28/07/2001

Dealing with an insurance payout that doesn’t quite stretch to cover your repair costs can be incredibly frustrating. Whether it's for damage to your home or your car, many policyholders naturally assume their claim cheque will perfectly align with the actual expenses, only to discover a disheartening gap between what they receive and what they owe. This common predicament can leave you feeling bewildered and out of pocket, wondering why your carefully chosen insurance policy isn't delivering the full protection you expected. Understanding the underlying reasons why this discrepancy occurs and, more importantly, knowing the proactive steps you can take is absolutely essential to ensure you aren't left paying more than necessary from your own pocket.

Common Reasons for a Lower Payment

Insurance companies meticulously determine claim payouts based on a complex interplay of policy terms, specific coverage limits, and their own expert assessment of the repair costs. One of the most frequent and often overlooked reasons for receiving a lower cheque than anticipated is the deductible. Every single insurance policy, without exception, includes a deductible. This is the predetermined amount you are personally responsible for paying towards a claim before your insurance provider steps in to cover the remainder. For instance, if your policy has a £1,000 deductible and the total repair cost for a damaged item or property is £5,000, your insurer will only issue a payment for £4,000. Many policyholders, in the heat of the moment or when estimating their expected payout, simply overlook this fundamental aspect of their policy.

Depreciation also plays a significant and often underestimated role, particularly in home insurance claims. Insurers frequently calculate payouts based on the Actual Cash Value (ACV) of the damaged property rather than its Replacement Cost Value (RCV). ACV inherently accounts for wear and tear, age, and obsolescence, meaning older materials or items are valued at significantly less than their original purchase price or the cost to replace them new. If your policy explicitly states that it only covers ACV, you may well receive a considerably lower amount than you expected, thus requiring you to cover the difference out of your own funds. This distinction between ACV and RCV is critical and often a source of confusion for policyholders.

Furthermore, policy exclusions and limitations can significantly reduce the final payout. It's not uncommon for some policies to explicitly exclude certain types of damage, such as gradual wear and tear, pre-existing conditions, mould growth, or specific weather-related events like floods in areas not designated for flood insurance. Even when damage is covered, insurers may impose specific sub-limits on particular types of repairs. For example, a home insurance policy might cap roof replacement coverage at £10,000, even if the actual, current cost to replace your roof is £15,000. Thoroughly understanding these limitations before you ever need to file a claim can help set far more realistic expectations regarding your potential payout.

Finally, the adjuster's assessment directly impacts the final payment you receive. Insurance adjusters are professionals trained to evaluate damage based on their inspections, which may, at times, differ considerably from the estimates provided by independent contractors. If the adjuster determines that certain repairs are unnecessary, or that pre-existing damage contributed to the current issue, they may reduce the payout accordingly. Insurers also frequently utilise proprietary third-party estimating software that applies standardised pricing models. While efficient, these models may not always accurately reflect the nuances of actual local repair costs, including variations in labour rates, material availability, and regional pricing differences.

Re-examining Repair Estimates

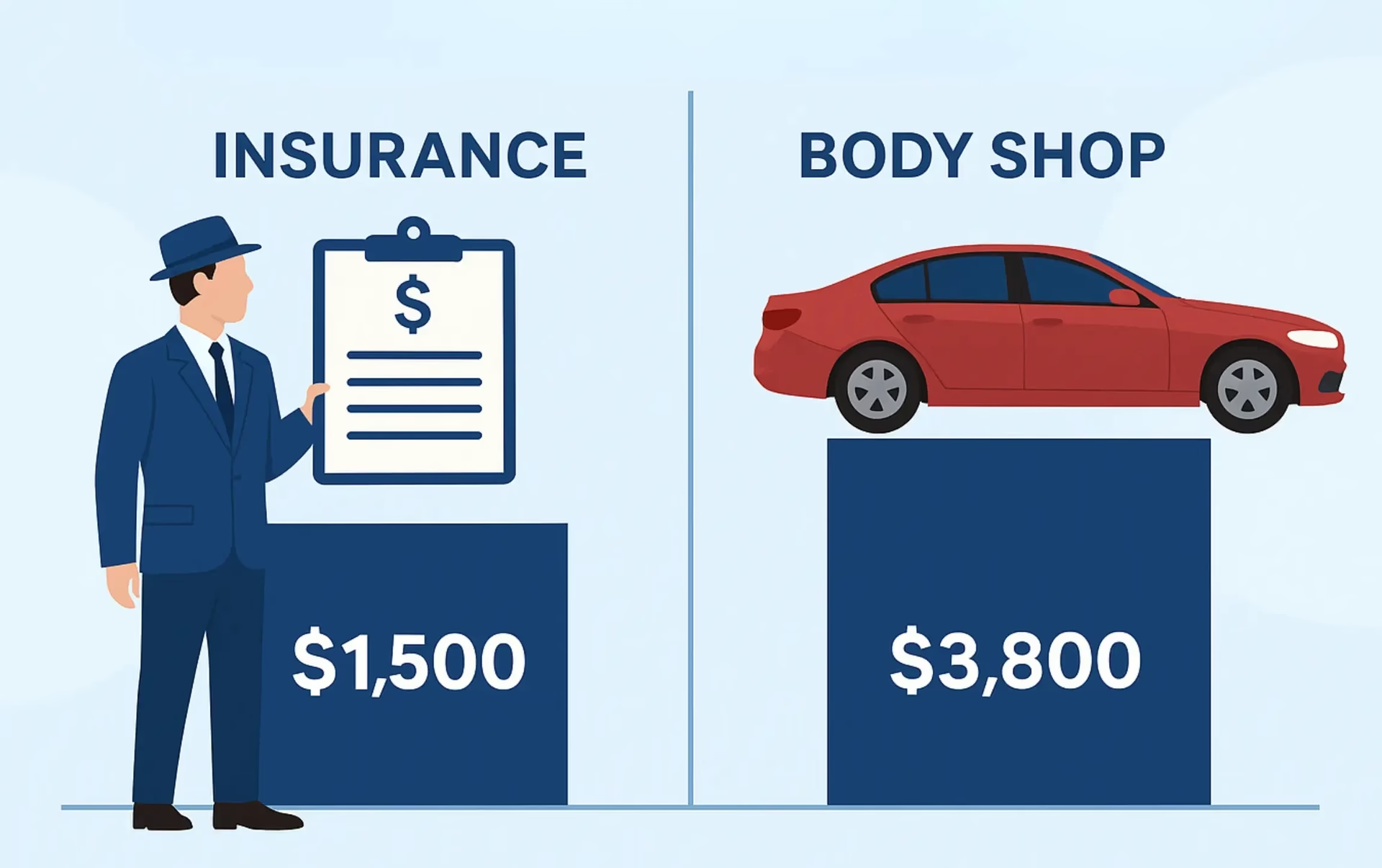

When your insurance payout falls short of your expectations, the very first crucial step is to meticulously review the estimate that the insurer used to calculate your payout. As previously mentioned, insurers often rely on adjusters who assess damage based on standardised pricing databases. While these databases aim for consistency and use regional averages, they don’t always account for the dynamic fluctuations in local labour costs, specific material shortages, or the specialised nature of certain repairs. If your chosen contractor’s estimate significantly exceeds the insurance payout, a detailed, line-by-line comparison of both assessments can often reveal glaring discrepancies that explain the shortfall.

It's worth noting that insurance-approved estimators often operate under strict cost-containment guidelines, which can inherently lead to lower payouts. They might suggest repairs instead of full replacements, even in scenarios where a complete replacement is demonstrably the more practical, durable, or ultimately cost-effective long-term solution. Adjusters may also inadvertently overlook hidden damage that only becomes apparent once the initial visible repairs begin. For instance, water damage may be far more extensive behind a wall than initially perceived. If the insurer’s report appears to lack crucial details – such as the need for structural reinforcements, specific materials, or code upgrades required by stringent local building ordinances – this could be a significant contributor to the financial shortfall. Requesting a comprehensive copy of the insurer’s estimate and meticulously reviewing it line by line with your contractor can help pinpoint these missing elements and build a stronger case for additional funds.

Another vital factor to consider is whether the insurer’s estimate included all necessary permits and compliance costs. Many local government bodies across the UK require specific permits for significant work such as roofing, extensive electrical rewiring, or major plumbing overhauls. The fees associated with these permits can add up considerably. Some insurance estimates may erroneously exclude these costs, assuming the homeowner will handle them separately. If your contractor’s bid explicitly includes permit fees and compliance costs, but the insurance estimate does not, this discrepancy can contribute significantly to the overall shortfall. Understanding your policy’s “ordinance or law” provisions can clarify whether additional funds should indeed be available for code-required upgrades, ensuring your repairs meet current safety and building standards.

Contractor Discrepancies

Differences between contractor estimates and insurance payouts frequently stem from fundamental variations in how damage is assessed and subsequently priced. Reputable contractors base their estimates on current, actual market rates for both materials and skilled labour, which are subject to supply and demand, inflation, and regional variations. In contrast, insurers often rely on standardised pricing models that, while efficient for processing large volumes of claims, may not fully reflect the dynamic and often higher current costs in a specific locality. This inherent difference can create a noticeable gap between what a qualified contractor genuinely charges and what the insurance company is initially prepared to pay. Furthermore, contractors, during their thorough assessment, may identify and include necessary repairs for underlying issues that insurers, with their more superficial initial assessment, may not have approved or even noticed.

A skilled contractor, upon deeper inspection, may uncover critical underlying issues such as extensive water damage beneath flooring, significant structural weakening behind walls, or hidden electrical faults that were not immediately visible or included in the insurer’s initial assessment. Insurance adjusters, particularly in cases where damage is not immediately apparent, often conduct only surface-level inspections. If the insurer’s estimate does not account for these additional, often crucial, repairs, the policyholder may face unexpected and substantial costs once the actual work commences. This scenario is particularly common in trades like roofing and plumbing, where hidden damage can dramatically increase the total repair bill beyond initial estimates.

Labour costs are also a frequent point of contention. Contractors employ skilled tradespeople whose rates reflect their expertise, the demand for their services, and the cost of living in the area. In contrast, insurers may base their labour cost calculations on outdated or lower-cost estimates derived from their standardised databases. In regions experiencing labour shortages, or following severe weather events that lead to a surge in demand for repairs, contractor prices can surge well beyond what an insurance company initially approves. If a homeowner opts to hire a contractor who charges above the insurer’s estimated rate, they will likely need to negotiate to bridge the difference or risk paying the excess amount entirely out of their own pocket. It's always advisable to get multiple quotes from reputable contractors to understand the true market rate for your repairs.

Submitting a Supplement Claim

When an insurance payout clearly falls short, policyholders are not without options; they can, and often should, file a supplement claim. This is a formal request for additional funds based on new information, newly discovered damage, or overlooked costs that genuinely justify a higher payment. Insurers typically allow supplement claims precisely for situations where additional damage is uncovered during the repair process, or if the original estimate demonstrably failed to account for necessary and legitimate costs. Many insurance policies include specific provisions for supplement claims to address these unforeseen or underestimated expenses, acknowledging that initial assessments may not always be exhaustive.

For a supplement claim to have the best chance of success, it must be well-documented and comprehensive. This should ideally include a revised, detailed contractor estimate that clearly outlines the new or additional work, high-quality photographs of the newly uncovered damage, and a thorough written explanation detailing why the additional work is necessary and directly related to the original claim event. Most insurers prefer, and sometimes require, contractors to submit these requests directly, often utilising industry-standard estimating software like Xactimate. This ensures consistency with the insurer’s own pricing models and facilitates a smoother review process. In some instances, insurers may dispatch an adjuster back to the property to personally inspect the newly discovered damage before approving any additional payments. The timeframe for this process can vary significantly, ranging from a few days to several weeks, depending on the insurer’s current workload, the complexity of the claim, and the clarity of the documentation provided.

Dispute Resolution Options

If a supplement claim is denied, or if the insurer steadfastly refuses to adjust the payout despite clear and compelling discrepancies, policyholders may need to escalate the matter. Most reputable insurance companies have an internal appeals process. This allows claimants to formally request a second review of their claim. This often involves submitting additional, compelling documentation, such as independent contractor estimates that contradict the insurer’s figures, expert opinions from surveyors or engineers, or detailed reports that further challenge the insurer’s initial assessment. In some cases, insurers may assign a different, senior adjuster to reassess the damage, which can sometimes, but not always, lead to a revised and more favourable payment.

For more formal and structured disputes, many insurance policies include an appraisal clause. This clause allows both the policyholder and the insurer to each hire their own independent appraiser to determine the true extent and cost of the repairs. If these two appraisers cannot reach a consensus, a neutral umpire, agreed upon by both parties, is brought in to make the final, binding decision. This appraisal process can often be less adversarial and generally faster than pursuing full-blown litigation. However, if appraisal does not successfully resolve the issue, policyholders may consider filing a formal complaint with their state’s or country's insurance regulatory agency (such as the Financial Conduct Authority or the Financial Ombudsman Service in the UK). As a last resort, legal action through arbitration or a full lawsuit may be necessary. These steps can be time-consuming, emotionally taxing, and almost certainly require hiring a solicitor, but they can be absolutely necessary if the insurer is perceived to be acting in bad faith by underpaying or outright denying a legitimate claim without sufficient justification.

Legal Considerations

When insurance companies demonstrably fail to provide a fair and equitable settlement, policyholders may indeed have legal recourse under consumer protection laws. In the UK, the Financial Conduct Authority (FCA) regulates insurance companies, and the Financial Ombudsman Service (FOS) handles complaints from consumers. These bodies ensure that insurers handle claims in good faith, meaning they must conduct thorough investigations, communicate promptly and transparently, and provide reasonable justifications for their decisions. If an insurer is found to have acted in bad faith – for example, by unreasonably delaying payments, misrepresenting policy terms, or wrongfully denying valid claims without proper cause – policyholders may be entitled to additional compensation, which could include damages for financial losses incurred and even legal fees.

Filing a lawsuit against an insurer requires strong, well-organised evidence. This includes all correspondence with the insurance company, detailed contractor estimates, expert reports (e.g., from structural engineers or surveyors), and any other documentation that supports your claim. In many cases, policyholders may first be required to go through mediation or arbitration, as stipulated by their policy’s dispute resolution clause, before proceeding to court. While the concept of punitive damages is less common in the UK legal system compared to some other jurisdictions, if an insurer’s conduct is particularly egregious or demonstrates a systemic failure, the FOS or courts may apply remedies that go beyond the direct claim amount. Consulting with a solicitor who specialises in insurance disputes is paramount. They can help you determine the best course of action, especially if the claim involves a substantial sum of money or is causing ongoing financial hardship.

Comparative Table: Insurer's Estimate vs. Contractor's Estimate

| Feature | Insurer's Estimate | Contractor's Estimate |

|---|---|---|

| Basis of Cost | Standardised databases, regional averages, potentially outdated pricing. | Actual market rates, local labour costs, current material prices. |

| Hidden Damage | Often overlooks damage not immediately visible during initial inspection. | Identifies and includes underlying issues discovered during thorough inspection. |

| Permits/Compliance | May exclude necessary permit fees and costs for code upgrades. | Typically includes all required permit fees and compliance costs. |

| Material/Labour Costs | Fixed rates, potentially lower than current market demand. | Reflects current market rates, demand-driven pricing, and skilled labour. |

| Scope of Work | Focuses primarily on visible, direct damage, sometimes favouring repair over replacement. | Broader scope, includes all necessary repairs, even if underlying or requiring full replacement. |

Frequently Asked Questions (FAQs)

Q1: What exactly is a deductible and how does it affect my payout?

A1: A deductible is the amount of money you must pay out of pocket before your insurance coverage begins. For example, if your deductible is £500 and your repair bill is £2,000, the insurer will pay £1,500, and you pay the initial £500. It directly reduces the amount of the cheque you receive from your insurer.

Q2: What's the difference between Actual Cash Value (ACV) and Replacement Cost Value (RCV)?

A2: ACV pays for the cost of repairing or replacing property minus depreciation (wear and tear, age). RCV pays for the cost of repairing or replacing property with new materials of similar kind and quality, without deduction for depreciation. RCV policies typically result in higher payouts but usually have higher premiums.

Q3: Can I choose my own contractor for repairs?

A3: Yes, in most cases, you have the right to choose your own contractor. While insurers might recommend their 'approved' contractors, you are not obligated to use them. However, ensure your chosen contractor is reputable, provides a detailed estimate, and is willing to work with your insurance company.

Q4: How long does it typically take for a supplement claim to be processed?

A4: The processing time for a supplement claim can vary significantly, often ranging from a few days to several weeks. It depends on the complexity of the additional damage, how quickly your contractor submits the necessary documentation, and your insurer's current workload.

Q5: When should I consider getting a solicitor involved in an insurance claim dispute?

A5: You should consider consulting a solicitor if your insurer is denying a legitimate claim without clear justification, significantly underpaying, or acting in bad faith (e.g., unreasonable delays, misrepresenting policy terms). A solicitor can advise on your legal rights and the best course of action, especially if the claim is substantial or if internal dispute resolution processes have failed.

If you want to read more articles similar to Insurance Payouts: Bridging the Repair Cost Gap, you can visit the Insurance category.