30/05/2022

In the intricate world of automotive engineering, brake pads stand as unsung heroes, silently ensuring our safety on every journey. These critical components, housed within a vehicle's disc brake system, are fundamental to its ability to stop, converting kinetic energy into thermal energy through friction. When the brake pedal is engaged, the brake pads press against the spinning disc, bringing the vehicle to a controlled halt or reducing its speed. Their importance cannot be overstated, directly impacting vehicle control, stability, and overall road safety. The global automotive brake pad market has been experiencing robust growth, valued at an impressive $3.8 billion in 2021 and projected to reach $6.5 billion by 2031, demonstrating a compound annual growth rate (CAGR) of 5.6% from 2022 to 2031. This significant expansion is driven by a confluence of factors, from heightened safety awareness and stringent regulations to technological advancements and evolving consumer demands.

Understanding the Market's Upward Trajectory

The consistent growth observed in the automotive brake pad market is not merely incidental but a direct consequence of several powerful trends and strategic developments across the global automotive landscape. These drivers collectively reinforce the demand for more advanced, durable, and environmentally conscious braking solutions.

Enhanced Safety Awareness and Regulatory Standards

One of the primary catalysts for market expansion is the escalating focus on automotive safety, both from consumers and governmental bodies. As vehicle owners become more attuned to the importance of active and passive safety features, demand for sophisticated braking systems naturally increases. This consumer awareness is strongly complemented by stringent government regulations worldwide. Technologies such as Anti-lock Braking Systems (ABS) and autonomous braking systems, once considered luxury features, are now becoming standard equipment in most new vehicles. These systems inherently demand high-performance brake pads to function optimally, thereby accelerating market growth.

Governments across the globe are proactively establishing and enforcing regulations aimed at improving vehicle safety. For instance, in the U.S., the Department of Transportation's National Highway Traffic Safety Administration (NHTSA), in collaboration with the Insurance Institute for Highway Safety and 20 leading vehicle manufacturers, announced that automatic emergency braking (AEB) systems would be a standard feature in all new cars from September 2022. Similarly, the Government of India mandated ABS for two-wheelers above 125 cc and a combined-braking system (CBS) for those below 125 cc, effective from April 2019. Such mandates necessitate the integration of advanced braking components, including high-quality brake pads, into a wide range of vehicles. Furthermore, global initiatives like the NCAP (New Car Assessment Programme) road map for safer vehicles advocate for safety regulations covering electronic stability control, pedestrian protection, and emergency brake systems. These programmes propose that such regulations be applied to new models and eventually to all vehicles in production, driving manufacturers to develop advanced braking pads that meet these rigorous standards.

The Rise of Eco-Friendly and Sustainable Brake Pads

A significant shift in the market is the increasing demand for eco-friendly and sustainable brake pads. Historically, asbestos was a common raw material in brake pad manufacturing due to its heat resistance and friction properties. However, its harmful health effects have led to a global movement away from its use. This has spurred a surge in demand for natural alternatives such as coconut fibre, wood or wheat flour, bamboo fibre, and shell powder. These natural fibres offer numerous advantages over synthetic ones, including lower density, abundance, lower cost, recyclability, biodegradability, and relatively high strength and stiffness. The environmental awareness is not just consumer-driven; regulations are also playing a crucial role. For example, in the U.S., regulations have prohibited the sale and use of friction material products with a copper content of 5% or more since 2021, with further tightening to 0.5% by 2025. This has prompted manufacturers like Nisshinbo Brake to develop low-copper or copper-free friction materials, ensuring their products meet or exceed these environmental parameters. The benefits of eco-friendly brake pads, such as their lower cost and lighter weight, are expected to significantly drive their adoption in both current and future vehicle models.

Increased Traffic Congestion and Aftermarket Demand

The burgeoning global population and urbanisation have led to a substantial increase in traffic congestion, particularly in metropolitan areas. More stop-and-go driving conditions directly translate to increased wear and tear on vehicle braking systems, especially brake pads. As original equipment manufacturer (OEM) pads reach the end of their service life, they are replaced by aftermarket (AM) brake pads. This replacement market is a significant contributor to the overall growth of the automotive brake pad industry. Auto dealers, independent repair shops, and quick-fit centres are continuously installing aftermarket brake pads, ensuring a steady and growing revenue stream for manufacturers.

Strategic Expansions and Manufacturing Hubs

The Asia-Pacific region has emerged as a powerhouse in the automotive industry, becoming a manufacturing hub due to the availability of low-cost labour and raw materials. Countries like China, India, and Japan are at the forefront of this growth, attracting significant investments from global automotive players. Manufacturers are strategically expanding their presence in these regions by establishing new headquarters or manufacturing plants. For instance, Porsche expanded its operations in Asia with a research and development centre in Shanghai, China, and a production site in Malaysia. Such expansions directly fuel the demand for automotive components, including brake pads. Furthermore, strategic agreements and joint ventures, such as Brembo's partnership with a China-based company for an aftermarket brake pad manufacturing facility, or Gold Phoenix Group's contract to supply brake pads for Daimler’s Mercedes-Benz Vito models, exemplify the region's increasing importance and contribution to market growth.

The Advent of Smart Brake Pads

Innovation continues to push the boundaries of brake pad technology with the development of 'smart pads'. Recognising that many accidents are caused by late braking or driver negligence, manufacturers are exploring brake pads equipped with advanced sensors. These sensors, often based on relay circuits and integrated with traditional braking systems, can provide real-time data on temperature, pressure distribution, torque, residual torque, vibration, noise, and wear. This dynamic data collection transforms a passive component into an active safety system. GALT, an ITT startup, launched unique embedded and connected sensor brake pads designed to improve driving safety and efficiency by providing high-precision measurements and improved close-range detection. These smart pads represent a significant step towards the future of mobility, offering enhanced safety, efficiency, and connectivity, even in the harsh environments to which brake pads are typically exposed.

Segmentation of the Automotive Brake Pad Market

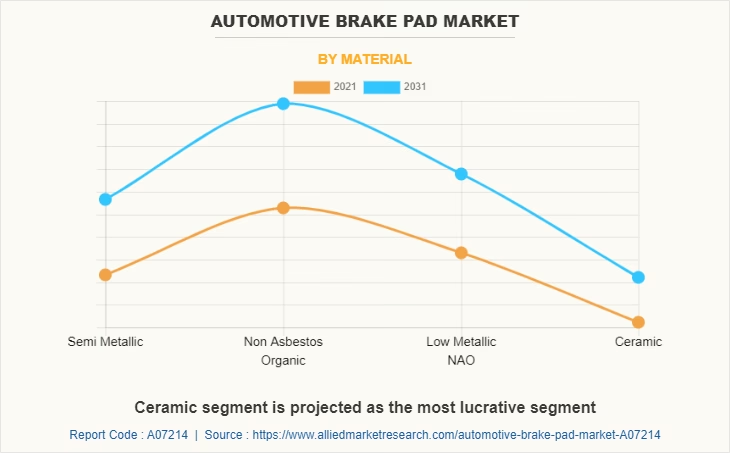

To fully comprehend the dynamics of this evolving market, it is essential to look at its various segments. The automotive brake pad market is broadly categorised based on material, position, vehicle type, and sales channel, providing a granular view of its structure and opportunities.

Market Segmentation Overview

| Category | Key Segments |

|---|---|

| Material | Semi-Metallic, Non-Asbestos Organic (NAO), Low Metallic NAO, Ceramic |

| Position | Front, Front & Rear |

| Vehicle Type | Two-Wheelers, Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles |

| Sales Channel | OEM (Original Equipment Manufacturer), Aftermarket |

| Region | North America, Europe, Asia-Pacific, LAMEA (Latin America, Middle East, Africa) |

By material, the market's traditional reliance on semi-metallic and non-asbestos organic (NAO) pads is evolving with the increasing prominence of low metallic NAO and ceramic options, driven by performance and environmental considerations. Positionally, both front-only and front & rear brake pad configurations are crucial, reflecting the diverse braking requirements of different vehicle types. Passenger cars continue to be the leading application segment, although demand from two-wheelers, light commercial vehicles (LCVs), and heavy commercial vehicles (HCVs) is also significant. The market is effectively split between OEM sales, where manufacturers supply directly to vehicle assemblers, and the robust aftermarket, which caters to replacement needs throughout a vehicle's life cycle.

Challenges in the Market Landscape

Despite the overall positive growth trajectory, the automotive brake pad market faces certain challenges that could impede its expansion. The most notable hurdle is the high development cost associated with advanced brake pad materials and technologies. Innovating with materials like ceramics or advanced steels requires substantial capital expenditure for research, development, and commercialisation. This high initial investment often means that only a few major automotive companies can undertake such ventures, limiting broader market access to cutting-edge solutions. While advanced electronic braking systems offer superior braking distance and enhanced stability, their associated costs, including that of their specialised brake pads, can be prohibitive for economy-class vehicles, creating a demand for high-performance raw materials at stable and lower costs. Striking a balance between innovation, performance, and affordability remains a key challenge for manufacturers.

Leading Market Players and Recent Innovations

The competitive landscape of the automotive brake pad market is dominated by several key players who are continually investing in research and development to enhance product performance, durability, and environmental compliance. Prominent companies include Akebono Brake Industry Co Ltd., ADVICS, Brake Parts Inc., Brembo S.p.A., Continental AG, Delphi Technologies Inc. (BorgWarner Inc.), EBC Brake, ITT Inc., Nisshinbo Brake Inc., Robert Bosch GmbH, Tenneco Inc., and ZF Friedrichshafen AG. These industry leaders are adopting various strategies, such as product launches and strategic partnerships, to strengthen their market position.

Recent developments highlight this commitment to innovation. In April 2022, Brembo introduced its new Aftermarket line of brake pads specifically for heavy-duty vehicles, alongside new Co-Cast and Splined disc solutions. Similarly, in February 2021, First Brands Group expanded its Raybestos brake components line by adding over 200 part numbers, including increased coverage for luxury vehicle applications. In a move towards sustainability and specialised vehicle needs, Bendix, an Australian braking systems manufacturer, unveiled its 'EV Hybrid' brake pads in July 2021. These pads utilise ceramic technology and are made from organic materials, specifically designed to meet the unique braking requirements of electric vehicles while minimising environmental impact. Such initiatives underscore the industry's drive to meet the evolving demands of consumers and stringent regulatory standards.

Frequently Asked Questions (FAQs)

To provide further clarity on the automotive brake pad market, here are answers to some commonly asked questions:

Q1. What is the estimated industry size of the automotive brake pad market?

A1. The global automotive brake pad market was valued at $3.83 billion in 2021 and is projected to reach $6.51 billion by 2031, registering a CAGR of 5.6%.

Q2. Which are the top companies holding market share in automotive brake pads?

A2. Some major companies operating in the market include Akebono Brake Industry Co Ltd., ADVICS, Brake Parts Inc., Brembo S.p.A., Continental AG, Delphi Technologies Inc. (BorgWarner Inc.), EBC Brake, ITT Inc., Nisshinbo Brake Inc., Robert Bosch GmbH, Tenneco Inc., and ZF Friedrichshafen AG.

Q3. Which is the largest regional market for automotive brake pads?

A3. Asia-Pacific is currently the largest regional market for automotive brake pads.

Q4. What is the leading application of the automotive brake pad market?

A4. Passenger Cars represent the leading application segment within the automotive brake pad market.

Q5. What are the upcoming trends in the automotive brake pad market globally?

A5. Key upcoming trends include an increasing demand for eco-friendly and sustainable brake pads, along with the continued development of smart pads featuring integrated sensors and advanced functionalities.

Conclusion

The automotive brake pad market is on a clear path of significant growth, propelled by an increasing emphasis on vehicle safety, the relentless pursuit of technological innovation, and a growing global awareness of environmental sustainability. From the widespread adoption of advanced braking systems like ABS and AEB to the development of eco-friendly materials and the emergence of 'smart' brake pads, the industry is adapting to meet complex demands. While challenges such as high development costs persist, the long-term outlook remains positive. With continuous investment in research and development, strategic expansions in key growth regions like Asia-Pacific, and a commitment to meeting increasingly stringent regulations, the automotive brake pad market is set to play an even more crucial role in ensuring safer, more efficient, and environmentally responsible mobility for the years to come.

If you want to read more articles similar to The Surging Automotive Brake Pad Market: A Deep Dive, you can visit the Automotive category.