15/08/2008

A car accident, no matter how minor, can be a stressful experience. Beyond the immediate shock and inconvenience, one of the first questions that typically springs to mind is: how much is this going to cost me? The truth is, there's no single answer to that question. Car accident repair costs in the UK can vary wildly, ranging from a couple of hundred quid for a minor scuff to many thousands for significant structural damage, sometimes even leading to your vehicle being written off. Understanding the myriad factors that influence these costs is crucial for navigating the aftermath of an incident and making informed decisions about repairs.

The price you'll pay depends on a complex interplay of variables, including the severity and type of damage, the make and model of your vehicle, the specific parts required, the labour rates of the chosen garage, and whether you're involving your insurance company. Let's delve deeper into what determines these costs and what you can expect when facing a repair bill.

- Key Factors Influencing Car Accident Repair Costs

- Estimated Costs for Common Car Accident Repairs (UK)

- Insurance Claim vs. Paying Out-of-Pocket

- Getting a Repair Estimate

- When is a Car a 'Write-Off'?

- Tips for Managing Repair Costs

- Frequently Asked Questions (FAQs)

- Q1: Will my insurance premium go up if I make a claim?

- Q2: How long do car accident repairs typically take?

- Q3: Should I use an approved repairer recommended by my insurer?

- Q4: What if hidden damage is found after the initial estimate?

- Q5: Is it safe to drive a car after an accident if it looks okay?

Key Factors Influencing Car Accident Repair Costs

Several critical elements contribute to the final price tag of a car repair after an accident. Being aware of these can help you anticipate expenses and understand the quotes you receive.

1. Severity and Type of Damage

This is arguably the most significant factor. A small scratch on a bumper will naturally cost far less to fix than a crumpled wing or a bent chassis. Damage can be broadly categorised:

- Cosmetic Damage: This includes scratches, scuffs, minor dents, and paint chips. While unsightly, they rarely affect the car's functionality or safety. Repairs typically involve sanding, filling, painting, and polishing.

- Panel Damage: This refers to more substantial damage to body panels like doors, wings, bonnets, or boots. Depending on the extent, panels might be repaired (panel beating, filling, painting) or require complete replacement. Replacement is often necessary if the panel is severely creased, torn, or if its structural integrity is compromised.

- Mechanical Damage: Impacts can affect a car's internal components. This might include damage to the suspension system (shock absorbers, springs, control arms), steering components, braking system, exhaust, or even the engine and transmission. Mechanical repairs often involve replacing complex parts and require specialised diagnostic tools and skilled labour.

- Structural Damage: This is the most serious and expensive type of damage, affecting the vehicle's chassis or frame. The chassis is the car's foundational structure, and damage here compromises its safety and ability to absorb future impacts. Repairing structural damage often requires specialist equipment (like a jig for chassis straightening) and highly skilled technicians, making it incredibly costly and often leading to a 'write-off' classification.

2. Vehicle Make, Model, and Age

The type of car you drive has a direct impact on repair costs. Luxury vehicles, sports cars, and those with advanced technology (e.g., adaptive cruise control sensors, LED matrix headlights) tend to be more expensive to repair. This is due to:

- Part Costs: Parts for premium brands are often more expensive than those for mass-market cars. Specialist components, lightweight materials (like aluminium or carbon fibre), and complex electronic modules drive up prices.

- Labour Rates: Some high-end vehicles require specialist tools and training for repairs, meaning main dealerships or specialist garages might charge higher labour rates.

- Complexity: Modern cars are increasingly complex, with integrated systems. A seemingly minor bump might trigger multiple sensor warnings or require recalibration of advanced driver-assistance systems (ADAS), adding to the diagnostic and repair time.

3. Type of Parts Used

When a part needs replacing, garages typically have a few options, each with different cost implications:

- Original Equipment Manufacturer (OEM) Parts: These are identical to the parts your car was built with, supplied by the car manufacturer. They guarantee a perfect fit and quality but are generally the most expensive option. Insurers often prefer OEM parts for newer vehicles or safety-critical components.

- Aftermarket Parts: Produced by third-party manufacturers, these parts are designed to fit and function like OEM parts but are often considerably cheaper. Quality can vary, so it's important to use reputable aftermarket suppliers.

- Used/Salvage Parts: These are parts salvaged from other vehicles, often from breakers' yards. They are the cheapest option and can be suitable for non-critical components or older vehicles, but their condition can vary, and they might not come with a warranty.

4. Labour Rates and Location

The hourly rate charged by garages can differ significantly. Main dealerships generally have the highest labour rates, followed by independent garages, and then smaller local mechanics. These rates also vary depending on your geographical location within the UK, with garages in London and the South East typically charging more than those in other regions.

5. Paintwork and Finishing

Even a small repair often requires paintwork to seamlessly blend the repaired area with the rest of the car. This involves meticulous colour matching, priming, painting, and lacquering. Complex metallic or pearlescent paints can be more difficult and time-consuming to match, increasing costs. Multiple panels needing paintwork due to blending requirements will also escalate the price.

One of the most frustrating aspects of accident repair costs is the potential for hidden damage. What appears to be a minor dent on the surface might conceal underlying structural or mechanical issues. For example, a seemingly small front-end impact could have bent a radiator support, damaged a headlight mounting, or even cracked an engine mount. Garages often provide an initial estimate based on visible damage, but the final bill can increase once the vehicle is dismantled and further issues are discovered. This is why it's crucial to get a thorough assessment.

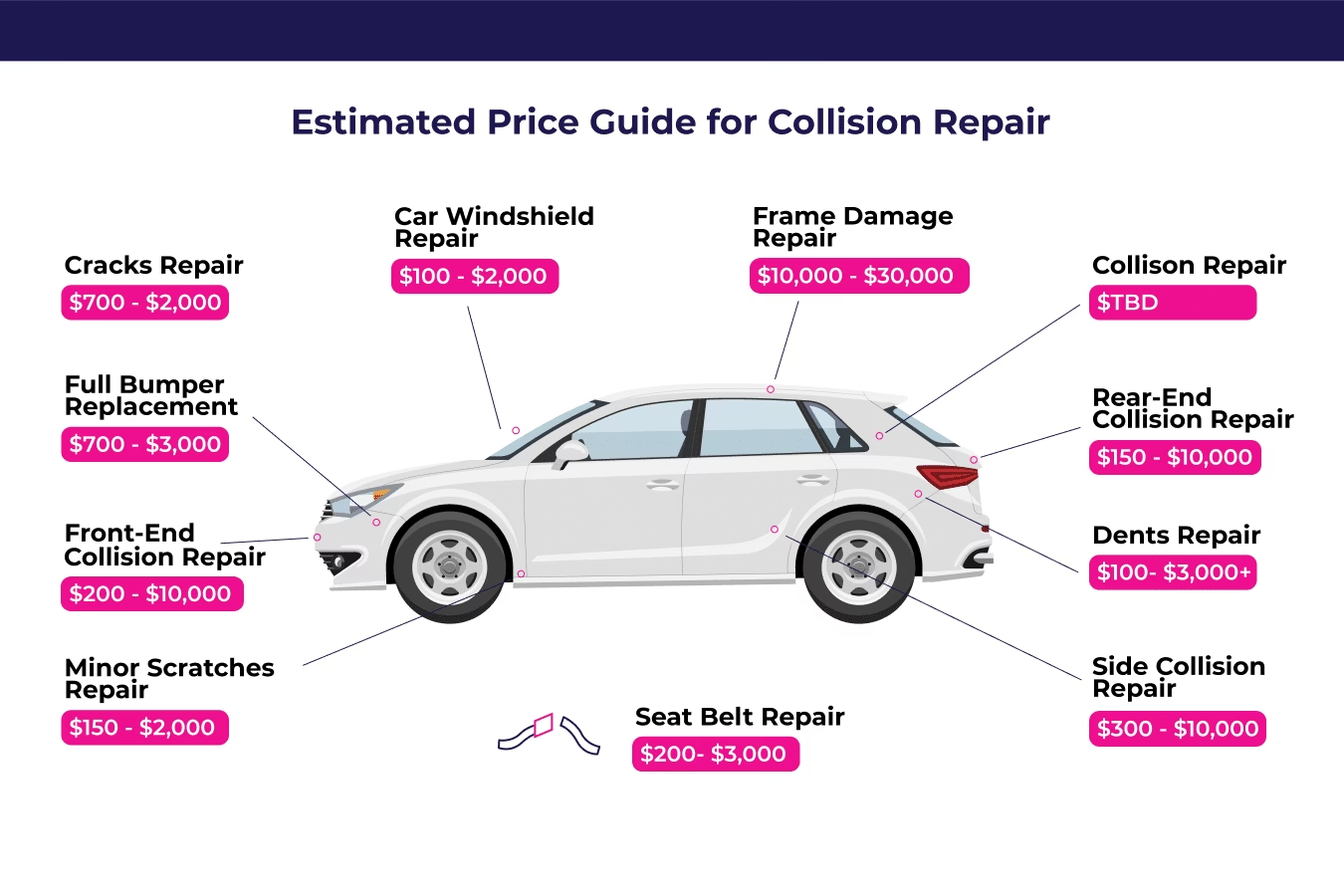

Estimated Costs for Common Car Accident Repairs (UK)

Here's a general guide to what you might expect to pay for various types of repairs. Please remember these are broad estimates and can vary significantly.

Minor Cosmetic Repairs

- Scratches and Scuffs: For minor surface scratches that don't penetrate the paint, a smart repair (small to medium area repair technique) can cost anywhere from £100 to £350 per panel. Deeper scratches requiring filling and full panel respray could be £250 to £500+.

- Small Dents (Paintless Dent Removal - PDR): If the paintwork is intact, PDR can remove small dents for £50 to £200 per dent, depending on size and location.

Bodywork Repairs

- Bumper Repair/Replacement: A plastic bumper repair (e.g., crack, scuff) might cost £200 to £600, including paint. A full bumper replacement, including the cost of a new bumper (OEM or aftermarket) and painting, could range from £400 to £1,500+, especially for modern bumpers with sensors or complex designs.

- Wing/Fender Repair/Replacement: Repairing a damaged wing could be £300 to £800. If replacement is necessary, including the new panel and paint, expect £500 to £1,500+.

- Door Panel Repair/Replacement: Similar to wings, door repairs can range from £400 to £1,200. Replacement, which often involves transferring internal components (windows, wiring), can be £800 to £2,000+.

- Bonnet/Boot Lid Repair/Replacement: These larger panels can cost £500 to £1,500 for repair or £800 to £2,500+ for replacement, especially if they include complex mechanisms or integrated lighting.

Glass and Lighting

- Windscreen Replacement: Often covered by insurance with a lower excess, but out-of-pocket costs can be £150 to £600, more if it includes rain sensors or heating elements.

- Headlight/Taillight Replacement: A single unit can range from £100 to £500 for standard halogen lights, but modern LED or Xenon units can easily be £500 to £1,500+ each due to integrated electronics.

Mechanical and Structural Repairs

- Suspension Damage: Repairing a bent wishbone or damaged shock absorber could be £200 to £800 per corner. More extensive damage involving multiple components or an axle could be £800 to £3,000+.

- Radiator/Cooling System Damage: Replacing a radiator, condenser, or associated pipework could cost £300 to £1,000+ depending on the vehicle and complexity.

- Engine/Transmission Damage: This is where costs escalate dramatically. If an impact has damaged the engine block, gearbox casing, or internal components, repairs can run into several thousands of pounds, often making the car an economic write-off. Expect £1,500 to £5,000+, potentially much more.

- Chassis/Structural Damage: Repairing a bent chassis or significant structural components is the most expensive type of repair. Costs can easily exceed £2,000 to £10,000+, leading to a write-off in most cases unless it's a very high-value vehicle.

Comparative Cost Table (Estimated Ranges)

| Repair Type | Estimated Cost Range (GBP) | Notes |

|---|---|---|

| Minor Scratches/Scuffs | £100 - £350 | Smart repair, single panel |

| Small Dents (PDR) | £50 - £200 | Paintwork intact |

| Bumper Repair (plastic) | £200 - £600 | Includes paintwork |

| Bumper Replacement | £400 - £1,500+ | Includes new part & paint |

| Wing/Fender Repair | £300 - £800 | Includes paintwork |

| Wing/Fender Replacement | £500 - £1,500+ | Includes new part & paint |

| Door Panel Repair | £400 - £1,200 | Includes paintwork |

| Door Panel Replacement | £800 - £2,000+ | Includes new part & paint, internal transfers |

| Windscreen Replacement | £150 - £600 | More for sensors/heating |

| Headlight Replacement (single) | £100 - £500 | Standard halogen |

| Headlight Replacement (single, advanced) | £500 - £1,500+ | LED, Xenon, matrix lights |

| Suspension Component (e.g., wishbone) | £200 - £800 | Per component, includes labour |

| Extensive Suspension Damage | £800 - £3,000+ | Multiple components, axle damage |

| Radiator Replacement | £300 - £1,000+ | Depends on vehicle & part cost |

| Engine/Transmission Damage | £1,500 - £5,000+ | Often leads to write-off |

| Chassis/Structural Damage | £2,000 - £10,000+ | Highly variable, very often a write-off |

Insurance Claim vs. Paying Out-of-Pocket

Once you have an idea of the repair costs, the next big decision is whether to claim through your insurance or pay for the repairs yourself. This decision hinges primarily on your insurance excess and the potential impact on your no-claims bonus (NCB).

- Insurance Excess: This is the amount you agree to pay towards any claim before your insurer pays the rest. If your excess is £500 and the repair cost is £400, it makes no sense to claim, as you'd pay the full amount anyway.

- No-Claims Bonus (NCB): Your NCB is a discount on your premium for each year you don't make a claim. Making a claim, even for a minor incident, can reduce your NCB, leading to higher premiums in subsequent years. Some insurers offer NCB protection, but this typically comes at an additional cost and might still affect future premiums to some extent.

As a general rule of thumb, if the repair cost is significantly less than your excess plus the potential loss of your NCB over a few years, it's often more economical to pay out-of-pocket. For major repairs, especially those involving significant mechanical or structural damage, claiming on your insurance is almost always the more sensible option. Always get a repair estimate before deciding.

Getting a Repair Estimate

After an accident, it's highly recommended to obtain multiple quotes for the repair work. Don't just go with the first garage you find or the one recommended by your insurer without checking. Different garages will have varying labour rates, and their preferred suppliers for parts might also differ. A comprehensive estimate should clearly itemise:

- Parts costs (specifying OEM, aftermarket, or used)

- Labour hours and hourly rate

- Paint and materials costs

- VAT

Be wary of estimates that seem too good to be true, as they might be missing crucial steps or using inferior parts. Conversely, don't automatically assume the most expensive quote is the best; ensure it's justified by the quality of parts, expertise, and warranty offered.

When is a Car a 'Write-Off'?

A car is declared a 'write-off' (or 'total loss') by an insurance company when the cost of repairing the damage exceeds a certain percentage of the vehicle's market value. This threshold varies between insurers, but it's typically around 50-70%. If your car is written off, your insurer will pay you its market value (less your excess) rather than covering the repair costs.

In the UK, written-off vehicles are categorised:

- Category S (Structural): The vehicle has sustained structural damage. It can be repaired and returned to the road, but it must pass a new MOT and be re-registered with the DVLA.

- Category N (Non-Structural): The vehicle has sustained non-structural damage (e.g., body panel damage, electrical issues). It can be repaired and returned to the road without requiring a re-registration, though an MOT is still necessary if due.

It's important to understand that a car can be a write-off even if it looks like it could be repaired, simply because the cost of repair outweighs its current value.

Tips for Managing Repair Costs

- Get Multiple Quotes: As mentioned, this is paramount. Compare itemised breakdowns.

- Consider Independent Garages: While main dealerships offer manufacturer-specific expertise, independent garages often have lower labour rates and can provide excellent quality work, sometimes specialising in certain makes or types of repair.

- Discuss Part Options: Ask your chosen garage about the possibility of using high-quality aftermarket or even used parts for non-critical components to save money.

- Be Clear on Warranty: Ensure the repair work comes with a warranty on both parts and labour.

- Don't Rush: Unless your car is unsafe to drive, take your time to get thorough assessments and compare options.

- DIY for Minor Scuffs: For very minor cosmetic damage, a DIY repair kit or touch-up paint might save you a small fortune, but ensure you have the skills and tools to do it properly.

Frequently Asked Questions (FAQs)

A1: In most cases, yes. Making a claim, even if you're not at fault, can lead to an increase in your premium at renewal time due to the loss of your no-claims bonus or simply because you're now deemed a higher risk. Always weigh the cost of repair against the potential long-term increase in your premiums.

Q2: How long do car accident repairs typically take?

A2: The duration varies greatly depending on the extent of the damage and the availability of parts. Minor cosmetic repairs might take a day or two. Panel replacements could take a few days to a week. More extensive mechanical or structural repairs could take several weeks, especially if specialist parts need ordering or complex chassis work is involved. Your garage should be able to give you an estimated timeframe.

Q3: Should I use an approved repairer recommended by my insurer?

A3: Insurers often have a network of approved repairers, and using them can streamline the process, as the insurer has pre-negotiated rates and trusts their quality. However, you are usually not obligated to use their chosen garage. You have the right to choose your own repairer. Just ensure your chosen garage is reputable and provides a detailed quote that your insurer will accept.

A4: This is a common occurrence. If hidden damage is discovered during the repair process, the garage should immediately contact you (and your insurer if a claim is active) to inform you of the additional work required and the revised cost. They should not proceed with the extra work without your authorisation. This is why a thorough initial inspection is crucial.

Q5: Is it safe to drive a car after an accident if it looks okay?

A5: It is generally not advisable to drive a car after an accident, even if the damage appears minor. There could be unseen structural damage, issues with steering, brakes, or suspension, or even deployed airbags that make the vehicle unsafe. Always get the car inspected by a qualified mechanic before driving it, or arrange for recovery.

Navigating car accident repairs can be daunting, but by understanding the factors at play, getting multiple quotes, and carefully considering your insurance options, you can make the process smoother and ensure your vehicle is safely and cost-effectively returned to its pre-accident condition.

If you want to read more articles similar to Car Accident Repair Costs: A UK Guide, you can visit the Repairs category.