03/12/2019

It's a driver's worst nightmare: you've finally got your dream car on finance, and just six months down the line, it's involved in an accident. Whether it's a minor fender-bender or more significant damage, the immediate concern often shifts from the physical repair to the financial implications. What happens to your car payments? Who pays for the repairs? This guide will walk you through the essential steps and considerations for dealing with a damaged financed car in the UK.

- Understanding Your Finance Agreement and Insurance

- Reporting the Damage

- Repairable Damage: What Happens Next?

- Total Loss: When Your Car is Written Off

- What is Guaranteed Asset Protection (GAP) Insurance?

- What If You Can't Afford the Excess or Shortfall?

- Your Rights and Responsibilities

- Frequently Asked Questions

- Conclusion

Understanding Your Finance Agreement and Insurance

The first and most crucial step is to understand the terms of your finance agreement and your car insurance policy. Most finance agreements, particularly Conditional Sale and Hire Purchase agreements, stipulate that you must maintain comprehensive insurance cover for the vehicle. This is because the finance company technically still owns the car until the final payment is made. Your insurance policy is designed to protect both you and the lender in case of damage, theft, or write-off.

Key Documents to Review:

- Finance Agreement: Look for clauses relating to damage, total loss, and your obligations.

- Car Insurance Policy: Pay close attention to the section on accidental damage, uninsured loss, and write-off procedures.

Reporting the Damage

Regardless of who is at fault, you must report the damage to your insurance company as soon as possible. Failing to do so can invalidate your policy. When you contact your insurer, be prepared to provide details of the accident, including:

- Date, time, and location of the incident.

- Details of any other vehicles or parties involved (names, addresses, insurance details).

- A description of the damage to your car and any other property.

- Whether the police were involved and any crime reference numbers.

Your insurer will then guide you through the claims process. They will likely arrange for an assessor to inspect the damage and provide an estimate for the repair costs. They will also determine if your car is repairable or if it's a total loss.

Repairable Damage: What Happens Next?

If the damage is deemed repairable, your insurer will typically arrange for the repairs to be carried out at an approved repair centre. The repair costs will be paid directly to the garage, minus your policy's excess (the amount you agree to pay towards a claim).

Important Considerations for Repairable Damage:

- Excess Payment: Ensure you can afford to pay your policy excess.

- Repair Quality: If you have a choice, consider whether to use an approved garage or one of your own choosing. Some finance agreements may dictate this.

- Courtesy Car: Check if your insurance policy includes a courtesy car while yours is being repaired. This is often a crucial element when you rely on your vehicle for daily life.

While your car is being repaired, your finance payments will continue as normal. The damage doesn't suspend your contractual obligation to the finance company. If the repairs are substantial, the finance company may want to be assured that the repairs are carried out to a satisfactory standard.

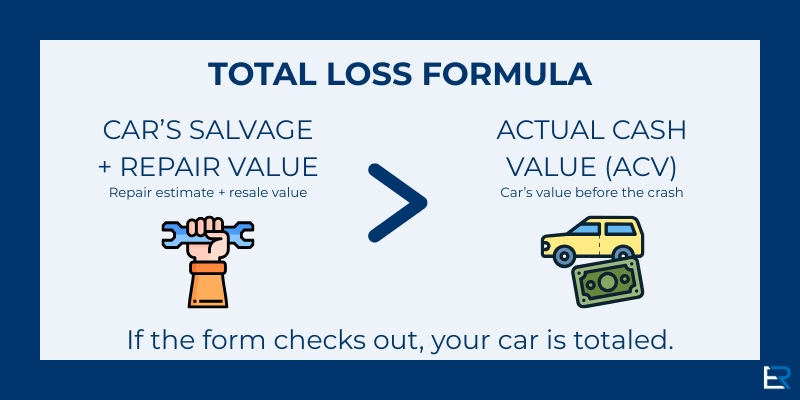

Total Loss: When Your Car is Written Off

If the cost of repairs exceeds a certain percentage of the car's pre-accident value (this threshold varies between insurers), the vehicle will be declared a total loss or a write-off. Insurers categorise write-offs into different classes:

- Category A: Scrapped and cannot be repaired or returned to the road.

- Category B: Can be broken for parts, but the shell must be scrapped.

- Category S (previously Category C): Structurally damaged but repairable. The vehicle can be repaired and returned to the road after undergoing a rigorous inspection.

- Category N (previously Category D): Non-structurally damaged but repairable. Typically, this means damage to electrics or mechanicals, but no chassis damage.

If your car is declared a total loss, your insurance company will pay out the market value of the car immediately before the accident. This payout will be based on the car's age, mileage, condition, and any optional extras, minus your excess.

How Does the Payout Work with Finance?

This is where it gets slightly more complex. The insurance payout is intended to cover the outstanding balance on your finance agreement. The insurer will typically pay the settlement amount directly to the finance company. Any remaining balance after the finance company has been paid will be given to you.

Scenario 1: Payout Exceeds Outstanding Finance

If the market value payout from your insurer is more than what you owe on your finance agreement, you will receive the difference. For example, if your car's market value is £12,000, you owe £9,000 on the finance, and your excess is £500, the insurer will pay £8,500 directly to the finance company. You will then receive the remaining £3,500. You will still need to settle your excess with the insurer, but this is usually deducted from the total payout before it's sent to the finance company.

Scenario 2: Payout is Less Than Outstanding Finance

If the market value payout is less than what you owe, this is where you might face a shortfall. For instance, if your car's market value is £10,000, but you still owe £12,000 on the finance, the insurer will pay the £10,000 (minus your excess) to the finance company. You will then be liable for the remaining £2,000 (plus your excess if not already deducted). This is a critical situation, and you will still need to pay this outstanding amount to the finance company to settle the agreement. Failure to do so could have severe consequences for your credit rating.

What is Guaranteed Asset Protection (GAP) Insurance?

This is where GAP insurance becomes invaluable, especially for newer cars on finance. GAP insurance is designed to cover the difference between the market value payout from your insurer and the outstanding balance on your finance agreement in the event of a total loss. If you took out GAP insurance when you financed your car, it would pay out the shortfall, ensuring you are not left with a debt for a car you no longer possess.

Types of GAP Insurance:

- Return to Invoice (RTI): Covers the difference between the insurance payout and the original price you paid for the car.

- Vehicle Replacement: Pays the difference to buy a brand-new replacement car of the same make and model.

- Finance GAP: Specifically covers the shortfall on your finance agreement.

If you didn't take out GAP insurance, you will need to discuss options with your finance company to settle the remaining debt. They may offer alternative finance arrangements, but this is not guaranteed.

What If You Can't Afford the Excess or Shortfall?

If you find yourself unable to pay the excess or the shortfall on your finance agreement, it's crucial to communicate this with your insurance company and finance provider immediately. They may have options available, such as payment plans, but don't delay in making contact. Ignoring the problem will only worsen the situation, potentially leading to further charges and damage to your credit history.

Your Rights and Responsibilities

As the person responsible for the car under the finance agreement, you have a responsibility to keep it in good condition and insured. However, you also have rights:

- Right to Fair Treatment: Your insurer and finance company must treat you fairly and adhere to the terms of your agreements.

- Right to Information: You have the right to be clearly informed about the claims process, repair assessments, and payout calculations.

- Responsibility to Cooperate: You must cooperate fully with your insurer and provide all necessary information promptly.

Frequently Asked Questions

Q1: Do I have to use the garage recommended by my insurer?

A1: In most cases, you can choose your own garage, but your insurer may only cover repairs up to the cost estimated by their approved repairer. Check your policy terms and conditions, and discuss this with your insurer. Some finance agreements may also have stipulations on approved repairers.

Q2: What happens if my car is stolen and on finance?

A2: If your car is stolen, you must report it to the police and your insurance company immediately. If the car is not recovered, your insurance company will treat it as a total loss and pay out according to the market value, minus your excess. The payout will then be used to settle your finance agreement, with any remainder returned to you. Again, GAP insurance is vital here.

Q3: Can I keep the car if it's written off?

A3: Generally, no. If your car is declared a total loss, the insurance company takes ownership of the salvage (the damaged vehicle) and pays out its value. If you wish to keep the car, you would need to negotiate with the insurer to buy the salvage back from them, but this is usually only an option for Category S or N write-offs, and you would still need to settle the finance agreement and cover repair costs.

Q4: How long does the claims process usually take?

A4: The timeline can vary significantly depending on the complexity of the damage, the availability of parts, and the efficiency of the insurer and repairer. For minor repairs, it might take a few days to a week. For total loss settlements, it can take several weeks to a few months from the initial claim to the final payout and settlement of the finance.

Conclusion

Dealing with a damaged financed car can be a stressful experience, but by understanding your rights, responsibilities, and the processes involved, you can navigate it more effectively. Always keep your finance agreement and insurance policy details to hand, report any damage promptly, and communicate openly with your insurer and finance provider. While unfortunate, an accident doesn't have to mean financial ruin if you are well-informed and proactive.

If you want to read more articles similar to Damaged Financed Car: What Now?, you can visit the Insurance category.