03/06/2010

Navigating the labyrinth of business expenses can often feel like a drive through a dense fog, especially when it comes to vehicles. For countless UK businesses, from sole traders to limited companies, a car is not just a mode of transport; it's a fundamental tool for operations. Understanding which automotive costs qualify as legitimate business expenses, how to claim them, and the nuances of VAT and capital allowances, is crucial for maintaining healthy finances and ensuring compliance with HM Revenue & Customs (HMRC) rules. Getting this right can lead to significant tax savings, while missteps can result in penalties or missed opportunities. This comprehensive guide aims to demystify car expense claims, offering clarity on everything from purchasing and leasing to daily running costs and eventual sale.

The rules surrounding vehicle expenses can appear intricate, varying depending on factors such as your business structure (e.g., sole trader vs. limited company), how the vehicle is used, and the accounting method you employ. We'll delve into the specifics, providing practical insights into VAT reclaim, the treatment of loan interest, and the two primary methods for claiming motor expenses for business travel. By the end, you'll have a clearer roadmap for managing your vehicle-related finances effectively.

Understanding VAT on Vehicle Purchases

One of the most common questions businesses have revolves around reclaiming Value Added Tax (VAT) on the purchase of a vehicle. Broadly speaking, the answer is often 'no', but there are specific, important exceptions that could allow you to reclaim this significant cost.

Generally, VAT cannot be reclaimed on the purchase of a car if it is available for private use, even if that private use is minimal. This rule is in place to prevent businesses from gaining a tax advantage on assets that also serve a personal purpose. However, there are two primary scenarios where reclaiming VAT on a car purchase becomes possible:

- The Business Is the Car: If your business inherently involves the car itself, such as a taxi service, a driving instructor's vehicle, or a car hire firm, then the vehicle is considered stock in trade, and the VAT can typically be reclaimed. In these cases, the car is the direct means by which your business generates income.

- Exclusive Business Use: If the car is used exclusively for business purposes and is genuinely not available for any private use whatsoever, you may be able to reclaim the VAT. This is a strict condition, and you must be able to provide robust evidence to HMRC to prove that no private use occurs. This could include keeping the car on business premises overnight, having a clear policy prohibiting private use, and ensuring no private mileage is ever recorded.

VAT Rules for Leasing a Car

The rules for reclaiming VAT are somewhat more flexible when you lease a car compared to purchasing one outright. This offers more scope for businesses to reclaim a portion of the VAT paid on lease costs.

- Full VAT Reclaim (100% Business Use): Similar to purchasing, if the leased car is used exclusively for business purposes with no personal use, and you can demonstrate this to HMRC with sufficient evidence, you can reclaim the full VAT on the lease costs.

- Partial VAT Reclaim (Business and Personal Use): If the leased car is available for both business and personal use, you are generally able to claim 50% of the VAT on the lease payments. This 50% block applies regardless of the actual proportion of business use, provided there is some private use. The remaining 50% is considered to relate to the private use of the vehicle and is not reclaimable.

It's also important to note that VAT can be reclaimed on fuel used specifically for business journeys, regardless of whether the car is owned or leased. However, VAT on fuel used for private journeys cannot be reclaimed. If a car is used for both business and private travel, you'll need to keep accurate records to separate the business fuel costs from private ones. Many businesses opt for the 'fuel scale charge' if claiming VAT on fuel for cars with mixed use, which simplifies the process but may not always be the most tax-efficient.

When dealing with VAT on vehicle purchases or leases, it is paramount to provide your accountant with all relevant documentation, including the sale and purchase agreements, lease contracts, and any financing arrangements. Your accountant will then accurately record these transactions in your accounting software and ensure they are correctly reflected in your VAT returns, preventing potential issues with HMRC.

Decoding Loan Repayments and Interest

Many businesses opt to finance their vehicle purchases through loans. A common misconception is that the entire loan repayment can be claimed as a business expense. This is not the case. When you make a loan repayment, it typically consists of two components: the principal repayment and the interest charge.

- Principal Repayment: The portion of your payment that reduces the outstanding loan balance is not a business expense. This is because the principal repayment relates to the acquisition of an asset (the car), not an operational cost. It's a movement of capital, not an expense.

- Interest on the Loan: Conversely, the interest charged on the loan *can* be claimed as a legitimate business expense. This is because interest is the cost of borrowing money to finance the asset, making it a financial expense of running your business. Your accountant will typically make the necessary adjustments to separate the interest component from the principal when preparing your financial statements, ensuring only the allowable interest is claimed against your profits.

What happens when it’s time to sell a vehicle that has been used for business purposes? The process isn't as simple as just selling it; there are tax implications to consider, especially if you've previously claimed VAT or capital allowances.

- VAT Implications: If you initially claimed VAT on the purchase price of the vehicle (which, as discussed, is rare for cars unless it's for exclusive business use or the business *is* the car), then you are generally required to charge VAT on the sale price when you dispose of it. This ensures that HMRC recoups the VAT that was originally reclaimed.

- Market Value for Related Party Sales: If you sell the vehicle to yourself (e.g., moving it from your business to personal ownership) or to a related party, you cannot simply sell it for a nominal sum (like £1). HMRC requires that such transactions are conducted at the vehicle's market value. This prevents artificial depreciation or profit manipulation for tax purposes.

- Tax on Profit: If you sell the vehicle for more than its tax written-down value (its original cost minus any capital allowances claimed), any profit realised from the sale will generally be subject to Corporation Tax (for limited companies) or Income Tax (for sole traders). However, given that vehicles typically depreciate in value over time, it's more common for a loss to be incurred on sale rather than a profit, meaning this particular tax consequence doesn't apply as frequently.

- Fixed Asset Register: From an accounting perspective, the vehicle needs to be formally removed from your business's fixed asset register. This is an administrative task that your accountant is best placed to handle, ensuring your balance sheet accurately reflects your assets.

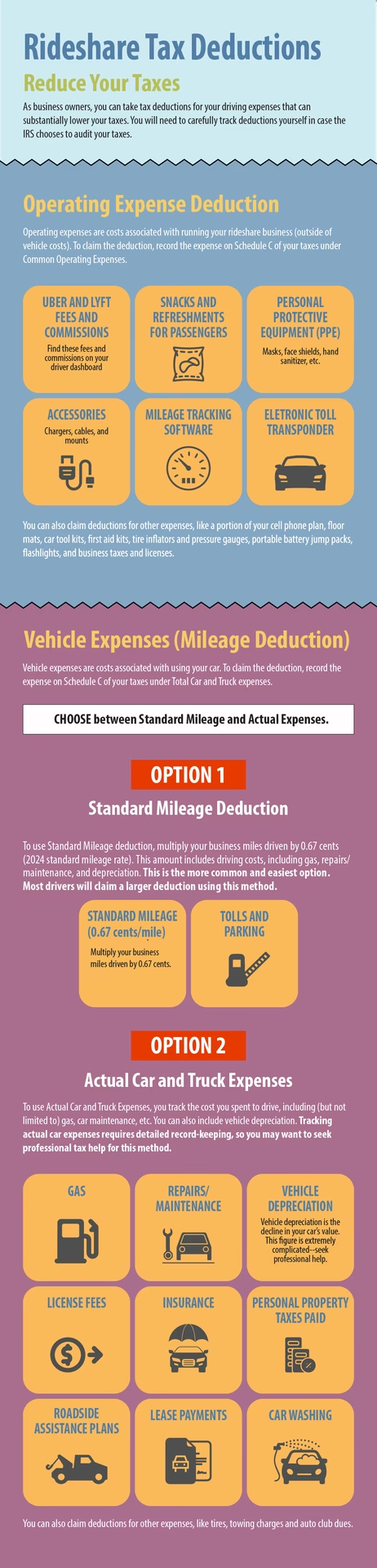

Claiming Motor Expenses for Business Travel (Especially for Sole Traders)

For sole traders or self-employed individuals who use their own personal vehicle for business travel, claiming motor expenses is a key area for tax relief. HMRC offers two main methods to calculate how much you can claim: the simplified expenses method or the actual cost method.

Simplified Expenses: The Straightforward Approach

As the name suggests, the simplified expenses method is the easiest way to calculate your motor expense claims. This method allows you to claim a flat rate per mile for business journeys, regardless of your actual running costs. It removes the need to meticulously track every fuel receipt, service bill, or insurance premium.

For the tax year 2020/21 (and often remaining consistent for subsequent years, though always check the latest HMRC guidance), the flat rates are:

- Cars and Vans: £0.45 per mile for the first 10,000 business miles in a tax year.

- Cars and Vans: £0.25 per mile for every subsequent mile over 10,000 in the same tax year.

- Motorcycles: £0.24 per mile for all business miles.

This method covers all vehicle running costs, including fuel, servicing, insurance, vehicle tax, and depreciation. Therefore, if you use simplified expenses, you cannot claim these costs separately. To use this method, you only need to keep an accurate record of your business mileage. This can be done using a physical logbook in your car, a spreadsheet on your computer, or a dedicated mileage tracking app on your smartphone. The key is consistency and accuracy to justify your claim if HMRC were to enquire.

Actual Cost Method: Detailed Tracking for Maximum Claims

The actual cost method involves calculating the precise proportion of your vehicle's running costs that relate to business use. This method can potentially lead to a higher claim if your actual costs are significantly above the simplified rates, but it requires much more rigorous record-keeping.

To use this method, you'll need to meticulously track all expenses related to your vehicle, including:

- Fuel costs

- MOTs and servicing

- Insurance premiums

- Breakdown cover subscriptions

- Repairs and maintenance

- Vehicle tax (road tax)

- Lease payments (if applicable)

- Depreciation (though this is typically accounted for via capital allowances, discussed later)

Once you have a total for these costs, you then need to determine the proportion of your vehicle's use that was for business purposes. This is typically done by comparing your business mileage to your total mileage for the tax year. For example, if you drove 10,000 miles in total during the year, and 6,000 of those miles were for business, you could claim 60% of your total vehicle running costs. To do this accurately, you'll need to record your car's mileage at the beginning and end of the tax year, in addition to maintaining a detailed log of all business journeys.

Choosing Your Method Wisely

A crucial rule to remember is that once you choose a method for claiming motor expenses for a particular vehicle, you must stick with that method for as long as you own that car. You cannot switch between simplified and actual cost methods from one year to the next for the same vehicle. This is to prevent businesses from 'picking and choosing' the most favourable method each year based on fluctuating costs or mileage.

However, if you change your car, you are free to choose a new method for the new vehicle. In such a scenario, it often makes sense to keep records for both methods for the first year of ownership of the new car. This allows you to compare the potential claims under each method and select the one that is most tax-efficient for your specific circumstances moving forward.

Hiring Vehicles for Business Trips

If you need to hire a vehicle solely for a specific business trip, the rules are much simpler. You can claim the full cost of the vehicle hire, along with any associated expenses such as fuel, parking, and congestion charges, as a legitimate business expense. This is separate from the expenses related to your own personal car and doesn't affect your chosen method for claiming those costs.

Always remember that tax rules can change, so it is always advisable to check the latest guidance from HMRC or consult with a qualified accountant or tax adviser before making any claims. A professional can provide tailored advice based on your unique business situation.

Capital Allowances and Other Allowable Expenses

Beyond the daily running costs and mileage claims, there are other significant vehicle-related expenses that businesses can claim, primarily through capital allowances when purchasing a vehicle, and other allowable business expenses for everyday operational costs.

Allowable business expenses are costs that are incurred wholly and exclusively for the purpose of your trade. For vehicles and travel, these can include a wide range of expenditures:

| Allowable Business Expenses | Non-Allowable Expenses |

|---|---|

| Vehicle insurance | Non-business driving or travel costs |

| Repairs and servicing | Fines or penalty charges (e.g., parking fines, speeding tickets) |

| Fuel (for business journeys) | Travel between home and a regular place of work |

| Parking charges (for business purposes) | Personal vehicle modifications |

| Hire charges (for business use) | |

| Vehicle tax (road tax) | |

| Breakdown cover | |

| Train, bus, tram, air, and taxi fares (for business trips) | |

| Hotel rooms (for overnight business trips) | |

| Meals (on overnight business trips) |

It's crucial to distinguish between business and non-business travel. For instance, your daily commute from home to your regular place of work is generally considered non-allowable, as it's a personal journey. However, travel from your regular workplace to a client's site, or between different business premises, would typically qualify as business travel.

Buying Vehicles: Capital Allowances

When you purchase a vehicle for your business, the cost isn't usually deducted as a straightforward expense in the year of purchase (unless it's a van or certain other vehicles under specific accounting methods). Instead, the cost is relieved through 'capital allowances'. Capital allowances allow businesses to write off the cost of certain assets against their taxable profits over time, reflecting the asset's depreciation.

- Traditional Accounting (Accruals Basis): If your business uses traditional accounting (also known as the accruals basis), and you purchase a vehicle for your business, you will claim capital allowances on the cost of the purchase. The rate at which you can claim these allowances depends on the vehicle's CO2 emissions and whether it's new or used. For example, low-emission cars might qualify for a higher first-year allowance, allowing a larger deduction in the year of purchase.

- Cash Basis Accounting: If your business uses cash basis accounting (a simpler method often used by smaller businesses and sole traders), the rules for claiming the cost of vehicles differ slightly. If you buy a car for your business, you will claim the cost as a capital allowance, provided you are *not* using simplified expenses for your mileage claims for that vehicle. For all other types of vehicles (such as vans, lorries, or motorcycles), the cost is claimed as an allowable expense in the year of purchase, rather than through capital allowances. This distinction is important and highlights why understanding your accounting method is key.

The rules around capital allowances can be complex, particularly with the varying rates and conditions for different types of vehicles and emissions levels. It is always best to consult with your accountant to ensure you are claiming the maximum allowable capital allowances, as these can significantly reduce your taxable profits.

Important Considerations

Regardless of the method you choose for claiming motor expenses or the type of vehicle you operate, thorough record-keeping is non-negotiable. HMRC requires businesses to maintain accurate records to substantiate any claims made. This includes mileage logs, receipts for all expenses, invoices for purchases, and details of financing arrangements. In the event of an HMRC enquiry, robust records will be your best defence.

Furthermore, the details of what and how much you can claim do change from time to time, as HMRC updates its guidance and tax legislation. Therefore, staying informed about the latest rules or, more practically, relying on the expertise of a professional accountant, is crucial to ensure ongoing compliance and to maximise your eligible claims.

Frequently Asked Questions About Car Expenses

- Can I claim VAT on a car if I use it for personal trips sometimes?

- Generally, no, if you purchased the car. However, if you lease the car and it's available for both business and private use, you can typically reclaim 50% of the VAT on the lease payments. For fuel, you can only reclaim VAT on the portion used for business journeys, not private.

- Do I need to keep a logbook for my car expenses?

- Yes, absolutely. Whether you use the simplified expenses method or the actual cost method, you must keep accurate records of your business mileage. A logbook, spreadsheet, or mileage tracking app is essential to substantiate your claims to HMRC if requested.

- What's the main difference between simplified and actual cost methods?

- The simplified method uses a flat rate per mile for business journeys, covering all running costs without needing individual receipts. The actual cost method requires you to track all specific expenses (fuel, servicing, insurance, etc.) and then claim a proportion based on your business mileage. Simplified is easier to administer, while actual cost can sometimes lead to a higher claim if your running costs are high.

- Can I claim for my daily commute to work?

- No, travel between your home and your regular place of work is generally considered ordinary commuting and is not an allowable business expense for tax purposes. Business travel refers to journeys made for specific business activities, such as visiting clients, suppliers, or attending conferences.

- Are the rules different if I buy a van instead of a car for my business?

- Yes, generally, the rules are more favourable for vans, as they are typically considered commercial vehicles. For VAT, it's often easier to reclaim the full VAT on a van purchase if it's used for business. For capital allowances, vans often qualify for more generous allowances, such as the Annual Investment Allowance, which allows you to deduct the full cost in the year of purchase, irrespective of accounting method, up to a certain limit.

Managing vehicle expenses for your UK business can be a complex but rewarding area of financial management. By understanding the distinctions between VAT on purchases versus leasing, the nuances of loan interest, the two primary methods for claiming mileage, and the role of capital allowances, you can ensure your business is maximising its tax efficiency while remaining fully compliant with HMRC regulations. Remember, accurate record-keeping is the bedrock of any successful expense claim, and when in doubt, the most prudent course of action is always to seek advice from a qualified accounting professional. They can provide tailored guidance that aligns with your specific business structure and operational needs, helping you navigate the road ahead with confidence.

If you want to read more articles similar to Claiming Car Expenses for Your UK Business, you can visit the Vehicles category.