10/05/2018

In the intricate world of commercial transactions, a bill of exchange serves as a crucial financial instrument, a written order binding one party to pay a fixed sum of money to another party on demand or at a predetermined future date. While these instruments are designed to facilitate smooth and secure payments, what happens when the agreed-upon payment fails to materialise? The non-payment of a bill of exchange can throw a significant spanner in the works for creditors, impacting cash flow and causing considerable financial stress. Fortunately, the legal framework provides specific mechanisms, known as 'bill of exchange actions', to protect the rights of the creditor and ensure that obligations are met.

Understanding these actions is paramount for anyone involved in commercial dealings, whether you're a small business owner, a large corporation, or simply someone who has accepted a bill of exchange. This article will delve into the various remedies available when a bill of exchange is dishonoured, explaining the nuances of direct and return actions, the critical role of the notarial protest, and other essential steps you can take to reclaim what is rightfully yours. It's about empowering you with the knowledge to navigate these challenging situations effectively and pursue the fulfilment of the debt.

- What Happens When a Bill of Exchange Isn't Paid?

- The Direct Bill of Exchange Action

- The Return Bill of Exchange Action

- Direct vs. Return Bill of Exchange Actions: A Comparison

- What to Do in Case of Non-Payment of the Bill of Exchange?

- The Equivalent Declaration: A Simpler Alternative

- What is a Reverse Bill of Exchange (Back Draft)?

- Navigating the Path to Recovery: Key Considerations

- Frequently Asked Questions (FAQs)

- Q: What is the primary purpose of bill of exchange actions?

- Q: Is a protest always necessary for an unpaid bill of exchange?

- Q: How long do I have to initiate a direct action for non-payment?

- Q: Can I use an equivalent declaration instead of a notarial protest?

- Q: What is a 'back draft' in the context of an unpaid bill of exchange?

- Conclusion

What Happens When a Bill of Exchange Isn't Paid?

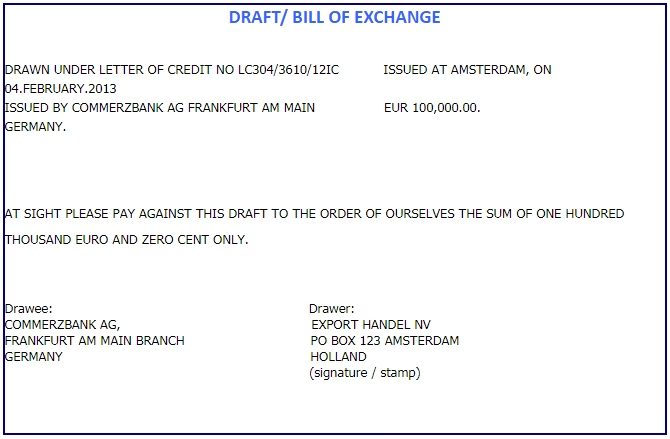

When a bill of exchange is not paid or accepted, it signifies a breach of the underlying agreement and can have immediate financial repercussions for the holder of the bill. The primary purpose of a bill of exchange is to guarantee payment, and when this guarantee is broken, the law provides recourse. The Bill of Exchange and Check Law (LCCh), specifically Article 49, outlines the two principal avenues available to the creditor to enforce their rights: the direct action and the indirect, or return, action. These actions are designed to be a protective and conservative measure for the creditor's credit, ensuring that they have robust legal tools to pursue the debt.

The default can arise from two main scenarios: either the drawee refuses to accept the bill upon presentation (non-acceptance), or they fail to make the payment when the bill matures (non-payment). In either case, the creditor is not left without options. The choice between a direct action and a return action often depends on who the creditor wishes to pursue and the specific circumstances surrounding the dishonour of the bill. It's crucial to understand the distinct characteristics and requirements of each action to determine the most appropriate course of action.

The Direct Bill of Exchange Action

The direct bill of exchange action is perhaps the most straightforward and immediate remedy available to a creditor when a bill of exchange is dishonoured. This action is specifically exercised against the principal debtor – the individual or entity who is ultimately responsible for the payment of the bill. A defining characteristic of the direct action, as stipulated by the Bill of Exchange and Check Law, is that it can be initiated without the need for a formal 'protest'. This simplifies the process significantly, as it removes a procedural hurdle that is often associated with other forms of debt recovery.

The absence of the protest requirement means that the creditor can proceed directly against the debtor armed solely with the unpaid bill of exchange. This is a considerable advantage, as it streamlines the legal process and potentially speeds up recovery efforts. Case law from Provincial Courts consistently supports this, distinguishing the direct action from return actions which do typically require a protest. Therefore, if you are the holder of an unpaid bill and the primary party liable is the debtor, a direct action allows you to pursue them without additional formal steps beyond presenting the bill itself as evidence of the debt.

It is important to note the statute of limitations for the direct action. According to Article 88 of the Bill of Exchange and Check Law, this action has a limitation period of three years from the maturity date of the bill of exchange. This means creditors must act within this timeframe to preserve their right to pursue the debt via this route. Missing this deadline could significantly jeopardise the ability to recover funds, making timely action paramount.

The Return Bill of Exchange Action

In contrast to the direct action, the return bill of exchange action offers a broader scope for recovery, as it can be exercised against any person who has signed the exchange instrument. This includes, but is not limited to, endorsers, drawers (if they are not the principal debtor), and guarantors. This provides a safety net for the creditor, allowing them to pursue other parties in the chain of endorsement if the primary debtor defaults. However, this broader reach comes with specific requirements that must be diligently met.

The key distinguishing feature of the return action is the mandatory requirement for a notarial protest to be filed. Unlike the direct action, the law explicitly establishes the lifting of the protest as a formal prerequisite for exercising the return action. The purpose of this requirement is to provide formal, irrefutable proof that the expired bill of exchange has indeed not been previously accepted or paid. It serves as an official declaration of dishonour, giving notice to all parties liable on the bill that their obligation has arisen.

Without a valid notarial protest (or an equivalent declaration, which we will discuss later), the creditor generally cannot pursue a return action against the signatories. This makes the protest a critical procedural step, ensuring that all parties are properly informed of the bill's non-payment or non-acceptance and that the creditor has followed the necessary legal protocols. While it adds a layer of complexity compared to the direct action, the return action significantly expands the pool of potential parties from whom the debt can be recovered, thereby increasing the likelihood of successful collection.

Direct vs. Return Bill of Exchange Actions: A Comparison

Understanding the fundamental differences between these two vital actions is key to choosing the correct legal path. Here's a comparative overview:

| Feature | Direct Bill of Exchange Action | Return Bill of Exchange Action |

|---|---|---|

| Against Whom Exercised? | Principal debtor only | Any person who signed the exchange instrument (drawer, endorsers, guarantors) |

| Protest Requirement? | No (not required) | Yes (notarial protest or equivalent declaration is mandatory) |

| Purpose of Protest | Not applicable | To formally prove non-acceptance or non-payment to all signatories |

| Statute of Limitations | Three years from maturity date | Varies (often shorter than direct action for endorsers, specific rules apply to different signatories) |

| Complexity | Generally simpler, more direct | More complex due to protest requirement and multiple potential parties |

| Coverage | Limited to the primary obligor | Broader, covering all parties in the chain of liability |

What to Do in Case of Non-Payment of the Bill of Exchange?

When faced with a dishonoured bill of exchange, prompt and precise action is essential. As previously mentioned, the notarial protest is a pivotal act, particularly if you intend to pursue a return action. Its primary purpose is to formally prove the lack of acceptance or the lack of payment of a bill of exchange. It's not just a formality; it's an act with significant legal weight, confirming the default to all relevant parties.

A notarial protest, as its name suggests, is based on a notarial act. This means it must be carried out in the presence of a notary public, a legal professional who certifies the authenticity of signatures and documents. The notary's involvement gives the protest an eminently probative character, as their official presence reaffirms the fact of non-acceptance or non-payment. This formal documentation is regulated by Articles 51 and following of the Exchange and Check Law, underscoring its importance as an essential act for exercising the action of return.

However, there are specific circumstances where a notarial protest might not be necessary. The law provides an exception in cases of force majeure, such as natural disasters or unavoidable circumstances that prevent the protest from being made within the stipulated timeframes. In such extraordinary situations, the requirement for a notarial protest may be waived, though other forms of proof might still be required.

The timing of the protest is crucial. If the protest is for non-acceptance, it must be made within the term fixed for the presentation of the acceptance or within five days after its expiration. If the protest is for non-payment, which is more common, it must be made within eight days after the due date of the bill. Adhering to these strict deadlines is absolutely vital; failure to protest within the prescribed time can lead to the loss of rights against endorsers and other parties liable on the bill via the return action.

The Equivalent Declaration: A Simpler Alternative

Recognising the practicalities of commercial dealings, the Exchange and Check Law offers a simplified alternative to the formal notarial protest. Article 51.2 of the Law states that a declaration made directly on the exchange instrument itself can be equivalent to a notarial protest. This provision offers a more convenient and often quicker method of formally evidencing the dishonour of the bill, especially when a notary is not immediately accessible or when the parties wish to streamline the process.

For this declaration to be legally equivalent to a notarial protest, it must meet specific criteria: it must be signed and dated by the creditor, and it must explicitly state the denial of acceptance or payment. This declaration effectively serves the same probative purpose as a notarial act, providing formal notice of the bill's dishonour. The same strict deadlines that apply to the notarial protest also apply to this equivalent declaration. For non-payment, the declaration must be made within eight days from the bill's expiration. For lack of acceptance, it must be made within five days from its expiration.

This 'equivalent declaration' provides flexibility for creditors, allowing them to fulfil the formal requirement for a return action without necessarily incurring the time and cost associated with a notary. It's a pragmatic solution that acknowledges the fast-paced nature of modern business, while still maintaining the necessary legal rigour to protect the creditor's rights.

What is a Reverse Bill of Exchange (Back Draft)?

In situations where a creditor has exercised the action of return and is seeking reimbursement, the Exchange and Check Law provides for a mechanism known as a "back draft" or a reverse bill of exchange. Article 62 of the Law stipulates that the creditor who exercises the action of return has the right to reimburse themselves by means of a new bill of exchange. This new bill is typically drawn at sight (meaning payable on demand) on any of the obligors who are liable for the original unpaid bill.

The purpose of a back draft is to consolidate the outstanding debt, including any accrued interest and costs incurred due to the original non-payment. This new bill of exchange must contain the nominal amount of the unpaid bill plus any agreed-upon interest. It essentially creates a new, legally binding instrument for the recovery of the debt, drawn on a party who is obligated to pay under the original bill's terms.

However, the main challenge with a reverse bill of exchange, much like the original, is the potential for a lack of acceptance by the debtor. While it provides a formal means of demanding reimbursement, it does not automatically guarantee payment. If the debtor on the back draft also refuses to accept or pay, the creditor would then need to pursue further actions, potentially including another round of direct or return actions based on the new instrument. It’s a tool for formalising the claim for reimbursement rather than an absolute guarantee of immediate recovery.

Successfully recovering funds from an unpaid bill of exchange requires not just knowledge of the legal actions but also a strategic approach. Timeliness is paramount. As highlighted, strict deadlines apply to protests and declarations. Missing these can significantly weaken your position, particularly for return actions. Therefore, as soon as a bill is dishonoured, assessing the situation and acting swiftly is crucial.

Furthermore, careful documentation is essential. Maintain meticulous records of the bill of exchange itself, any communication regarding its presentation or dishonour, and all steps taken, such as protests or equivalent declarations. This documentation will serve as vital evidence should legal proceedings become necessary. Understanding who signed the bill and in what capacity (drawer, endorser, acceptor) will also help determine the most effective course of action – whether a direct action against the primary debtor or a return action against other signatories is more appropriate.

While the legal framework aims to protect creditors, proactive measures can often prevent the need for extensive legal battles. This includes performing due diligence on parties you engage with, clearly defining terms, and ensuring that bills of exchange are properly drafted and presented. However, when default occurs, knowing your rights and the available legal actions is your strongest defence.

Frequently Asked Questions (FAQs)

Q: What is the primary purpose of bill of exchange actions?

A: The primary purpose of bill of exchange actions is to provide legal recourse for the creditor when a bill of exchange is dishonoured due to non-acceptance or non-payment. These actions are designed to protect the creditor's interests and facilitate the recovery of the debt, ensuring the fulfilment of the financial obligation.

Q: Is a protest always necessary for an unpaid bill of exchange?

A: No, a protest is not always necessary. For a 'direct action' against the principal debtor, a protest is generally not required. However, for a 'return action' against any other signatory on the bill (such as endorsers), a notarial protest or an equivalent declaration on the bill itself is a mandatory formal requirement.

Q: How long do I have to initiate a direct action for non-payment?

A: You have a statute of limitations period of three years from the maturity date of the bill of exchange to initiate a direct action against the principal debtor. It is crucial to adhere to this timeframe to preserve your legal right to pursue the debt via this route.

Q: Can I use an equivalent declaration instead of a notarial protest?

A: Yes, the Exchange and Check Law allows for an 'equivalent declaration' made directly on the bill of exchange itself to substitute a notarial protest. This declaration must be signed and dated by the creditor, explicitly denying acceptance or payment, and must be made within the same strict timeframes as a formal protest.

Q: What is a 'back draft' in the context of an unpaid bill of exchange?

A: A 'back draft', or reverse bill of exchange, is a new bill drawn by the creditor (who has exercised a return action) on any of the obligors of the original unpaid bill. Its purpose is to reimburse the creditor for the nominal amount of the unpaid bill plus any agreed interest and costs. It's a mechanism for formalising the claim for reimbursement.

Conclusion

The non-payment or non-acceptance of a bill of exchange can present a significant challenge for creditors. However, the legal framework, particularly the Exchange and Check Law, provides robust mechanisms to address such defaults. Bill of exchange actions, encompassing both the direct and return actions, are granted to the creditor to pursue the fulfilment of the debt and protect their credit interests. They are inherently protective and conservative in nature, designed to uphold the integrity of commercial transactions.

While the direct action offers a straightforward path against the principal debtor without the need for a protest, the return action extends the reach to all signatories but necessitates the crucial step of a notarial protest or an equivalent declaration within strict time limits. Understanding these distinct actions, along with the purpose and procedure of the protest and the concept of a reverse bill of exchange, is fundamental for any creditor. Acting promptly, adhering to legal requirements, and maintaining meticulous documentation are key to successfully navigating the complexities of unpaid bills of exchange and ensuring that financial obligations are honoured.

If you want to read more articles similar to Unpaid Bill of Exchange: Your Rights & Actions, you can visit the Automotive category.