17/09/2010

Finding the 'best' car insurance in the UK isn't a simple one-size-fits-all task; it's about securing the ideal cover that aligns perfectly with your individual needs, driving habits, and budget. The market is vast, with numerous providers offering a myriad of policies, each with its own nuances and benefits. Our goal here is to demystify the process, providing you with a comprehensive guide to navigate the options, understand what truly matters, and ultimately help you make an informed decision that ensures you're well-protected without breaking the bank.

Ultimately, the best policy is one that offers the right level of cover, is there for you in your hour of need, and comes at a price you can afford. This guide will delve into various aspects, from understanding different policy types and key factors influencing premiums to highlighting top providers in specific categories and offering practical tips for saving money.

- Understanding Your Car Insurance Needs

- Key Factors Influencing Your Premium

- Top Car Insurance Providers by Category

- How We Evaluate Car Insurance Policies

- Top 10 Car Insurance Companies by Policy Score (Comprehensive)

- Top 10 Car Insurance Companies by Customer Satisfaction (December 2023)

- How to Secure the Best Car Insurance for You

- Frequently Asked Questions (FAQs)

Understanding Your Car Insurance Needs

Before you even begin to compare quotes, it's vital to have a clear understanding of what you actually need from your car insurance. This isn't just about legal requirements; it's about protecting your investment and your financial well-being. Consider your driving frequency, the value of your vehicle, where you park it, and who else might be driving it.

Types of Car Insurance Cover

In the UK, there are three primary levels of car insurance cover:

- Third Party Only (TPO): This is the minimum legal requirement. It covers damage to other people's vehicles or property, and injury to other people, but it does not cover any damage to your own car if you're at fault. While often perceived as the cheapest, this isn't always the case, so always compare.

- Third Party, Fire and Theft (TPFT): This includes everything covered by TPO, plus protection for your own vehicle if it's stolen or catches fire. It's a step up in protection for your car, but still won't cover damage if you cause an accident.

- Comprehensive: As the name suggests, this is the most extensive level of cover. It includes everything from TPFT, but crucially, it also covers damage to your own vehicle, even if you are responsible for the accident. Many comprehensive policies also include additional benefits such as a courtesy car, personal belongings cover, and windscreen repair. Surprisingly, comprehensive cover can sometimes be more affordable than TPO or TPFT due to the risk profiles associated with drivers choosing different levels of cover.

Car insurance premiums are highly personalised, calculated by complex algorithms that assess numerous risk factors. Understanding these can help you find ways to reduce your costs. Here are some of the most significant:

- Your Vehicle: The make, model, age, engine size, and value of your car all play a role. High-performance, luxury, or frequently stolen models will typically command higher premiums. Every car is assigned to an insurance group, which helps insurers gauge risk.

- Your Driving History: A clean driving record with a substantial no-claims bonus is one of the most effective ways to lower your premium. Conversely, convictions or previous claims will increase it.

- Your Age and Experience: Young or newly qualified drivers often face higher premiums due to their lack of experience and statistically higher risk of accidents. Policies like black box (telematics) insurance can help mitigate this.

- Your Location: Where you live and where you regularly park your car can significantly impact your premium. Areas with high crime rates or traffic density typically lead to higher costs.

- Your Occupation: Some professions are deemed higher risk than others, which can affect your premium. Be accurate and explore different descriptions if applicable.

- Annual Mileage: The more you drive, the higher your risk of an accident, so lower mileage can often lead to lower premiums.

- Voluntary Excess: This is the amount you agree to pay towards a claim before your insurer contributes. Opting for a higher voluntary excess can reduce your premium, but ensure you can comfortably afford it if you need to make a claim.

Top Car Insurance Providers by Category

While the 'best' insurer is subjective, certain companies excel in specific areas. Based on extensive analysis and customer feedback, here are some top picks:

Best for Cheapest Rates: LV=

LV= frequently offers competitive quotes across various age groups. Their comprehensive policy boasts features like personal possessions cover (£300), accident cover (up to £10,000), and EU cover for 180 days. They also provide discounts for insuring multiple vehicles (up to 20% off per extra vehicle) and an uninsured driver promise to protect your no-claims discount. LV= offers policies for standard, classic, and electric cars.

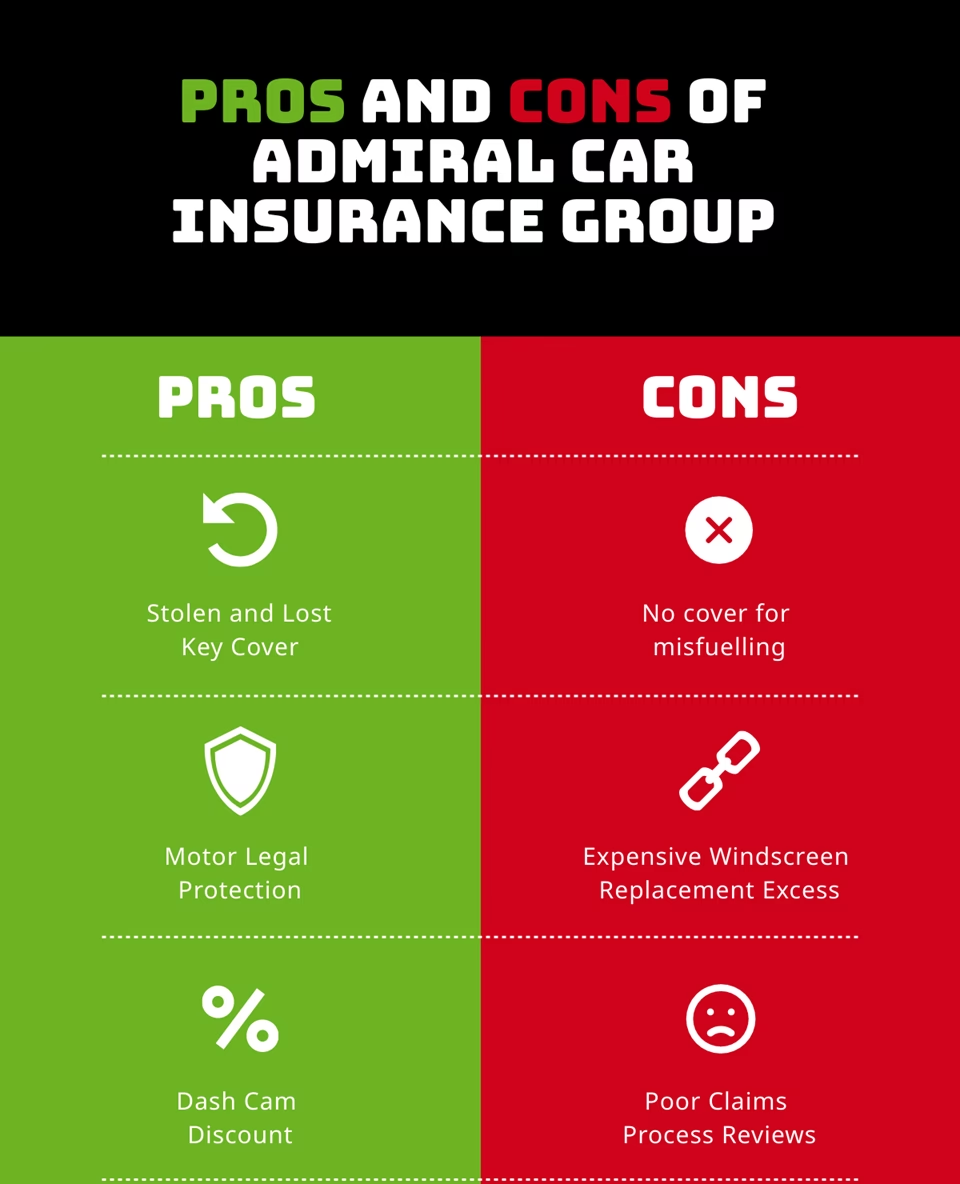

Best for Multi-Car & Customer Service: Admiral

Admiral is a standout for multi-car policies, allowing significant savings by insuring multiple vehicles under one policy with a single renewal date. Each car maintains its own no-claims bonus, and you can even have different cover levels for different cars. They were also a winner in the Finder Customer Satisfaction Awards 2024. However, their claims helplines are not 24/7.

Best for Over-50s: Saga

Saga specialises in cover tailored for drivers over 50, with no upper age limit. Their policies include benefits like discounts for additional cars, an uninsured driver promise, and generous EU cover (unlimited with Saga Select/Plus, 90 days with Saga Standard). Saga Plus also offers the option to fix your premium for three years under certain conditions.

Best for Temporary Insurance: Tempcover

Tempcover offers highly flexible insurance from 1 hour up to 28 days, perfect for short-term needs. A key benefit is that making a claim on a temporary policy won't affect your annual no-claims discount. They cater to learner drivers, students, and full UK licence holders (up to age 78) with a quick 90-second quotation process. The cover is typically comprehensive as standard.

Best for Young Drivers: Hastings Direct

Hastings Direct provides a range of reasonably priced policies for drivers aged 17-25, including telematics (black box) and multi-car options. Their 5-star Defaqto-rated YouDrive black box policy comes with a courtesy car, an uninsured driver promise, and personal belongings cover as standard. They also offer a 24/7 claims line.

Best for Convicted Drivers: Swinton

Swinton is a broker with a dedicated section for convicted drivers, indicating their willingness to cater to those with motoring offences. As a broker, they work with multiple underwriters, increasing the likelihood of finding cover. They offer three levels of comprehensive cover, all including a courtesy car and personal belongings cover (up to £200), and a 24/7 claims helpline.

Best for Black Box Cover: Churchill

Churchill's DriveSure black box policy is designed for younger drivers (17-25) looking to manage insurance costs through careful driving. You're guaranteed a discount in your first year, and premiums won't increase mid-term. Driving is monitored via a smartphone app, tracking speed, smoothness, time/location of driving, and mobile phone use. It includes an uninsured driver promise and no-claims protection.

How We Evaluate Car Insurance Policies

Our assessment of car insurance policies goes beyond just price. We meticulously analyse 29 different policy elements from various providers, factoring in both the level of cover and what actual customers say about the brand. Key aspects considered include:

- Cover Levels: The extent of protection offered for personal possessions, accident cover, EU driving, and specific benefits like new car replacement or key cover.

- Standard Inclusions: Whether essential benefits like a courtesy car, windscreen repair, or onward travel are included as standard or as costly add-ons.

- Flexibility and Restrictions: Any limitations on EU cover (days, distance), payment options, and online policy management capabilities.

- Customer Satisfaction: Direct feedback from thousands of insurance customers on their overall experience, claims process, and willingness to recommend the provider.

Top 10 Car Insurance Companies by Policy Score (Comprehensive)

This table ranks providers based on the comprehensiveness of their policy features and cover levels.

| Rank | Company | Policy Score |

|---|---|---|

| 1 | NFU Mutual | 83.2% |

| 2 | Aviva | 82.51% |

| 3 | Saga | 82.3% |

| 4 | M&S Bank | 81.47% |

| 5 | Direct Line | 80.84% |

| 6 | Sheilas’ Wheels | 79.9% |

| 7 | Age Co | 79.57% |

| 8 | RIAS | 79.24% |

| 9 | AXA | 77.97% |

| 10 | Hastings Direct | 77.02% |

Top 10 Car Insurance Companies by Customer Satisfaction (December 2023)

Customer experience is paramount. This table reflects how satisfied customers are with their insurer.

| Rank | Provider | Overall Satisfaction | Customers who’d recommend |

|---|---|---|---|

| 1 | Admiral | ★★★★★ | 93% |

| 2 | NFU Mutual | ★★★★★ | 89% |

| 3 | Aviva | ★★★★★ | 84% |

| 4 | The AA | ★★★★★ | 80% |

| 5 | LV= | ★★★★★ | 84% |

| 6 | Saga | ★★★★★ | 76% |

| 7 | Direct Line | ★★★★★ | 78% |

| 8 | Hastings Direct | ★★★★★ | 78% |

| 9 | Diamond | ★★★★★ | 83% |

| 10 | Churchill | ★★★★★ | 79% |

How to Secure the Best Car Insurance for You

Finding the right policy involves a strategic approach. Here’s how to make sure you’re getting the optimal deal:

- Compare Policies Extensively: This is arguably the most crucial step. Different insurers use proprietary algorithms, meaning the same level of cover can vary wildly in price. Use multiple comparison websites and also check direct with insurers who aren't on comparison sites (e.g., Direct Line).

- Review Your Policy Annually: Don't just auto-renew! Insurers often offer better deals to new customers. Always shop around a few weeks before your renewal date. Many drivers save hundreds by switching or by haggling with their current provider.

- Adjust Your Excess: Experiment with different voluntary excess amounts. A higher excess usually lowers your premium, but ensure it's an amount you can realistically afford if you need to make a claim.

- Consider Telematics (Black Box) Insurance: Especially beneficial for young drivers or those with a low mileage, a black box monitors your driving habits and can reward safe drivers with lower premiums.

- Enhance Car Security: Fitting an approved alarm, immobiliser, or tracker can make your car less appealing to thieves, potentially reducing your premium. Parking in a secure location, such as a garage or private driveway, also helps.

- Reduce Your Mileage: If your commute changes or you drive less, inform your insurer. Lower annual mileage often translates to lower premiums.

- Limit Named Drivers: Only add drivers who genuinely use your car. Adding young or inexperienced drivers can significantly increase your premium.

- Pay Annually: If possible, pay your premium upfront for the entire year. Paying monthly often incurs interest charges, making the policy more expensive overall.

- Consider Advanced Driving Courses: Completing recognised courses like Pass Plus can sometimes earn you a discount with certain insurers, as it demonstrates a commitment to safer driving.

- Don't Over-insure on Extras: Carefully review optional extras like breakdown cover, legal protection, or enhanced courtesy car options. Only pay for what you genuinely need. You might already have breakdown cover through another service.

Frequently Asked Questions (FAQs)

Which are the best and worst cars to insure?

Generally, smaller, less powerful, and more common cars tend to be cheaper to insure. These vehicles are often in lower insurance groups, cost less to repair, and are less attractive to thieves. Examples often include popular hatchbacks. Conversely, expensive, high-performance, luxury, or rare sports cars usually fall into higher insurance groups, making them more costly to insure due to higher repair costs, greater risk of theft, and potential for higher damage in an accident. Always check a car's insurance group before purchasing if insurance cost is a major concern.

What is the best way to save on my car insurance?

The most effective way to save is to compare quotes from a wide range of providers well in advance of your renewal date (ideally 2-3 weeks). Additionally, increasing your voluntary excess (to an affordable amount), improving your car's security, reducing your annual mileage, considering a telematics policy, and paying your premium annually rather than monthly are all excellent strategies. Only adding essential drivers to your policy and reviewing optional extras can also help trim costs.

How can I cut costs and still get the best level of cover?

To maintain a high level of comprehensive cover while cutting costs, focus on factors within your control. Enhance your car's security with alarms or parking it securely. If your mileage has dropped, update your insurer. Increase your voluntary excess to a manageable level. Consider paying annually to avoid interest. For careful drivers, telematics policies can offer significant savings. If you're a higher-risk driver, adding an older, experienced named driver can sometimes reduce the premium. Finally, always shop around; sometimes, comprehensive cover from one insurer can be cheaper than a third-party policy from another.

When is the best time to renew car insurance?

While there's no single 'best' day, evidence suggests that renewing your car insurance approximately two to three weeks before your current policy expires can lead to significant savings. Studies have shown savings ranging from 17% to 42% compared to renewing on the day of expiry. Insurers often penalise last-minute renewals, so planning ahead is key.

What features should I look for to get the best car insurance policy?

Beyond the price, consider features that are important to your lifestyle. For example, if you frequently travel to Europe, ensure adequate EU cover. If you rely on your car for work, a good courtesy car provision is vital. Look for an uninsured driver promise, which protects your no-claims bonus if hit by an uninsured driver. Check personal belongings cover limits and whether key replacement is included. Compare these 'standard' features across policies, as what's standard for one insurer might be an expensive add-on for another. Prioritise what gives you peace of mind and avoid paying for extras you genuinely don't need.

In conclusion, finding the best car insurance in the UK is a dynamic process that requires careful consideration of your personal circumstances and a proactive approach to comparing the market. The algorithms insurers use are indeed a 'dark art', constantly changing, which is why the advice to shop around annually remains evergreen. By understanding your needs, exploring different providers, and implementing smart saving strategies, you can secure robust protection for your vehicle without unnecessary expense. Remember, the cheapest policy isn't always the best; value lies in the right cover at a fair price, backed by reliable customer service when you need it most.

If you want to read more articles similar to Your Guide to Choosing the Best UK Car Insurance, you can visit the Insurance category.