01/03/2011

Don't Settle for Less: What to Do When Your Car Insurance Write-Off Offer is Too Low

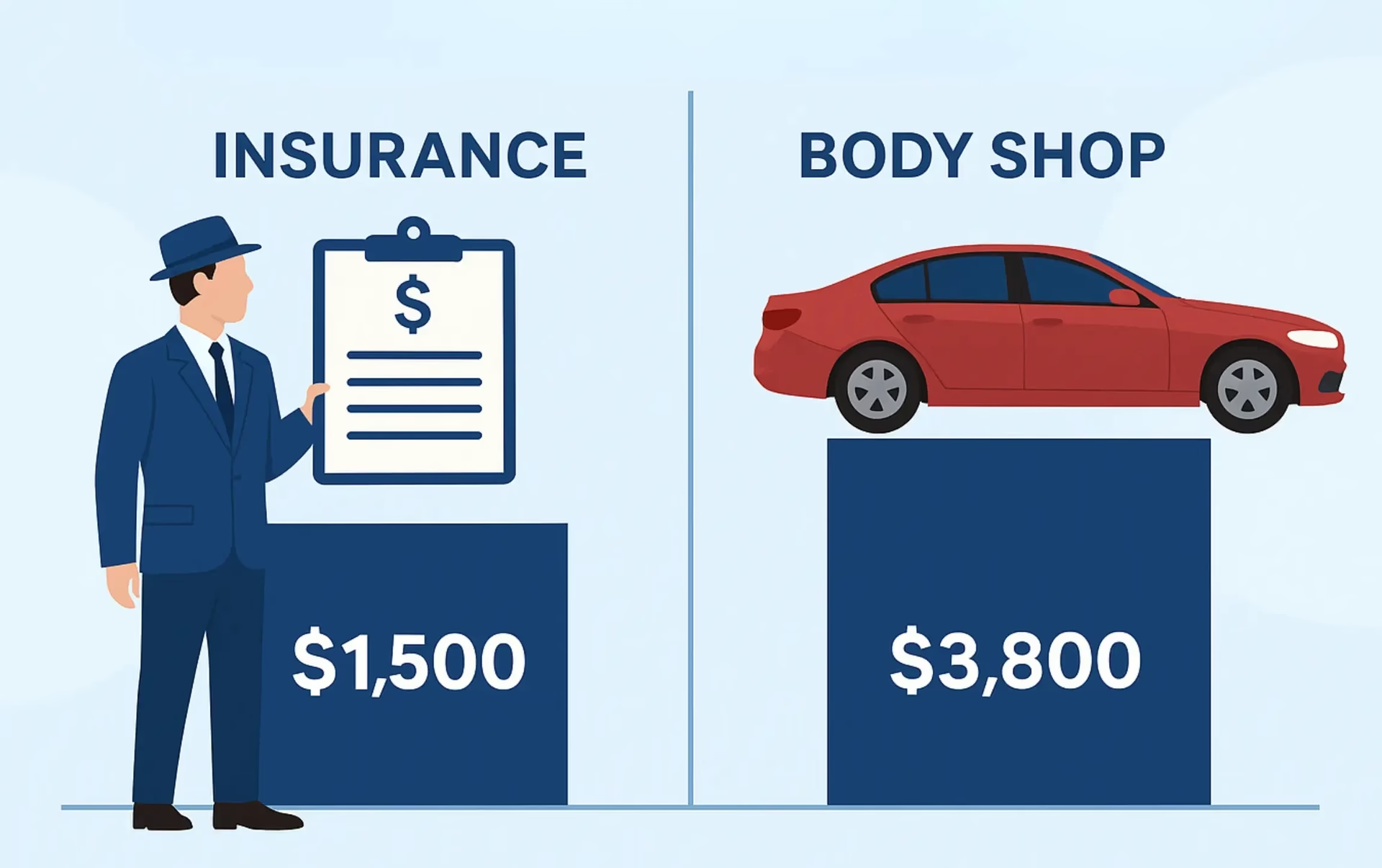

It's a disheartening moment when your car is declared a write-off by your insurance company. Even more so when the payout offered feels significantly less than what your vehicle is truly worth. Many policyholders are unaware that they possess the right to challenge an insurer's valuation, and crucially, that this process can be undertaken for free. This guide will meticulously walk you through the steps to effectively dispute an undervalued vehicle settlement, empowering you to secure the fair compensation you deserve.

Why Do Insurers Sometimes Undervalue Write-Offs?

Insurance companies typically determine a vehicle's pre-accident value (PAV) by consulting trade guides and market data. However, these calculations aren't always a true reflection of the current market price. Several factors can contribute to an insurer undervaluing your vehicle:

- Outdated or Incorrect Data: Insurers might rely on older valuation data that doesn't account for recent price fluctuations or market trends.

- Failure to Consider Vehicle Condition or Features: If your car boasted a comprehensive service history, recent valuable upgrades (like a new stereo system or alloy wheels), or was maintained in exceptional condition, its value could be considerably higher than the insurer's initial estimate. These nuances are sometimes overlooked.

- Limited Trade Guide Usage: Insurers may only consult a limited number of trade guides, potentially missing out on more favourable valuations available from other sources.

- Low Initial Offers: Some insurers adopt a strategy of presenting a lower initial offer, anticipating that policyholders will negotiate upwards. This can be a tactic to gauge the policyholder's awareness and willingness to dispute.

Can You Dispute Your Insurer's Valuation? Absolutely!

Yes, you most certainly can dispute your insurer's valuation if you believe you are being left out of pocket. Below, we outline five straightforward steps to help you make a write-off claim yourself:

Step 1: Request a Data Subject Access Request (DSAR)

A Data Subject Access Request (DSAR) is a powerful tool that allows you to scrutinise how your insurer arrived at their valuation. By obtaining this information, you can identify any potential flaws, errors, or missing data in their assessment. How to Request a DSAR:

- Compose a formal written request to your insurer.

- Clearly state that you wish to receive all data pertaining to their valuation under a Data Subject Access Request (DSAR).

- Specify the information you require, which might include:

- The specific trade guides they consulted.

- The precise values assigned to your vehicle from these guides.

- Any supporting data or engineering reports used in their assessment.

Under UK data protection law, insurers are typically obligated to respond to your DSAR within one month.

Step 2: Gather Independent Valuation Evidence

To mount a compelling challenge against your insurer's offer, you need independent evidence to bolster your case. This evidence should ideally come from reputable sources that reflect the current market value of your vehicle. Where to Obtain Valuations:

- AutoTrader: Browse listings for vehicles that are identical or very similar to yours in terms of make, model, year, mileage, and condition.

- Parkers Guide: This well-respected publication provides comprehensive trade valuations and market insights.

- Glass's Guide: Widely used by insurers and automotive trade professionals, Glass's Guide offers another valuable benchmark.

While some of these services may require a fee, the detailed reports they provide can be absolutely critical in substantiating your claim and proving your vehicle's true worth. It's a small investment for potentially a much larger return.

Step 3: Formally Challenge Your Insurer in Writing

Once you have gathered your independent valuations, the next crucial step is to send a formal challenge letter to your insurer. This letter needs to be clear, concise, and professional. Ensure it includes:

- Your claim reference number for easy identification.

- A clear and unambiguous statement that you believe the insurer's valuation is too low.

- Copies of the independent valuations you have obtained, clearly presented.

- A reference to the Financial Conduct Authority's (FCA) fair value principle, reminding them of their obligation to offer reasonable and transparent settlements.

Presenting your case logically and with supporting evidence is key to a successful challenge.

Step 4: Understand Your Insurer's Response

Following your formal challenge, your insurer will likely respond in one of the following ways:

- Accept Your Evidence: They may review your documentation, acknowledge its validity, and increase their payout offer accordingly.

- Negotiate: They might offer a revised amount that is higher than their initial offer but perhaps still not exactly what you believe is fair. This opens the door for further negotiation.

- Reject the Challenge: In some instances, they may stand firm on their original offer, providing justification for their stance.

If the insurer's revised offer remains unsatisfactory, you have the right to escalate the matter further.

Step 5: Escalate to the Financial Ombudsman Service (FOS)

If your insurer is unwilling to budge or continues to offer an unfair settlement, your next port of call should be the Financial Ombudsman Service (FOS). The FOS is an independent, impartial body established to resolve disputes between consumers and financial services firms, and their service is entirely free of charge. How to Complain to the FOS:

- Visit the official Financial Ombudsman Service website (www.financial-ombudsman.org.uk).

- Submit your complaint online, detailing your case.

- Crucially, include copies of all relevant documentation: your DSAR response, the independent valuations you gathered, and all correspondence exchanged with your insurer.

The FOS will meticulously review your case to determine whether the insurer's offer was fair and reasonable. While the FOS process can sometimes take several months to conclude, if they find in your favour, your insurer will be legally bound to pay the correct, higher settlement amount.

The FCA's Stance on Fair Value

The Financial Conduct Authority (FCA) is the UK's regulatory body for financial services, and it mandates that insurers must provide fair and transparent settlements to their customers. In December 2022, the FCA issued a stern warning to the industry, highlighting instances where some insurers were undervaluing claims. They reiterated insurers' obligations under fair value rules, emphasising:

- Insurers must be able to clearly justify how they calculate their vehicle valuations.

- Consumers should never feel pressured into accepting a low settlement offer.

- If a settlement is deemed unfair, the FOS is empowered to intervene and rectify the situation.

This regulatory oversight provides a strong framework for consumers seeking fair treatment.

When to Seek Professional Assistance

While you can certainly navigate this process yourself, you might prefer to enlist the help of specialists if you find the process daunting or lack the time. Companies like Allegiant offer a 'no win, no fee' service specifically designed to challenge undervalued vehicle write-off settlements. Allegiant's Process Typically Involves:

- Requesting all relevant valuation data from the insurer via DSAR.

- Sourcing independent trade guide valuations to build a strong case.

- Drafting a persuasive challenge letter, referencing FCA guidelines and relevant ombudsman decisions.

- Managing all negotiations with the insurance company on your behalf.

- Escalating your case to the FOS if a satisfactory resolution cannot be reached directly with the insurer.

With a 'no win, no fee' agreement, you only incur a fee if they successfully secure a higher settlement for you. It's important to note that their fees typically range from 18% to 36% (including VAT) of the additional amount recovered. However, the option to pursue the claim yourself for free remains entirely viable.

Conclusion: Reclaim What's Yours

If you suspect your car insurance write-off settlement offer is unfairly low, remember that you have the power to challenge it. By systematically following these steps – requesting a DSAR, gathering independent valuations, writing a formal letter of challenge, and, if necessary, escalating to the FOS – you can significantly increase your chances of receiving the compensation you rightfully deserve. Don't let a low offer go unchallenged; take action to ensure a fair outcome for your written-off vehicle. Key Takeaways:

- Challenge: Never accept an initial write-off offer if you believe it's too low.

- DSAR: Obtain your insurer's valuation data.

- Evidence: Gather independent valuations from reputable sources.

- Formalise: Write to your insurer, presenting your evidence and referencing FCA rules.

- Escalate: Use the free Financial Ombudsman Service if an agreement isn't reached.

For those seeking expert support, consider professional services that operate on a 'no win, no fee' basis to handle the complexities of your claim. Disclaimer: This article provides general information and does not constitute legal advice. Always consult with a qualified professional for advice tailored to your specific situation.

If you want to read more articles similar to Challenging Low Car Insurance Write-Off Offers, you can visit the Insurance category.