19/11/2001

The question of whether a written-off car can be fixed is a common one, particularly when a vehicle is still under a finance agreement. If your car is declared a write-off while you still owe money on it, the situation can feel overwhelming. Typically, the insurance payout will be used to settle the outstanding balance on your finance agreement. However, it's crucial to understand that this payout might not always be enough to cover the full amount owed, leaving you responsible for any remaining shortfall. Conversely, if the insurance payout exceeds the outstanding balance, you'll receive the excess amount. Navigating this process smoothly and avoiding unexpected financial challenges requires a thorough understanding of your insurance and finance agreements. Let’s delve deeper into the intricacies of dealing with a written-off car in the UK.

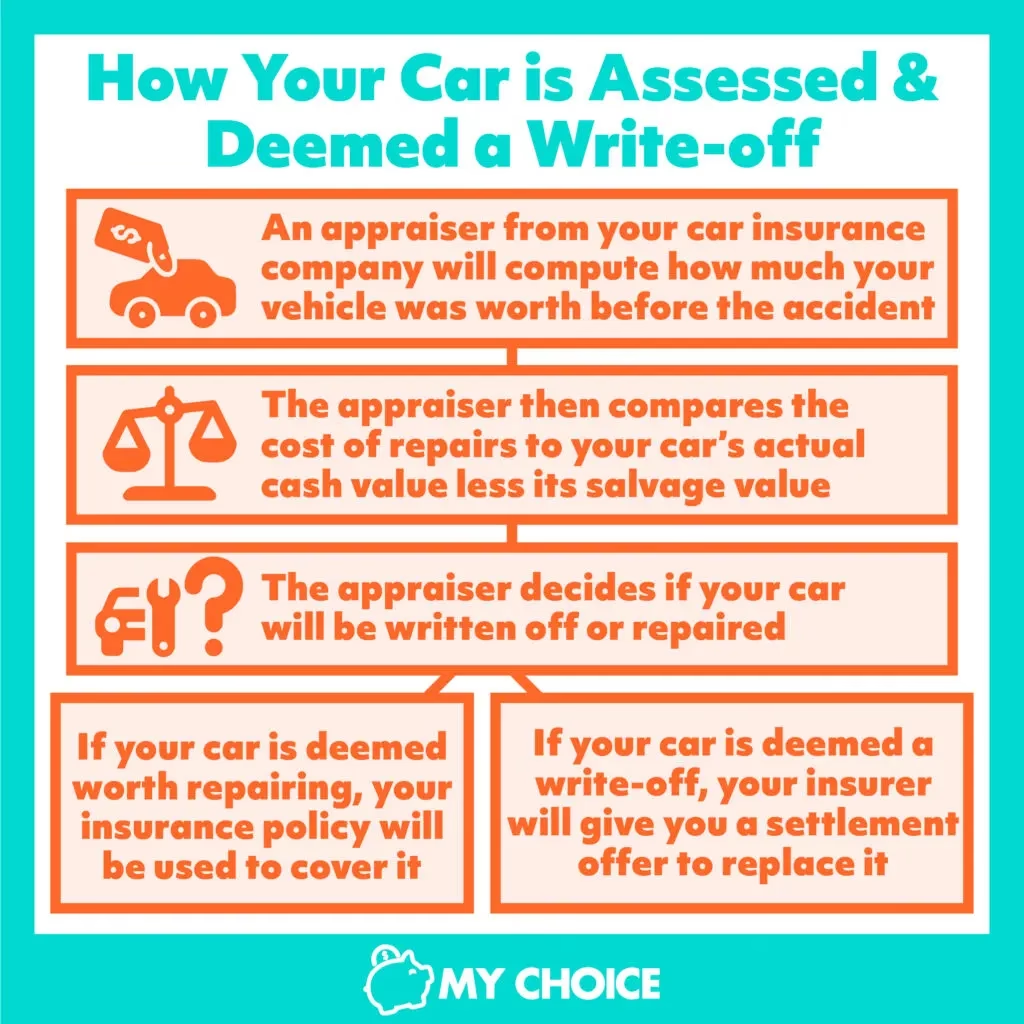

Understanding the different types of insurance write-off categories is the first step in comprehending the implications for your vehicle. When your car is declared a write-off, it falls into one of four distinct categories, each with specific rules and consequences, especially for a financed vehicle.

The Different Types of Insurance Write-Off Categories

In the UK, if your car has been declared a write-off, it will be assigned one of four categories: A, B, S, or N. These categories signify the extent of the damage and whether the vehicle can ever return to the road. The implications for your financed vehicle vary significantly depending on which category it falls into.

Categories A to N and Their Implications for Your Financed Vehicle

Each category has precise implications regarding repairability, salvageability, and most importantly, how the insurance payout interacts with your finance agreement:

- Category A: Scrap Only. This category applies to vehicles that have sustained severe damage, rendering them completely unsalvageable. The vehicle must be crushed entirely, and no parts can be salvaged or sold. For a financed car, the insurance payout will be directed towards settling your finance balance, as the car cannot be repaired or resold. This is the most definitive form of write-off, meaning the car is gone for good.

- Category B: Break for Parts. Similar to Category A, a Category B vehicle cannot return to the road. However, unlike Category A, some parts can be salvaged and sold for reuse. The vehicle structure itself is deemed irreparable and must be crushed. Again, the insurance payout will be used to settle your finance agreement, as the car is permanently off the road.

- Category S: Structurally Damaged but Repairable. A vehicle in Category S has sustained structural damage. While this type of damage is significant, the car is deemed repairable. If you choose to repair the car, you may be able to keep it, but you will still be responsible for settling the outstanding finance. If you decide not to repair, the insurance payout will help cover the finance. It’s crucial to ensure any repairs are carried out by qualified professionals and the car passes a Vehicle Identity Check (VIC) if required, although the VIC test was abolished in October 2015. However, the car still needs to be re-registered with the DVLA after repairs if it was previously marked as Cat S.

- Category N: Non-Structurally Damaged but Repairable. This category applies to vehicles with non-structural damage, such as problems with the electrics, interior, or body panels that don’t affect the structural integrity. Like Category S, the car is deemed repairable. You have the option to repair and keep the car, or you can use the insurance payout to address the finances. Category N damage is generally less severe than Category S, making repairs often more straightforward and cost-effective.

Understanding these categories is vital for managing the aftermath of a write-off, especially when finance is involved. Your options and responsibilities will largely depend on which category your vehicle falls into.

Summary of Write-Off Categories

| Category | Damage Type | Repairable? | Can it return to road? | Finance Implications |

|---|---|---|---|---|

| A | Severe structural | No | No | Insurance payout settles finance; vehicle scrapped. |

| B | Severe structural | No | No | Insurance payout settles finance; vehicle scrapped, parts salvaged. |

| S | Structural | Yes | Yes (after repair) | You can repair and keep (settle finance), or use payout for finance. |

| N | Non-structural | Yes | Yes (after repair) | You can repair and keep (settle finance), or use payout for finance. |

Immediate Steps Following a Write-Off Declaration

When your car is declared a write-off, time is of the essence. Taking immediate and correct steps can significantly ease the process and prevent further financial complications. There are three critical parties you need to contact promptly: your finance provider, your insurance company, and the DVLA.

Contact Your Finance Provider Promptly

Your first and most crucial step is to contact your finance provider without delay. Informing them promptly ensures they are aware of the situation and can guide you through the necessary procedures. They will typically work directly with your insurance company to ascertain the remaining finance balance and how the insurance payout will be applied. Failing to notify your finance provider could lead to serious complications, such as continuing to make monthly payments for a vehicle you no longer possess, or even incurring late payment charges if the situation isn't formally acknowledged.

Speak to Your Insurance Company to Ensure Proper Coverage

Next, contact your insurance company to report the write-off. Provide them with all necessary details and documentation, including the date of the incident, police report (if applicable), and any other relevant information. Your insurer will then assess the damage, determine the write-off category, and calculate the payout amount based on your policy terms and the vehicle’s market value. Ensuring proper and clear communication with your insurer is paramount for an accurate and swift settlement of your claim and, subsequently, your finance balance. It’s also the time to discuss any potential gaps between the insurance payout and your outstanding finance balance, as you might be responsible for covering any shortfall if you don’t have additional protection like GAP insurance.

The Importance of Notifying the DVLA

Finally, it is absolutely essential to notify the DVLA (Driver and Vehicle Licensing Agency) about the write-off. This step is crucial for updating your vehicle’s status in their records. Neglecting to do so could lead to legal issues, as the car might still be mistakenly recorded as being on the road. You must send your V5C logbook (registration document) to the DVLA, clearly indicating that the car has been written off. The exact section to complete will depend on the write-off category. Keeping copies of all documentation for your records is highly recommended. This ensures all parties are correctly informed, maintaining legal compliance and clarity regarding your vehicle’s status.

Why GAP Insurance Is a Good Idea for Cars on Finance

When your car is on finance, a write-off can leave you in a precarious financial position. This is where GAP (Guaranteed Asset Protection) insurance becomes incredibly valuable. It’s a worthwhile investment that can protect you from significant financial loss.

How GAP Insurance Works When Your Financed Car Is Written Off

The core purpose of GAP insurance is to cover the financial gap that often arises between the amount your primary car insurance company pays out for a total loss and the remaining balance on your finance agreement. Here's a detailed breakdown of how it operates:

- Primary Insurance Payout: When your vehicle is declared a write-off, your standard car insurance policy will provide a payout based on the vehicle’s current market value at the time of the incident. Unfortunately, cars depreciate rapidly, meaning their market value can fall significantly below the original purchase price or, more critically, the outstanding finance balance.

- Outstanding Finance: The finance balance is the total amount you still owe on your car loan. Due to the rapid depreciation of vehicles, it's very common for the insurance payout to be less than what you still owe to your finance provider. This creates a 'gap' or shortfall, leaving you out of pocket and still liable for the remaining debt.

- GAP Insurance Coverage: This is where GAP insurance steps in. It is designed specifically to bridge this financial gap. It pays the difference between your car's market value (as determined by your primary insurer) and the remaining finance balance. This ensures that you are not left with a debt to your finance provider for a car you no longer own.

Without GAP insurance, you would be personally responsible for covering this shortfall, which could amount to thousands of pounds, even after receiving your primary insurance payout.

Types of GAP Insurance

There are several types of GAP insurance available, each offering slightly different coverage:

- Finance GAP Insurance: This is the most common type and directly covers the difference between your primary insurance payout and the outstanding balance on your finance agreement. It ensures your loan is fully cleared.

- Return to Invoice (RTI) GAP Insurance: This type of policy covers the difference between your primary insurance payout and the car’s original invoice price. This is particularly beneficial if you want to be in a position to purchase a similar new vehicle without incurring a loss from depreciation.

- Vehicle Replacement GAP Insurance: This policy aims to cover the cost of replacing your written-off vehicle with a new one of the same make, model, and specification, even if the price of the new car has increased since your original purchase. It's the most comprehensive form of GAP cover.

Considering the significant depreciation of modern vehicles and the potential for a shortfall, particularly for cars on finance, GAP insurance offers invaluable peace of mind and robust financial protection.

Next Steps and Possible Outcomes for Financed Cars That Are Written Off

Once your car has been declared a write-off, and the immediate notifications have been made, you'll need to consider your next steps. The outcomes largely depend on the write-off category and your personal financial situation.

Clearing the Outstanding Finance Balance

As discussed, the primary insurance payout for your written-off vehicle will typically go directly towards clearing the outstanding finance balance. If there is a shortfall – meaning the payout is less than what you owe – you will be responsible for covering this difference. It is crucial to contact your finance provider immediately to discuss your options. They may be able to offer solutions such as extending the loan term for the remaining balance or adjusting payment plans to make it more manageable. Prompt communication can prevent late payment fees and damage to your credit rating.

Buying Back and Repairing Your Car

If your car is classified as Category S or Category N, you may have the option to repurchase it from the insurer and undertake the necessary repairs. This can be an attractive option, especially if the damage is relatively minor or if the car holds significant sentimental value. However, before committing to this, it's vital to meticulously assess whether it’s truly worthwhile. Consider the following factors:

- Repair Costs: Obtain multiple detailed repair quotes from reputable mechanics. Compare these costs against the insurance payout you would receive if you didn't buy the car back. Remember that these repairs must restore the car to a roadworthy and safe condition.

- Post-Repair Value: Even after repairs, a car that has been a write-off (especially Category S) will have a diminished resale value. Factor this into your decision. Will the repaired car be worth enough to justify the repair expense and the effort?

- Safety: Ensuring the car's safety after repairs is paramount. Structural damage (Category S) requires expert attention to ensure the vehicle's integrity is fully restored. Always use certified mechanics who specialise in the type of repair needed.

- Insurance Implications: Be aware that insuring a previously written-off car can be more challenging and potentially more expensive. Some insurers may be reluctant to cover it, or they might charge higher premiums.

It's generally advisable to obtain an independent inspection of the damage before deciding to buy back a written-off vehicle to get an unbiased assessment of the repair feasibility and cost.

How to Upgrade or Replace Your Written-Off Vehicle

After a write-off, particularly once the financial obligations are cleared, you’ll likely need to consider upgrading or replacing your vehicle. This can be viewed as an opportunity to find a car that better suits your current needs and budget. Use any remaining insurance payout or excess funds as a down payment. When exploring new or used car options, remember to consider:

- Your Budget: Establish a clear budget for your new vehicle, including purchase price, insurance, running costs, and potential finance payments.

- Your Needs: Think about your daily driving habits, passenger requirements, and any specific features you desire, such as better fuel efficiency, advanced safety features, or increased cargo space.

- Financing Options: Research various financing options, including dealer finance offers, personal loans, and lease agreements. Compare interest rates, terms, and conditions to find the most suitable option for your financial situation.

Plan thoroughly and take your time to make an informed choice that fits your financial situation and lifestyle, ensuring a smooth transition back onto the road.

Frequently Asked Questions (FAQs)

What happens if my car is written off and it’s not my fault?

If your car is written off and the incident was not your fault, the at-fault driver’s insurance should cover the payout. This payout will be used to settle your finance agreement, and any excess amount that remains after the finance is cleared may be paid directly to you. Your own insurance no-claims bonus should not be affected in this scenario.

Can you fix a car that has been written off?

Yes, you can fix a written-off car if it has been classified as Category S (structurally damaged but repairable) or Category N (non-structurally damaged but repairable). It is crucial to thoroughly assess the repair costs and ensure that all repairs are carried out by certified and reputable mechanics to maintain roadworthiness and safety standards. Remember that the car's value may be affected in the long term.

How much does car insurance go up after a write-off?

After a write-off, it is highly likely that your car insurance premiums will increase, even if the incident wasn't your fault. The exact rise can vary significantly based on your insurer, your driving history, the specifics of the claim, and the write-off category. On average, premiums can see an increase of 20-50%, but this is merely an estimate and could be higher or lower depending on individual circumstances and the insurer's risk assessment. It's always advisable to shop around for new quotes after a write-off.

Is it time to sell your car?

If you're considering selling your car, whether due to a write-off situation or simply an upgrade, understanding the process is key. For more in-depth information on owning, maintaining, and selling your car, explore our other comprehensive guides. They cover everything from finding potential buyers and effectively negotiating a good price to ensuring payment is completed safely and securely, helping you navigate every step of your car ownership journey.

If you want to read more articles similar to Can You Fix a Written-Off Car in the UK?, you can visit the Insurance category.