04/02/2004

Every driver knows the feeling: that sickening crunch, the sudden scrape against a low wall, or the inexplicable dent that appears overnight. While major accidents are covered by your standard car insurance, what about those minor imperfections that chip away at your car's pristine appearance? This is where cosmetic car insurance steps in, offering a specialised solution for the everyday wear and tear that can otherwise leave a lasting mark – not just on your vehicle, but on your wallet and no-claims bonus too.

Often referred to as scratch and dent insurance, or even cosmetic repair insurance, this specific type of cover is designed to address those frustrating minor damages that don't impact your car's functionality but certainly spoil its aesthetic appeal. From those annoying car park dings to the scuffs that mysteriously appear on your bumper, cosmetic car insurance aims to keep your vehicle looking as good as new without the significant repercussions of claiming on your main policy. But how exactly does it work, what does it cover, and is it truly worth the extra investment?

- What Exactly is Cosmetic Car Insurance?

- Why Consider Cosmetic Car Insurance? The Impact on Your Main Policy

- What Damage Does Cosmetic Car Insurance Typically Cover?

- How to Acquire Cosmetic Car Insurance

- Cosmetic vs. Standard Car Insurance: A Comparison

- Common Questions About Cosmetic Car Insurance

- Is Cosmetic Car Insurance Worth the Investment?

What Exactly is Cosmetic Car Insurance?

Cosmetic car insurance is a dedicated insurance product tailored to cover the costs of minor, superficial damage to your vehicle's exterior. Unlike your comprehensive car insurance, which handles larger, more significant incidents like collisions or theft, cosmetic cover focuses exclusively on those smaller blemishes that are an inevitable part of car ownership. Think of it as a protective layer for your car's paintwork and bodywork, ensuring that minor scrapes, scratches, and dents can be rectified quickly and efficiently.

The primary benefit of this type of policy is its ability to allow you to repair cosmetic damage without making a claim on your main car insurance policy. This distinction is crucial because claiming for minor damage on your standard policy can have undesirable consequences, such as the loss of your hard-earned no-claims bonus (NCB) and potentially higher premiums in subsequent years. Cosmetic car insurance bypasses this dilemma, offering a separate avenue for repairs that keeps your primary policy untouched and your NCB intact.

Why Consider Cosmetic Car Insurance? The Impact on Your Main Policy

For many drivers, the thought of a small scratch or dent isn't worth involving their main car insurance. And for good reason. While your standard policy will likely cover scratches and dents resulting from vandalism or certain other causes, the financial implications of making such a claim can often outweigh the cost of the repair itself, particularly for minor damage.

Firstly, there's the excess. When you claim on your standard car insurance, you'll almost certainly have to pay an excess – a predetermined amount that you contribute towards the cost of the repair. For many, this excess can be set at £250 or even higher, depending on your policy. If the repair for a minor scratch costs, say, £150, paying a £250 excess simply doesn't make financial sense. In such cases, you'd be better off paying for the repair out of your own pocket. Cosmetic car insurance, however, typically has a much lower excess, or sometimes no excess at all, making it a more viable option for smaller repairs.

Secondly, and arguably more significantly, is the impact on your no-claims bonus. Your NCB is one of the most valuable assets you can accumulate as a careful driver, offering substantial discounts on your annual premiums. Making a claim on your main policy, even for minor cosmetic damage, can jeopardise this bonus. Insurers often report that a single claim can lead to a significant drop in your NCB, potentially increasing your premium by a considerable percentage in the following year. Data suggests that dropping from a one-year NCB to none could see your premium increase by over a third, which is a substantial financial hit for a minor scuff.

Finally, your claims history is something that car insurance providers closely examine when calculating future premiums. Even if a claim doesn't fully wipe out your NCB, having a history of claims, even for small incidents, can flag you as a higher risk in the eyes of insurers, pushing up your costs in the long run. Cosmetic car insurance helps you avoid this by keeping these minor repairs off your main claims record.

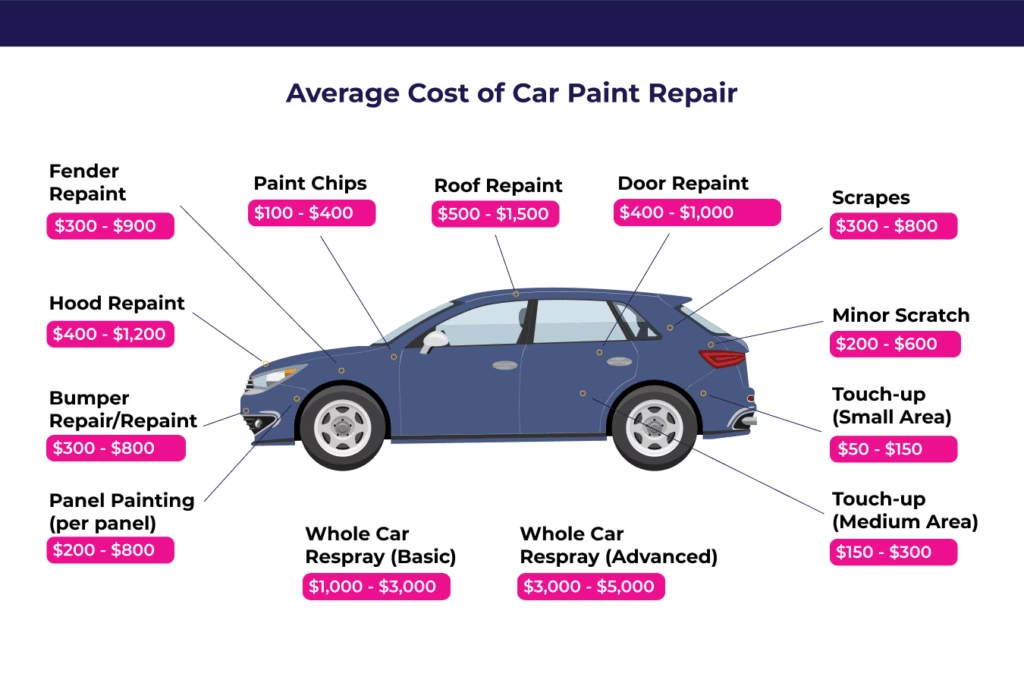

What Damage Does Cosmetic Car Insurance Typically Cover?

Cosmetic damage is generally defined as small exterior imperfections that do not affect the structural integrity or functionality of your vehicle. While the exact definitions can vary slightly between insurers, the types of damage typically covered by cosmetic car insurance include:

- Scrapes and Scratches: Surface marks on the paintwork, from light abrasions to deeper scratches that haven't compromised the panel's integrity.

- Small Dents: Minor indentations on body panels, usually without paint damage or sharp creases. These are often the result of car park dings or light impacts.

- Stone Chips: Small chips in the paintwork caused by stones or debris flicked up from the road.

- Minor Bumper Damage: Light scuffs or scrapes on the plastic bumpers, often from parking incidents.

It's important to understand the limitations, however. Cosmetic car insurance is not designed for extensive or structural damage. This means that if your car has suffered significant impact, requires entire panels to be replaced, or has damage that affects its safety or drivability, this would fall under your standard comprehensive policy, not your cosmetic cover. Always check your specific policy documents to confirm the exact scope of your coverage.

Many of these minor repairs are carried out using a technique known as SMART Repair (Small to Medium Area Repair Technology). This innovative method allows technicians to repair localised damage without needing to repaint entire panels. It's typically less expensive, quicker, and often allows for repairs to be conducted at your home or workplace, providing immense convenience and minimising disruption to your day.

How to Acquire Cosmetic Car Insurance

Getting cosmetic car insurance isn't quite as straightforward as comparing standard car insurance policies, as it's not widely offered through comparison websites. Generally, there are two main avenues for obtaining this type of cover:

- As an Add-on to Your Standard Policy: Some car insurance providers offer cosmetic damage cover as an optional extra when you're purchasing or renewing your main policy. While comparison sites might not list it as a selectable option, it's always worth calling your preferred insurer directly to inquire if they offer it and what the additional cost would be.

- As a Standalone Policy: You can also purchase cosmetic car insurance as a completely separate, standalone policy from specialist insurers. Again, you'll need to go directly to these providers to get a quote and arrange cover, as they are not typically featured on general insurance comparison platforms.

Given that comparison sites don't usually feature this type of insurance, a bit of direct research and phone calls might be necessary to find the best deal for your needs. Always ensure you fully understand the terms, conditions, excesses, and limitations of any policy before committing.

Cosmetic vs. Standard Car Insurance: A Comparison

To help illustrate the difference and why cosmetic cover can be beneficial, let's compare how different scenarios might play out with and without it:

| Scenario | Standard Insurance Action | Cosmetic Insurance Action | Financial & Policy Impact |

|---|---|---|---|

| Minor Car Park Dent | Claim on main policy, pay excess (£250+). | Claim on cosmetic policy, pay low/no excess. | Standard: NCB likely affected, future premiums may rise. Cosmetic: NCB protected, minor cost, quick repair. |

| Significant Collision Damage | Claim on main comprehensive policy, pay excess. | Not covered by cosmetic policy. | Standard: NCB likely affected, significant claim on record. Cosmetic: No impact, as it's not designed for major damage. |

| Stone Chip on Bonnet | Claim on main policy (unlikely due to excess). | Claim on cosmetic policy. | Standard: Likely pay out-of-pocket as excess is too high. Cosmetic: Covered, protecting appearance and main policy. |

| Vandalism Scratch | Claim on main policy, pay excess. | Claim on cosmetic policy (if vandalism is covered). | Standard: NCB at risk. Cosmetic: NCB protected, specific minor damage handled. |

Common Questions About Cosmetic Car Insurance

Will a dent cause my car to fail its MOT?

It depends entirely on the nature and severity of the dent. A small, superficial dent or scratch that doesn't compromise the car's structure or safety is highly unlikely to cause an MOT failure. The MOT inspection focuses on the car's roadworthiness and safety. However, if the damage is significant, makes the car unsafe, or affects critical structural components, then yes, your car would fail.

During the MOT, the mechanic inspects the body condition for any issues that could compromise safety. Your car might fail if it has:

- Body panels that are insecure, extensively damaged, or corroded to the point of being likely to cause injury.

- A body pillar (which connects the roof to the lower part of the car) that is so insecure that the stability or security of the vehicle is impacted.

It's not just physical damage; any unsafe modifications that negatively impact crucial systems like braking or steering will also result in an MOT failure. For full details on what constitutes a major or dangerous issue, it's always best to consult the official GOV.UK guidance.

What if someone hits my car and drives off?

This is an incredibly frustrating scenario, and unfortunately, it happens all too often. If you don't have cosmetic car insurance, your options are limited, and neither is particularly appealing:

- Pay for the repairs yourself: This means bearing the full cost out of your own pocket, which can be a bitter pill to swallow for damage you didn't cause.

- Claim on your main insurance: While your comprehensive policy might cover hit-and-run incidents, this again brings up the issue of paying your excess and, more importantly, potentially impacting your no-claims bonus and increasing your premiums for the following year.

If you had cosmetic car insurance, however, you would typically be covered for minor damage resulting from such an incident without having to involve your main policy or jeopardise your valuable no-claims bonus. It offers a much smoother and less financially impactful resolution.

The cosmetic damage itself doesn't directly affect your car insurance premiums. What affects your premiums is claiming for that damage on your standard car insurance policy. As discussed, making a claim, even for a minor scratch or dent, can lead to two primary financial impacts:

- Loss of No-Claims Bonus (NCB): Each claim on your main policy can reduce your NCB, leading to higher renewal premiums.

- Increased Future Premiums: Beyond the NCB, insurers consider your claims history. A history of claims, even small ones, can signal a higher risk, causing your premiums to increase over time.

This is precisely why cosmetic car insurance exists. By providing a separate mechanism for repairing minor damage, it allows you to keep your main policy clean, protecting your NCB and preventing those minor incidents from escalating into higher insurance costs in the long run. So, while cosmetic damage itself isn't the issue, how you choose to address it – either by paying out of pocket, claiming on your main policy, or utilising cosmetic insurance – absolutely dictates its impact on your future premiums.

Is Cosmetic Car Insurance Worth the Investment?

Deciding whether cosmetic car insurance is a worthwhile investment largely depends on your personal circumstances, priorities, and driving habits. For some, it's a non-negotiable part of keeping their car in pristine condition, while for others, it might seem like an unnecessary extra expense.

Here are some factors to consider:

- Your Driving Environment: Do you frequently park in busy car parks? Drive on roads prone to stone chips? If your car is regularly exposed to situations where minor damage is likely, cosmetic cover could save you money and hassle in the long run.

- Your Attitude to Imperfections: If you're someone who likes your car to look immaculate and finds even the smallest scratch bothersome, then the peace of mind offered by cosmetic insurance might be invaluable.

- Your No-Claims Bonus: If you've built up a significant no-claims bonus and are keen to protect it at all costs, cosmetic cover is an excellent way to address minor damage without impacting your main policy.

- Cost vs. Benefit: Weigh the annual premium of the cosmetic policy against the potential costs of paying for minor repairs yourself or the financial hit of claiming on your main policy (excess + increased future premiums). For frequent minor repairs, it can quickly pay for itself.

Ultimately, if you want to maintain your car's aesthetic appeal without incurring substantial costs or jeopardising your main insurance policy, cosmetic car insurance could be a very sensible option. It offers a dedicated solution for those annoying bumps and scrapes, ensuring your vehicle retains its showroom look and your insurance premiums stay as competitive as possible. While it requires a bit of direct research to find, the benefits of protecting your no-claims bonus and avoiding future premium hikes for minor scuffs might make it a smart addition to your overall car insurance strategy.

If you want to read more articles similar to Cosmetic Car Insurance: Keep Your Ride Pristine, you can visit the Insurance category.