03/04/2019

Embarking on the journey of enhancing your vehicle's performance through engine remapping is an exciting prospect for many car enthusiasts. However, alongside the thrill of increased power and improved responsiveness, it's crucial to consider the implications for your car insurance. One common query we often encounter is specifically about Admiral Insurance and their stance on remapped vehicles. This article aims to shed light on the general principles of how engine remapping interacts with car insurance, using the scenario provided as a jumping-off point to explore the broader landscape.

What Exactly is Engine Remapping?

At its core, engine remapping, often referred to as 'chipping', is a sophisticated process that involves modifying a car's onboard computer – the Electronic Control Unit (ECU). Think of the ECU as the car's brain; it governs various engine functions, and remapping essentially tweaks its existing software. This adjustment can lead to a number of benefits, including:

- Increased Horsepower: A common goal, leading to a more potent acceleration.

- Enhanced Torque: This translates to better pulling power, especially noticeable when climbing hills or overtaking.

- Improved Fuel Economy: Paradoxically, some remapping strategies can optimise fuel combustion, leading to better MPG, particularly in situations requiring less aggressive acceleration.

- Better Throttle Response: Making the car feel more immediate and eager to respond to your inputs.

- Smoother Power Delivery: A more refined and predictable surge of power.

The process typically involves accessing the ECU via the On-Board Diagnostics (OBD) port, allowing technicians to upload new software or modify existing parameters. The manufacturer's original settings are often designed with a degree of conservatism to cater for a wide range of conditions, driver habits, and to meet emissions regulations. Remapping aims to unlock some of this latent potential.

Types of Remapping

Not all remapping is created equal. Depending on your objectives and your vehicle's specific engine, different approaches can be taken:

- Economy Remaps: Focused on optimising fuel efficiency through adjustments to fuel injection and engine load.

- Performance Remaps: Prioritising power and torque increases, often requiring supporting hardware modifications.

- Tuning Boxes: A less invasive alternative that 'tricks' the ECU into delivering more fuel and boost pressure, without directly altering the ECU's core software. These are often plug-and-play and can be easily removed.

- Automatic Gearbox Remapping: Adjusting shift points and response times for a sportier feel.

It's worth noting that turbocharged engines, both petrol and diesel, are generally the most receptive to remapping, offering the most significant gains. Naturally aspirated engines can also benefit, though the improvements may be less dramatic.

The Crucial Link: Remapping and Car Insurance

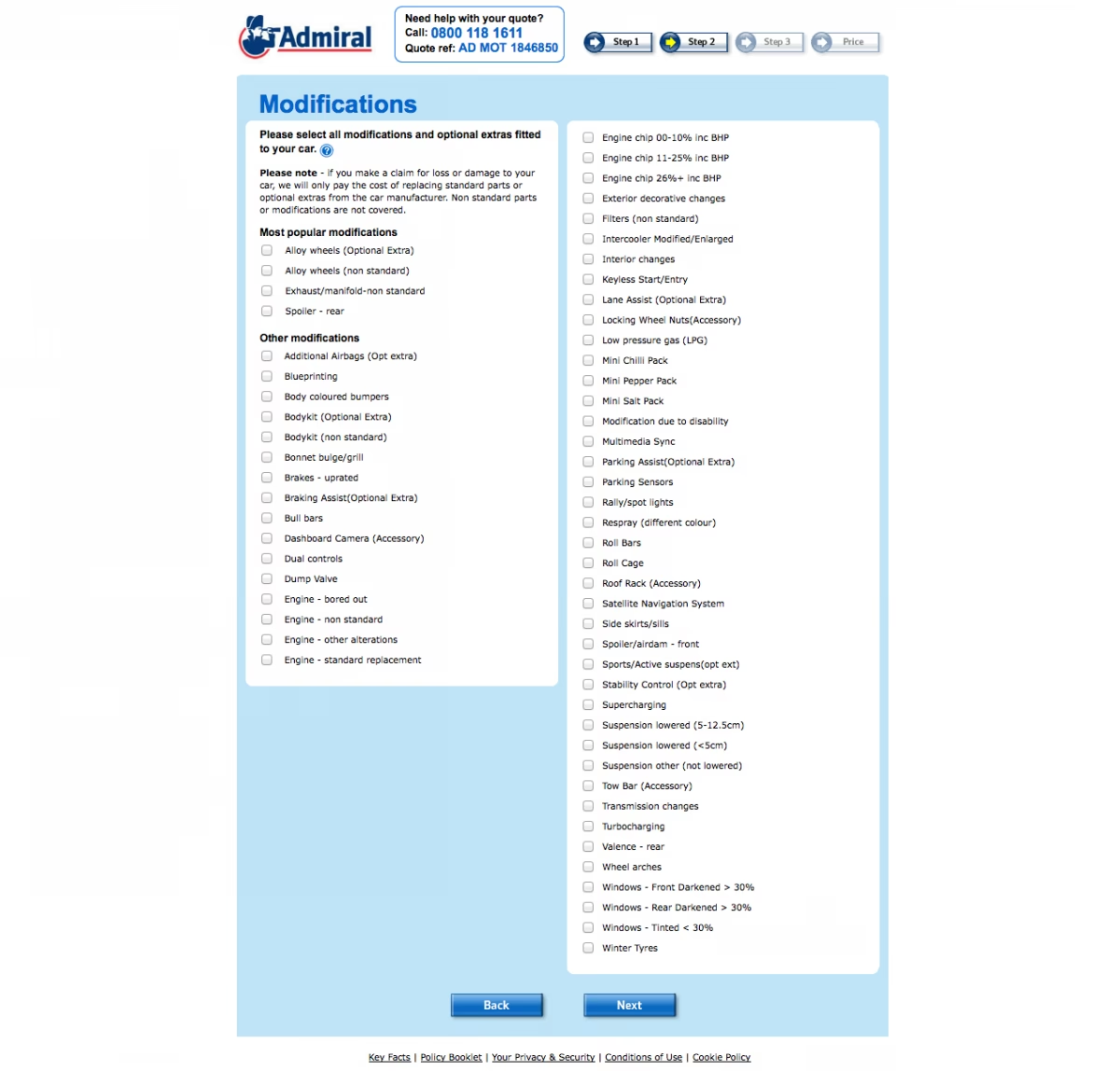

This is where the practicalities and potential pitfalls emerge. Any modification that alters a vehicle's performance, emissions, or characteristics from its original factory specification must, by law and by the terms of your insurance policy, be declared to your insurance provider. Engine remapping falls squarely into this category. The primary reason for this is that remapping can significantly alter the risk profile of your vehicle. An increase in power and speed can, statistically, lead to a higher likelihood of accidents, particularly if the driver is not accustomed to the enhanced performance. Consequently, insurers need to assess this increased risk.

What to Expect When Declaring a Remap to Admiral (and other Insurers)

The experience described in the initial query highlights a common frustration: the process of informing your insurer about modifications. Here’s a breakdown of what you can generally expect:

- The Need to Inform: As soon as you have had a remap (or installed a tuning box), you are obligated to tell your insurance company. Failure to do so could invalidate your policy, leaving you uninsured in the event of a claim.

- Policy Adjustment: Insurers will typically need to make an adjustment to your policy to reflect the modification. This usually involves a policy amendment fee and potentially an increase in your premium.

- Premium Increase Factors: The amount your premium rises will depend on several factors, including the insurer's assessment of the increased risk, the specific performance gains achieved by the remap, your driving history, and your age.

- Coverage Limitations: Some insurers may refuse to cover remapped vehicles altogether, or they might impose specific conditions. The distinction between a 'remap' and a 'superchip' (as experienced in the query) might stem from how different insurers categorise or understand these modifications, or it could be a misunderstanding of terminology. Often, 'chipping' and 'remapping' are used interchangeably, but some insurers might have specific internal classifications.

- Customer Service Challenges: As the anecdotal evidence suggests, contacting insurers to make policy changes can sometimes be a lengthy and frustrating process, involving hold times and potentially unclear communication.

Potential Downsides of Engine Remapping

Beyond the insurance implications, there are other factors to consider:

- Warranty Concerns: If your car is still under manufacturer warranty, a non-manufacturer-approved remap could potentially void it. Always check your warranty terms and conditions.

- Increased Wear and Tear: Higher performance can put additional strain on components like the clutch, brakes, and drivetrain.

- Fuel Grade Requirements: Some performance remaps may necessitate the use of higher-octane fuel, which is typically more expensive.

- Vehicle Saleability: While some buyers might appreciate a remapped car, others may be wary of modifications, potentially affecting resale value.

Remapping vs. Tuning Boxes: An Insurer's Perspective

While both remapping and tuning boxes aim to boost performance, their impact on insurance can be viewed differently by some providers. A tuning box, being a removable device that doesn't permanently alter the ECU's software, might be perceived as less of a fundamental change than a software remap. However, the outcome is often the same: increased power. Therefore, regardless of the method, disclosure to your insurer is paramount.

Frequently Asked Questions

- Do I have to declare a remap to my insurance company?

- Yes, absolutely. It is a modification that changes your vehicle's performance characteristics and must be declared to comply with your policy terms.

- Will my insurance premium increase if I remap my car?

- It is highly likely. Insurers will reassess the risk associated with the increased performance, which often results in a higher premium and a policy amendment fee.

- What is the difference between a remap and a 'superchip' from an insurance perspective?

- This distinction can be confusing and may depend on the insurer's internal classification or a misunderstanding of terminology. 'Chipping' and 'remapping' are often used interchangeably to describe ECU software modifications. It's best to clearly explain that you have modified the engine's software to enhance performance, regardless of the specific term used.

- Can Admiral Insurance cover remapped cars?

- While we cannot speak for Admiral's specific current policies, generally, many insurers do cover remapped vehicles, but typically with an additional cost and a need for disclosure. The best course of action is always to contact them directly to confirm their policy and any associated charges.

- What happens if I don't declare a remap?

- If you have an accident and your insurer discovers you have an undeclared modification such as a remap, they may void your entire policy. This means they would not pay out for any damage to your vehicle or for any third-party claims, leaving you personally liable.

Conclusion

Engine remapping can offer a rewarding boost to your car's performance. However, it's an enhancement that must be handled responsibly. Transparency with your insurance provider, such as Admiral Insurance, is non-negotiable. While the process of informing them might sometimes be trying, it is a vital step to ensure you remain legally insured and protected. Always be prepared for potential premium adjustments and policy fees, and ensure you clearly communicate the nature of the modification to your insurer to avoid any misunderstandings.

If you want to read more articles similar to Engine Remapping and Your Car Insurance, you can visit the Insurance category.