24/05/2022

Dealing with a car accident can be a stressful experience, and the aftermath of getting your vehicle repaired often adds to that burden. However, understanding how your car insurance policy handles claims and repairs can significantly streamline the process, ensuring your vehicle is fixed efficiently and without unnecessary delays or expenses. Knowing the right steps to take from the moment of the accident through to the final repair payment can make a world of difference in getting back on the road with confidence.

This guide will walk you through the typical journey of a car insurance claim, from the initial notification to the final resolution, equipping you with the knowledge to navigate the system effectively.

Claim Initiation: Your First Steps

The moment you realise you need to make an insurance claim, the clock starts ticking. Prompt notification is key. Most insurance policies stipulate that you must report an incident as soon as reasonably possible, often within a 24 to 72-hour window. Failing to do so can sometimes lead to your claim being denied, especially if the delay raises suspicions of fraud or makes it difficult to investigate the circumstances. When you contact your insurer, be prepared to provide essential details. This includes the date, time, and exact location of the accident. You'll also need to supply the names and insurance details of any other parties involved in the incident. Fortunately, insurers typically offer multiple convenient channels for reporting a claim. This could be via a dedicated phone hotline, a user-friendly mobile app, or a secure online portal. Choose the method that best suits you.

Once your claim is officially logged, the insurer will assign a dedicated claims adjuster to your case. This individual is your primary point of contact and will be responsible for gathering all necessary information, verifying the details of your policy to confirm coverage, and guiding you through each subsequent step. Before you proceed too far, it's highly advisable to review your insurance contract. This document clarifies precisely what your policy covers, any limits on repair costs, and crucially, whether you are obligated to use repair shops that are approved by your insurer. Some policies mandate the use of preferred facilities, which can simplify the process, while others offer more flexibility, allowing you to choose your own mechanic. Understanding these terms upfront can prevent potential disputes and misunderstandings down the line.

It's also common for insurers to request a recorded statement about the accident. While this is a standard procedure, it's important to be cautious. Stick strictly to the factual events of the incident and avoid any speculation or unnecessary admissions of fault, as these could potentially impact the approval of your claim. If another driver was involved, their insurance company may also try to contact you. However, you are not obligated to provide them with a statement without first consulting your own insurer. It's always best to direct their enquiries through your insurer to ensure your interests are protected.

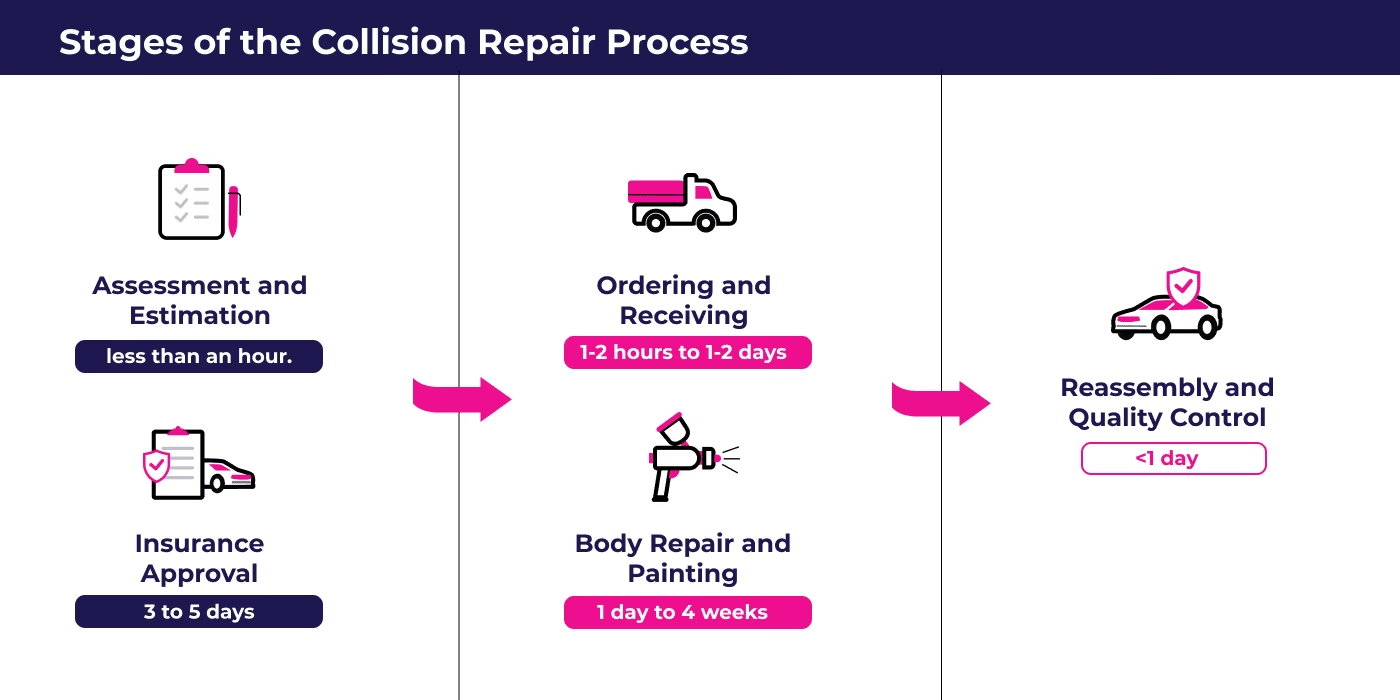

Documenting the Damage: Evidence is Crucial

Thorough documentation of the damage to your vehicle is absolutely vital for a smooth and efficient claims process. Clear, comprehensive records serve multiple purposes: they substantiate the extent of the damage, prevent potential disputes with the insurer or repair shop, and provide strong support for the repair estimates. Photographic evidence is paramount. Take as many high-resolution photos as possible, capturing the damage from various angles. Don't forget to include close-up shots of specific damaged areas as well as wider shots that show the overall condition of the vehicle. Also, photograph any debris at the scene, skid marks on the road, or any other accident-related evidence that might support your claim.

Written records add another crucial layer of support. Prepare a detailed written description of all the damage, including any mechanical issues that might not be immediately visible. If your car is still drivable, make a note of any warning lights illuminated on the dashboard or any handling problems you've noticed. This information will be invaluable when discussing repairs with both your insurer and the chosen repair shop. Obtaining a preliminary repair estimate from a trusted, independent mechanic or body shop can significantly strengthen your claim. Some insurers require multiple estimates to ensure they are offering fair pricing, so it's always recommended to keep copies of all estimates you receive and any written communication with repair shops.

Official reports and documentation from third parties can further validate your claim. If law enforcement attended the scene of the accident, obtain a copy of the police report. This provides an objective, professional account of the incident. Many insurers will require a formal damage appraisal, which can be conducted by an independent adjuster or an in-house representative from the insurance company. Keeping meticulous records of everything – including towing receipts, rental car agreements, and all correspondence with your insurer – ensures that nothing is overlooked. These organised records not only expedite the process but also serve as crucial protection should any disputes arise regarding repair costs or coverage decisions.

The Insurer's Assessment: Evaluating the Loss

Once you've filed your claim and submitted all the necessary damage documentation, the insurer will proceed to evaluate the loss and determine the extent of your coverage. A claims adjuster will meticulously review all the evidence you've provided, carefully examine the terms and conditions of your policy, and may conduct a physical inspection of the vehicle themselves. Some insurers employ their own in-house adjusters, while others utilise the services of third-party assessing companies. The findings of this assessment will directly influence the approved claim payout and the subsequent repair process.

Insurers typically employ standardised valuation methods to estimate the cost of repairs. Many rely on sophisticated software systems, such as CCC One or Mitchell Estimating, which analyse various factors including labour rates in your area, the cost of parts, and historical repair data. A critical threshold in this assessment is the concept of a 'total loss'. If the estimated cost of repairs exceeds a certain percentage of the car's actual cash value (ACV) before the accident – often set between 70% and 80% – the insurer may declare the vehicle a total loss rather than approving repairs. In such scenarios, the payout you receive will be based on the pre-accident market value of your car, taking into account factors like depreciation, mileage, and overall condition.

It's not uncommon for there to be discrepancies between the insurer's initial repair estimates and the quotes provided by your chosen body shop. If this occurs, a secondary inspection or appraisal may be necessary. An insurance appraiser might visit the repair facility, or they may request further documentation from you or the shop before approving a final settlement. It's important to remember that adjusters are often tasked with minimising claim costs for the insurer, so it is always advisable to review the insurer's estimate very carefully. If you believe the estimate seems too low, obtaining a second opinion from your repair shop and providing supporting documentation can help justify a higher payout. Don't hesitate to question an estimate that doesn't seem to reflect the true cost of the repairs needed.

Following the insurer's assessment and initial estimate, the next crucial step is the authorisation of repairs. Your insurance policy will typically specify whether you are required to use repair facilities that are part of the insurer's approved network or if you have the freedom to choose your own preferred mechanic. Shops within an insurer's Direct Repair Program (DRP) often have pre-negotiated rates with the insurance company, which can help streamline the payment process. If your policy grants you the flexibility to select an independent repair shop, the insurer will likely still need to review and approve the repair estimate before any work can commence. This ensures that the costs are in line with their assessment.

The authorisation of repairs is fundamentally dependent on the insurer's final assessment of the damage and the associated costs. If the quote provided by your chosen repair shop closely aligns with the insurer's appraisal, authorisation is usually granted without issue. However, if the shop's quote significantly exceeds the insurer's calculation, negotiations between the shop and the insurer may become necessary. In some instances, the insurer might request that the repair facility adjust its pricing to meet their estimate. Alternatively, if additional damage is discovered once the repair work has begun, the insurer may approve a supplement to cover the extra costs. Repair shops are usually adept at working directly with insurers, submitting revised estimates and supplement requests as needed to ensure the repairs are completed correctly.

Payment Resolution: Settling the Bill

Once the repairs have been authorised, the focus shifts to payment arrangements. Insurers typically handle payments in one of two ways: they will either pay the repair facility directly, or they will reimburse you, the policyholder, for the costs incurred. If you are using a repair shop that is part of the insurer's DRP, the payment process is generally very straightforward, with the insurer paying the shop directly. In this scenario, your primary responsibility is to pay your policy deductible, which is usually required before the repair work is completed. Depending on your specific coverage, your policy might also include provisions for rental car reimbursement during the period your vehicle is undergoing repairs, which can be a significant help.

If you choose to use a repair shop that is not part of the insurer's network, the process can sometimes be a little more complex. In these cases, insurers may require you to pay the repair facility upfront and then seek reimbursement from them. This can potentially lead to discrepancies if the insurer's final reimbursement amount is lower than the actual cost of the repairs. To minimise the risk of disputes and ensure a smooth reimbursement process, it is highly recommended to obtain written confirmation from your insurer detailing exactly what costs they will cover before authorising any work to begin. Should the repair shop discover additional damage during the dismantling process, they will likely need to submit a supplement request to the insurer for approval before proceeding with the additional work. Keeping meticulous records of all receipts and maintaining clear communication with both your insurer and the repair shop throughout this entire process is essential for a hassle-free reimbursement.

Dispute Resolution Processes: When Things Don't Add Up

Despite best efforts, disagreements can sometimes arise during the claims process. These might involve disputes over the cost of repairs, outright claim denials, or disagreements about the final settlement amount. Fortunately, policyholders typically have recourse to challenge the insurer's decision. Many insurers have established internal appeal processes. These allow claimants to submit additional evidence, such as independent repair estimates from other reputable shops or expert opinions, to build a case for a higher payout or a different outcome. Presenting detailed documentation, including all repair invoices, photographs, and correspondence with adjusters, can significantly strengthen your appeal.

If direct negotiations with the insurer fail to resolve the dispute, policyholders have several options for escalation. Many states offer consumer protection services through their insurance departments, where you can file formal complaints against insurers if you believe they have engaged in unfair claim settlement practices. Some insurance policies include an 'appraisal clause,' which provides a formal mechanism for resolving disputes. This clause typically allows both you and the insurer to hire independent appraisers to assess the damage and negotiate a fair resolution. If all other avenues prove unsuccessful, pursuing legal action may be a final option, although it's important to be aware that this can be a time-consuming and potentially costly route. Understanding the specific insurance regulations in your state and seeking legal advice when necessary can be invaluable in navigating these disputes effectively and achieving a fair outcome.

If you want to read more articles similar to Navigating Car Insurance Claims and Repairs, you can visit the Automotive category.