it's not cost-effective for the insurer to fix it. They will then offer you the car's market value at the time of the accident.

- Negotiating the Market Value: If you believe the offer is too low, you have the right to negotiate. Gather evidence of your car's true value, such as advertisements for similar cars for sale in your local area, recent sales data, or an independent valuation from a qualified engineer (though you'd typically pay for this yourself).

- Keeping a Write-Off: Normally, once a car is written off and you accept the market value, the insurer takes possession of the damaged vehicle. However, you can negotiate to keep the car. If you do, the insurer will deduct a 'salvage value' from your payout, reflecting what they would have received by selling the damaged vehicle for parts or scrap. They will only allow you to keep the car if it's repairable to a roadworthy condition and passes a new MOT after repairs.

- Consent for Scrapping: Your insurer should obtain your consent before sending your written-off car to a scrapyard for sale or breaking. If they scrap the car without your consent and then decide not to settle your claim, you are entitled to claim the salvage value of the car.

Minor Damage to Older Cars

For older cars with minor damage, you might consider not claiming on your insurance, especially if the repair cost is low. This is to avoid the risk of your car being declared a write-off, as insurers sometimes write off cars if repair costs are as little as 60% of the vehicle's value. If you repair it yourself, you avoid the write-off classification and potential hassle.

If you do claim and it's declared a write-off, you can still negotiate. You might be able to convince your insurer to value your car higher or find a garage that charges less for repairs than their approved network. Any alternative repairer must be approved by your insurer before work commences.

Non-Fault vs. At-Fault Claims: A Clear Distinction

It's important to differentiate between these two types of claims, as their impact on your insurance history and future premiums can differ significantly.

- Non-Fault Claim: This occurs when the liability for an accident clearly lies with another party, such as another motorist driving into the back of your vehicle. Your insurance provider will seek to recover all costs (repairs, hire car, etc.) from the person responsible or their insurer. Once these costs are fully recouped, the claim is recorded as a non-fault claim on your insurance history. While it's on your record, it typically has a much smaller impact on future premiums than an at-fault claim, and your no-claims bonus should remain intact or be reinstated.

- At-Fault Claim: This happens when you are deemed responsible for an accident, or when your insurance provider is unable to recover all repair costs from a third party (e.g., if the other driver is uninsured and the MIB doesn't cover all your losses). An at-fault claim will almost certainly lead to a loss of your no-claims bonus and can significantly increase your future insurance premiums.

Frequently Asked Questions

Q: Can I lose my no-claims bonus if the accident wasn't my fault?

A: If you have comprehensive insurance and make a claim through your own policy, your insurer will initially pay for the repairs. If they are successful in recovering all costs from the at-fault driver's insurer, your no-claims bonus should remain unaffected or be reinstated. However, if they cannot recover the costs (e.g., the other driver is uninsured or untraceable), you may indeed lose some or all of your no-claims bonus, unless you have protected it. Always check your policy wording.

Q: What exactly are 'uninsured losses'?

A: Uninsured losses are any costs you incur as a direct result of the accident that are not covered by your own insurance policy. This typically includes your policy excess, the cost of a hire car or alternative transport, loss of earnings due to injury or time off work, and compensation for personal injuries. You are entitled to claim these directly from the at-fault driver's insurance company.

Q: Do I have to use my insurer's approved repairer?

A: While your insurer might recommend or prefer you use an approved repairer, you generally have the right to choose your own garage. However, you will need to get a quote from your chosen repairer and get it approved by your insurer before any work begins. Insurers often have agreements with their approved network that can streamline the process, but your choice is usually respected.

Q: What if the other driver refuses to give me their details?

A: If the other driver refuses to provide their details or leaves the scene, it constitutes a hit-and-run, which is a criminal offence. You should immediately call the police to report the incident. Your insurer may be able to trace the driver through their vehicle registration number via the Motor Insurance Database. If they remain untraced or uninsured, the Motor Insurers Bureau (MIB) may be able to help with your claim, especially for personal injury.

Q: What happens if my car is declared an insurance write-off?

A: If your car is declared a write-off, your insurer believes it's uneconomical to repair. They will offer you the vehicle's market value at the time of the accident. You can negotiate this figure if you believe it's too low by providing evidence of your car's worth. You can also negotiate to keep the written-off vehicle, in which case a 'salvage value' will be deducted from your payout, and you'll be responsible for repairing it to a roadworthy standard.

Q: How do I prove the accident wasn't my fault?

A: The key to proving it wasn't your fault lies in gathering comprehensive evidence. This includes detailed photographs of the accident scene and vehicle damage, contact details and statements from independent witnesses, dashcam footage if available, and a clear, factual account of what happened. The more objective evidence you have, the stronger your case will be to your insurer and the third party's insurer.

Final Thoughts

Being involved in a car accident, even a non-fault one, is stressful. However, by understanding the steps to take, knowing your rights, and being prepared with the correct information, you can navigate the claims process with far greater ease and confidence. Always remember to prioritise safety, gather thorough evidence, and communicate promptly with your insurance provider. Your proactive approach will ensure that you achieve the best possible outcome and get back to your regular driving routine as swiftly as possible.

If you want to read more articles similar to Car Accident Not Your Fault? Know Your Rights!, you can visit the Insurance category.