23/07/2007

Experiencing a car accident can be a jarring and stressful event, leaving you shaken and unsure of what to do next. Beyond the immediate shock, the thought of dealing with insurance companies and navigating the claims process can add another layer of anxiety. However, understanding the steps involved and being prepared can significantly ease the burden, making your car insurance claim as smooth and straightforward as possible. This comprehensive guide will walk you through everything you need to know, from the moment an incident occurs to the final resolution of your claim.

- Immediate Steps After an Incident

- The Car Insurance Claims Process Explained

- How Long Does a Car Insurance Claim Take?

- Can You Cancel a Car Insurance Claim?

- Understanding Your Policy: Comprehensive vs. Third-Party

- Impact on Your No Claims Discount (NCD)

- Common Pitfalls to Avoid

- Frequently Asked Questions (FAQs)

- Conclusion

Immediate Steps After an Incident

Your actions immediately following an incident are crucial and can greatly influence the success and speed of your insurance claim. Prioritise safety first, then focus on gathering information.

Safety First

- Ensure Safety: First and foremost, check for injuries to yourself and anyone else involved. If anyone is injured, call emergency services immediately (999 in the UK).

- Move to Safety: If possible and safe to do so, move your vehicle to the side of the road or a safe location to prevent further accidents. If the vehicles are too damaged to move, turn on your hazard lights.

Gathering Crucial Information

Once safety is secured, begin collecting details. The more information you can provide to your insurer, the quicker and more efficiently they can process your claim. For anyone else involved in the incident, you'll need to gather:

- Personal Details: Their full name, address, and contact number.

- Vehicle Details: Make, model, colour, and registration number of their vehicle.

- Insurance Details: Their insurance company and policy number, if they have it to hand.

- Witness Details: If there were any independent witnesses, try to get their name and contact number. Their unbiased account can be invaluable.

- Police Involvement: If the police attended, note down the police force, incident number, and the name/collar number of the attending officer(s). This is particularly important if there were injuries, significant damage, or if a crime was committed (e.g., hit and run).

Beyond the other party's details, you must also note down specifics about the incident itself:

- Location: The exact road name, nearest junction, or a clear landmark. Postcodes are ideal if available.

- Time and Date: The precise time and date the incident occurred.

- Weather Conditions: Note the weather at the time (e.g., raining, foggy, sunny).

- Road Conditions: Any relevant road conditions (e.g., icy, wet, potholes).

- Damage: A detailed description of the damage to all vehicles involved.

- Photographs: Take clear photographs from multiple angles. Include damage to all vehicles, the position of the vehicles, road markings, traffic signs, and any relevant surroundings. Even a description of the driver may help if they weren't clearly included in your pictures or if you suspect they weren't the registered keeper.

- Diagram: A simple sketch of how the incident happened can be surprisingly helpful.

Crucial Tip: Do not admit fault at the scene, even if you think you might be to blame. This is for your insurer to determine after a full investigation. Stick to factual information.

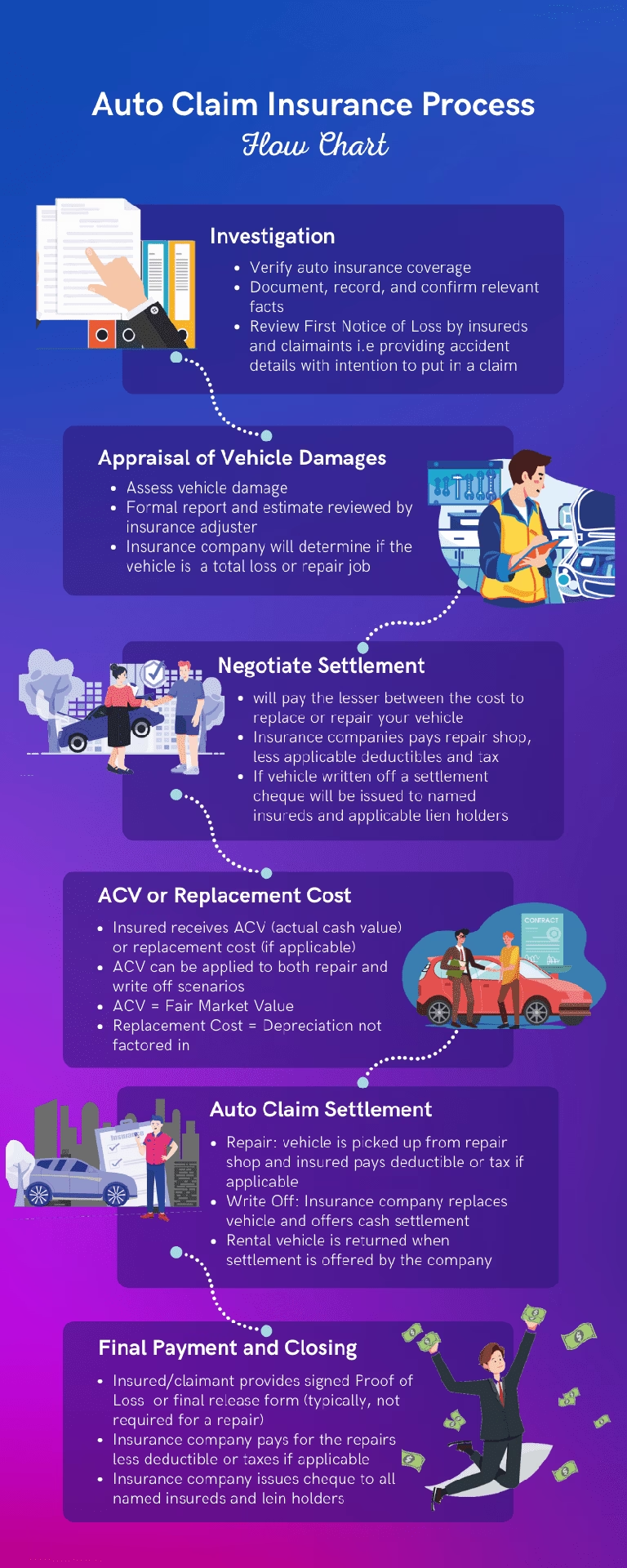

The Car Insurance Claims Process Explained

Once you've gathered all necessary information, the next step is to contact your insurer. The process typically follows these stages:

1. Reporting the Claim

Contact your insurance company as soon as possible, ideally within 24-48 hours of the incident, even if you don't intend to make a claim initially or if the damage seems minor. Most insurers have a dedicated claims line available 24/7. Provide them with all the information you've gathered. They will open a claim file and give you a claim reference number.

2. Initial Assessment and Investigation

Your insurer will review the details you've provided. Depending on the complexity, they may appoint a loss adjuster or an engineer to assess the damage to your vehicle. If a third party is involved, your insurer will also contact their insurer to gather their version of events.

3. Determining Liability

This is often the most time-consuming part. Insurers exchange information, evidence (such as photos, witness statements, police reports), and legal arguments to determine who was at fault. This can be straightforward if one party clearly admitted fault or if the evidence is conclusive, but it can become complex if there are conflicting accounts or no witnesses. The determination of liability directly impacts who pays for what.

4. Vehicle Repair or Total Loss

Once liability is established and damage assessed, your insurer will decide whether your car can be repaired economically or if it's a 'total loss' (also known as 'written off').

- Repair: If repairable, your insurer will arrange for your car to be fixed at an approved garage. You may need to pay your excess at this stage.

- Total Loss: If your car is a total loss, your insurer will pay you the market value of your vehicle at the time of the incident, minus any applicable excess.

5. Settlement

The final stage involves the financial resolution of the claim. This includes payment for repairs, total loss payouts, and potentially compensation for personal injuries or other losses (e.g., hire car costs). Once all aspects are settled, the claim will be closed.

How Long Does a Car Insurance Claim Take?

The duration of a car insurance claim can vary significantly. As the provided information states, an insurance claim will remain open until any uncertainty has been settled. That means your claim could take days to quickly confirm, or months to sort out. Several factors influence the timeline:

| Factor | Impact on Claim Duration |

|---|---|

| Complexity of Incident | Simple, single-vehicle incidents are typically resolved quicker. Multi-vehicle accidents or those involving significant injuries take much longer due to multiple parties, medical assessments, and detailed investigations. |

| Disputed Liability | If there's disagreement over who was at fault, insurers will engage in extensive communication and investigation, prolonging the process. This is a common reason for delays. |

| Third-Party Cooperation | Delays can occur if the third party or their insurer is slow to respond or provide necessary information. |

| Extent of Damage/Injuries | Extensive vehicle damage requires more time for assessment and repair. Personal injury claims, especially complex ones, can take years to settle as medical prognoses need to be established. |

| Information Provided | The more complete and accurate the information you provide at the outset, the faster your insurer can process the claim. Missing details lead to delays. |

| Legal Action | In rare cases, if liability cannot be agreed upon, the matter may proceed to court, significantly extending the claim duration. |

Can You Cancel a Car Insurance Claim?

Yes, you can cancel a car insurance claim. This is a common question, and there are several reasons why you might consider doing so:

- Minor Damage: You might realise the damage is minor and cheaper to repair out-of-pocket than to claim, especially if the repair cost is less than or close to your policy's voluntary and compulsory excess.

- Protecting No Claims Discount: Even if you are not at fault, some insurers may still reduce your No Claims Discount (NCD) if the claim is made through your policy, unless the cost is fully recovered from the third party. Cancelling a claim can protect your NCD.

- Change of Mind: You might simply decide you no longer wish to pursue the claim.

If you decide to cancel, contact your insurer immediately. Be aware that if your insurer has already incurred costs (e.g., for vehicle recovery or assessment), they may not be recoverable, and they might still record the 'incident' even if no claim is paid out. This incident could potentially still affect future premiums, although usually less so than a full paid-out claim.

Understanding Your Policy: Comprehensive vs. Third-Party

Your type of insurance policy plays a significant role in what you can claim for:

- Third-Party Only (TPO): This is the minimum legal requirement. It covers damage or injury you cause to a third party's vehicle or property, and injury to their passengers or pedestrians. It does NOT cover damage to your own vehicle.

- Third-Party, Fire and Theft (TPFT): This offers TPO cover, plus protection against your vehicle being stolen or damaged by fire.

- Comprehensive: This is the highest level of cover. It includes everything covered by TPFT, and crucially, it also covers damage to your own vehicle, regardless of who was at fault. It often includes additional benefits like personal accident cover, legal expenses, and courtesy car provision.

Having a comprehensive policy is generally recommended as it provides the most extensive protection, ensuring you're covered for your own vehicle's repairs or replacement.

Impact on Your No Claims Discount (NCD)

Making a claim, particularly an 'at-fault' claim, will almost certainly affect your No Claims Discount (NCD), also known as No Claims Bonus (NCB). This is a discount applied to your premium for each year you drive without making a claim. An at-fault claim means your insurer could not recover their costs from another party. Even a 'non-fault' claim, where your insurer pays out initially and then recovers costs from the third party's insurer, can sometimes impact your NCD if the recovery process is not 100% successful or if you don't have NCD protection.

Many drivers opt to pay an extra premium to 'protect' their NCD. This typically allows you to make one or two claims within a certain period without losing your full NCD, though it may still be reduced slightly.

Common Pitfalls to Avoid

To ensure your claim proceeds smoothly, be mindful of these common mistakes:

- Delaying Notification: Always report the incident to your insurer promptly, even if you are just informing them for now. Policy terms often require quick notification.

- Admitting Fault: Never admit fault at the scene, verbally or in writing. This can prejudice your insurer's ability to defend your position.

- Providing Incomplete Information: The more details you collect at the scene, the better. Missing information can lead to delays and complications.

- Not Documenting Everything: Photos, witness details, police reference numbers – these are your best friends in a claim.

- Ignoring Communication: Respond promptly to your insurer's requests for information or actions. Delays on your part will delay the claim.

Frequently Asked Questions (FAQs)

What if the other driver is uninsured?

If the other driver is uninsured, your insurer will still process your claim. If you have comprehensive cover, they will pay for your repairs and attempt to recover costs from the uninsured driver, though this is often difficult. If you only have third-party cover, you may be out of pocket for your own vehicle's damage unless you can pursue the uninsured driver through the Motor Insurers' Bureau (MIB).

What if I don't have all the details of the other party?

Provide your insurer with as much information as you have (e.g., vehicle make/model/colour, partial registration, driver description, location). They have tools to try and identify the other party, especially with a full registration number. Without details, it becomes much harder to pursue a claim against them.

Generally, yes. Even a non-fault claim can sometimes lead to an increase, as insurers may view you as a higher risk, regardless of fault. An at-fault claim is almost certain to increase your premium, and you will likely lose some or all of your No Claims Discount.

What is an excess?

The excess is the amount you agree to pay towards a claim before your insurer pays the rest. Most policies have a compulsory excess (set by the insurer) and a voluntary excess (chosen by you to reduce your premium). For example, if your excess is £250 and your repairs cost £1000, you pay £250 and your insurer pays £750. If the claim is non-fault and your insurer recovers all costs from the third party, your excess is usually reimbursed to you.

How long do I have to make a claim?

Most insurers require you to report an incident as soon as reasonably possible. While there isn't always a strict legal deadline for reporting to your insurer, delaying can complicate matters. Legally, you typically have six years to make a property damage claim and three years for a personal injury claim from the date of the incident (or date of knowledge for injuries).

What if I disagree with my insurer's decision?

If you're unhappy with your insurer's decision or the way your claim has been handled, first follow their internal complaints procedure. If you're still not satisfied after exhausting their complaints process, you can escalate your complaint to the Financial Ombudsman Service (FOS). The Ombudsman is an independent service that resolves disputes between consumers and financial services firms.

Conclusion

While no one wishes to be in a car accident, being prepared and understanding the car insurance claims process can significantly reduce stress and ensure a smoother resolution. By acting quickly, gathering comprehensive information, and communicating effectively with your insurer, you put yourself in the best position for a successful claim. Remember, your insurer is there to help, but providing them with all the necessary details is key to unlocking that support efficiently.

If you want to read more articles similar to Navigating Your Car Insurance Claim Smoothly, you can visit the Insurance category.