29/10/2004

A car accident, even a minor one, can be a highly stressful experience. Beyond the immediate shock and inconvenience, the thought of getting your vehicle repaired and dealing with insurance claims can feel overwhelming. Understanding the car repair claim process in the UK is crucial to ensuring a smooth, efficient, and fair outcome. This guide aims to demystify the steps involved, from the moment an incident occurs to the completion of repairs, helping you navigate the complexities with confidence.

Immediate Steps After a Car Accident

Before you even think about insurance claims, your priority after an accident should always be safety and gathering essential information. What you do in the moments following a collision can significantly impact the ease and success of your subsequent claim.

- Ensure Safety: First, check for injuries to yourself and any passengers. If safe to do so, move your vehicle to a safe location, out of the flow of traffic. Turn on your hazard lights.

- Exchange Details: It is legally required to exchange contact and insurance details with any other parties involved. This includes names, addresses, phone numbers, vehicle registration numbers, and insurance policy details. If possible, note the make, model, and colour of their vehicle.

- Gather Evidence: Take photographs of the accident scene from various angles, including damage to all vehicles involved, road conditions, traffic signs, and any relevant landmarks. Note the date, time, and exact location of the incident. If there are witnesses, ask for their contact details. A dashcam can be invaluable here.

- Report to the Police: While not always necessary for minor collisions, you must report an accident to the police if anyone is injured, if the other party leaves the scene without exchanging details, or if there's significant damage or a suspected crime.

- Do Not Admit Fault: Even if you feel you were responsible, avoid admitting fault at the scene. This could prejudice your insurance claim. Stick to factual information.

Understanding Your Motor Insurance Policy

Before initiating a claim, it's vital to have a clear understanding of your own motor insurance policy. Different levels of cover offer varying degrees of protection for vehicle repairs.

- Third Party Only (TPO): This is the minimum legal requirement in the UK. It covers damage to other people's property (e.g., their car) and injuries to them, but it does not cover any damage to your own vehicle.

- Third Party, Fire and Theft (TPFT): This offers the same cover as TPO, plus protection if your vehicle is stolen or catches fire. Again, it does not cover damage to your own car from an accident you caused.

- Comprehensive Cover: This is the highest level of cover. It includes TPO, TPFT, and importantly, covers damage to your own vehicle, regardless of whether the accident was your fault or not. This is the policy type that will typically pay for your car's repairs after an accident.

An important term you'll encounter is your policy's excess. This is the fixed amount you agree to pay towards the cost of a claim before your insurer pays the rest. For instance, if your repairs cost £1,000 and your excess is £250, you pay £250 and your insurer pays £750. There might be a compulsory excess set by your insurer and a voluntary excess you chose to lower your premium. If the accident was not your fault and the other party's insurer pays for the repairs, you may be able to reclaim your excess.

Initiating Your Car Repair Claim

Once you've gathered all necessary information, the next step is to contact your insurance provider. It's generally advisable to do this as soon as possible, typically within 24-48 hours of the incident, even if you don't intend to claim.

- Contact Your Insurer: Call your insurer's claims line or use their online portal. Have all the information you collected at the scene ready.

- Provide Details: You'll need to give a detailed account of what happened, including the date, time, location, parties involved, and the extent of the damage. Be factual and honest.

- Fault vs. Non-Fault Claim: Your insurer will determine whether your claim is a fault claim or a non-fault claim. A fault claim means your insurer has to pay out for your damages and/or damages to the third party, and they cannot recover these costs from another party. This typically impacts your no-claims bonus and future premiums. A non-fault claim means your insurer can recover all costs from the at-fault party's insurer.

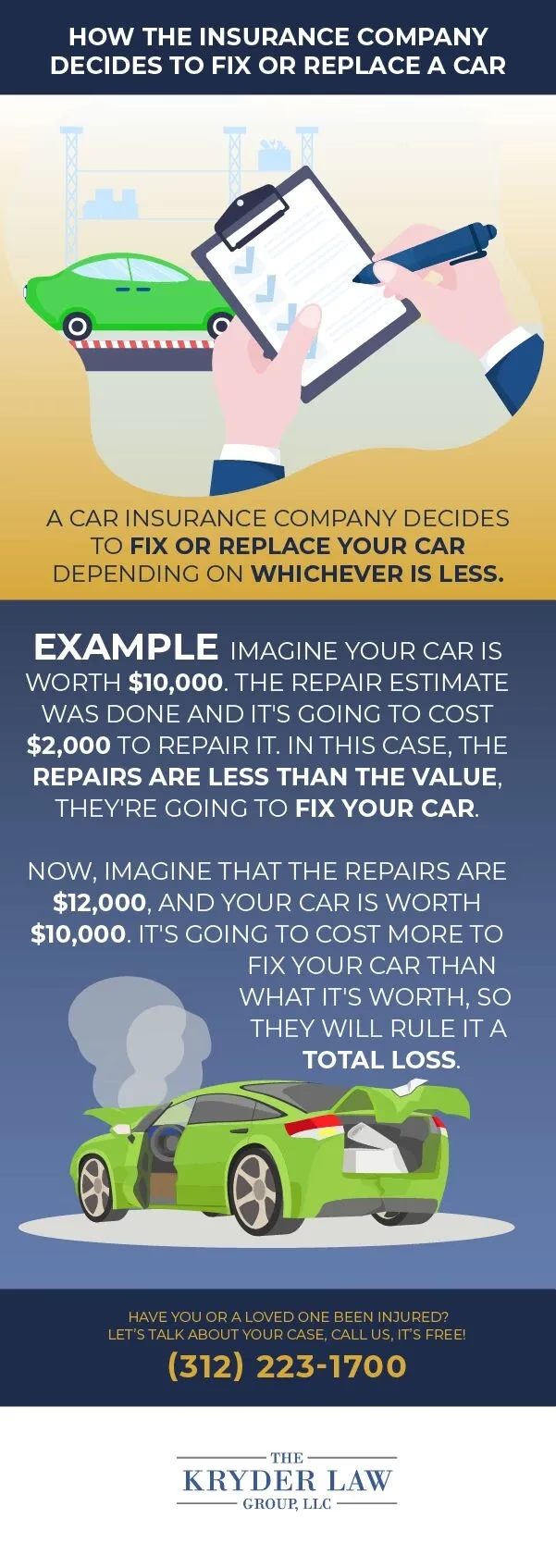

- Damage Assessment: Your insurer will likely arrange for an assessment of your vehicle's damage. This might involve you taking your car to an approved repair garage or an assessor coming to you. They will determine if the car is repairable or a 'write-off' (total loss).

Understanding the Damage Assessment Process

When your car undergoes damage assessment, an authorised assessor will inspect the vehicle to determine the extent of the damage and the cost of repairs. They will also consider if the car is economically viable to repair. If the cost of repairs exceeds a certain percentage of the car's market value (usually 50-70%, though this can vary), or if the damage is structural and compromises safety, the car may be declared a 'total loss' or 'written off'.

If your car is declared a total loss, your insurer will offer you a settlement based on its pre-accident market value. If you accept, the insurer takes ownership of the salvage. If you disagree with the valuation, you can challenge it with evidence of similar vehicles for sale.

The Repair Process: Getting Your Car Fixed

Once your claim is approved and the damage assessed, the repair process can begin. Your insurer will usually have a network of approved repairers.

- Approved Garages: Most insurers prefer you use their approved repairers. These garages have agreements with the insurer regarding pricing, quality standards, and often offer guarantees on their work. Using an approved garage can streamline the process, as the insurer deals directly with the garage for payment.

- Choosing Your Own Garage: You often have the right to choose your own repair garage, even if it's not on your insurer's approved list. However, if you opt for this, your insurer may require an independent assessment of the repair costs, and they might only pay up to the amount they would have paid their own network garage. You might also have to pay the garage directly and then claim reimbursement from your insurer.

- Repair Timeline: The time taken for repairs varies greatly depending on the extent of the damage, parts availability, and the garage's workload. Your insurer or the garage should keep you updated on the progress.

- Quality Control: Upon completion, inspect the repairs thoroughly before taking your car. Ensure all damage has been addressed and the quality of work is satisfactory. Most reputable garages and insurers offer a guarantee on repairs.

Table: Key Considerations for Fault vs. Non-Fault Claims

| Feature | Fault Claim | Non-Fault Claim |

|---|---|---|

| Impact on No-Claims Bonus | Likely reduced or lost | Usually protected |

| Excess Payment | Usually paid by you, non-recoverable | Usually paid by you initially, but recoverable from at-fault party's insurer |

| Premium Increase | Highly probable | Less likely, but possible depending on insurer's policy |

| Claims Process | Your insurer handles your vehicle's repairs and third-party liabilities | Your insurer may handle your repairs, but seeks recovery from the at-fault party's insurer |

| Legal Responsibility | You are deemed responsible for the incident | Another party is deemed responsible for the incident |

Frequently Asked Questions About Car Repair Claims

Does insurance pay to repair a car after an excess?

Yes, if you have comprehensive cover, your insurance policy will pay to repair your car after you have paid your agreed excess. The excess is the initial amount you contribute towards the cost of the repair. For example, if the repair bill is £1,000 and your excess is £250, you pay £250, and your insurer pays the remaining £750. If the accident was caused by another driver and they are identified, you can typically claim the cost of repairs from their insurance provider. In such a 'non-fault' scenario, you wouldn't usually have to pay your own excess, or if you do, your insurer should recover it for you from the at-fault party's insurer.

How long does a car repair claim take?

The duration of a car repair claim can vary significantly. Simple claims involving minor damage can be resolved within a few days to a couple of weeks, from reporting the incident to your car being repaired. More complex claims, especially those involving significant damage, third parties, or injuries, can take several weeks or even months. Factors influencing the timeline include the speed of communication between parties, availability of parts, garage workload, and whether liability is disputed.

Can I choose my own garage for repairs?

While your insurer will typically recommend or require you to use one of their approved repairers, you generally have the right to choose your own garage. However, there can be implications. If you use a non-approved garage, your insurer might require an independent assessment of their quote and may only authorise repairs up to the cost they would have paid their own network garage. You might also need to pay the garage directly and then claim reimbursement, which can be a longer process than direct billing through an approved repairer.

It's very likely that your car insurance premium will increase after making a claim, especially if it's a fault claim. Even a non-fault claim can sometimes lead to a slight increase, as insurers may view you as a higher risk due to your involvement in an incident, regardless of fault. However, the impact on your premium is usually much less severe for a non-fault claim, and your no-claims bonus is typically protected if the claim is genuinely non-fault and the costs are recovered from the other party's insurer.

What if my car is 'written off' (total loss)?

If your car is deemed a 'total loss' or 'written off' by your insurer, it means the cost of repairs is uneconomical relative to the car's market value, or the damage is so severe that it's unsafe to repair. In this scenario, your insurer will offer you a cash settlement based on the vehicle's market value immediately before the accident, less any applicable excess. Once you accept the settlement, the insurer takes ownership of the damaged vehicle (the salvage). You then use the settlement money to buy a replacement vehicle.

What if the other driver is uninsured or untraceable?

If the other driver is uninsured, flees the scene, or is untraceable, claiming can be more complicated. If you have comprehensive cover, your insurer will still cover your damages, but you will likely have to pay your excess, and your no-claims bonus might be affected as your insurer cannot recover costs from another party. In the UK, the Motor Insurers' Bureau (MIB) acts as a last resort for victims of uninsured or untraced drivers, providing compensation for injuries and, in some cases, property damage. You would need to report the incident to the police and then contact the MIB directly or through your insurer.

What If You're Unhappy with the Outcome?

If you are dissatisfied with your insurer's handling of your claim, the repair quality, or the settlement offer, you have avenues for recourse:

- Internal Complaints Procedure: First, raise a formal complaint directly with your insurance company. They have a procedure for handling complaints and must respond within a set timeframe.

- Financial Ombudsman Service (FOS): If you remain unhappy after exhausting your insurer's internal complaints procedure, you can escalate your complaint to the Financial Ombudsman Service. The FOS is an independent body that resolves disputes between consumers and financial services firms. Their decision is binding on the insurer.

- Legal Advice: For complex or high-value disputes, seeking independent legal advice may be necessary.

Navigating a car repair claim can be a daunting prospect, but by understanding the process, knowing your rights, and acting promptly, you can ensure a smoother journey towards getting your vehicle back on the road. Always keep meticulous records of all communications, photos, and documents related to your claim.

If you want to read more articles similar to Navigating Your Car Repair Claim in the UK, you can visit the Insurance category.