18/07/2006

Being involved in a car accident can be a stressful and confusing experience, especially when your vehicle is financed and subsequently declared a 'write-off' by your insurance company. This situation introduces a layer of complexity, as you're not only dealing with the immediate aftermath of a collision but also with financial obligations tied to the vehicle. Understanding who is responsible and how the process works with your insurance provider and lender is crucial to navigating this challenging period smoothly. This article aims to demystify the process, providing clarity on your rights and responsibilities when your financed car is written off.

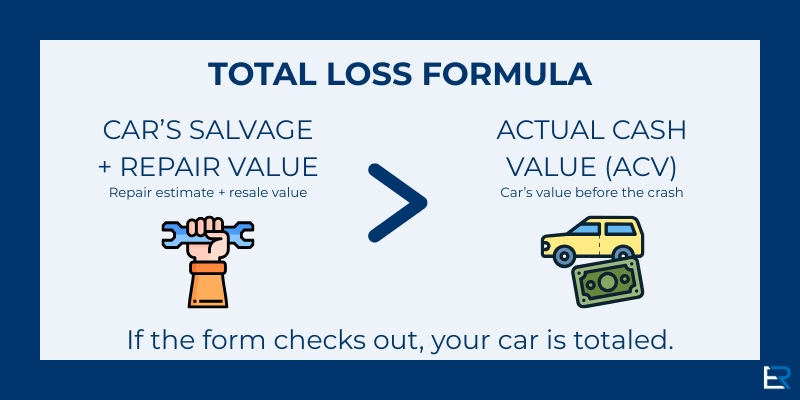

Understanding the 'Write-Off' Process

A 'write-off', also known as a total loss, occurs when the cost to repair your vehicle after an accident exceeds a certain percentage of its pre-accident market value. Insurance companies determine this threshold, and once a vehicle is declared a write-off, they will typically offer you a settlement figure. This figure is usually based on the market value of your car just before the crash, minus any excess you may have on your policy.

The Role of Your Insurance Provider

Your primary point of contact following a car accident is your insurance provider. They will assess the damage to your vehicle and determine if it qualifies as a write-off. Once this decision is made, they will offer you a settlement. It is vital to understand the settlement offer thoroughly. Negotiate if you believe the figure is too low, providing evidence such as comparable vehicle sales data.

The Importance of Informing Your Lender

When you have a financed car that is written off, your lender has a significant interest in the outcome. The car is technically still owned by the lender until the finance agreement is fully settled. Therefore, you must inform your lender about the accident and the subsequent insurance claim as soon as possible. Failure to do so could potentially breach the terms of your finance agreement.

Your lender will outline their specific policies regarding written-off vehicles. They will want to know the status of the insurance claim and the expected settlement amount. This information is crucial for them to determine how the insurance payout will be allocated.

Settling Your Finance Agreement

The most common course of action when your financed car is written off is for the insurance settlement to be used to pay off any outstanding finance. Your insurance company will typically pay the settlement directly to your lender to clear the debt. However, you need to be actively involved in this process.

You will need to contact your lender to inform them of the insurance claim. They will then advise you on the available options. In most cases, the settlement will be used to settle the finance agreement early. This means the loan will be paid off in full, and you will no longer have any financial obligations for that vehicle.

Potential Shortfalls and How to Handle Them

It is important to recognise that finance and insurance companies operate independently. While the insurance payout is intended to cover the cost of your car, it might not always be enough to clear the entire outstanding finance. This can happen if you have negative equity in your car, meaning you owe more on the finance than the car is actually worth.

If the insurance settlement figure leaves a shortfall – meaning the payout is less than the amount you owe on your finance – you will typically be expected to pay the difference. This is where proactive communication with your lender becomes even more critical.

What to do if there's a shortfall:

- Contact your finance company immediately: Discuss the situation with them. They may have options available to help you manage the shortfall.

- Explore payment plans: Your lender might be willing to set up a payment plan for the outstanding amount.

- Consider a new loan: In some cases, you might need to take out a small loan to cover the shortfall.

- Review your insurance policy: Some comprehensive insurance policies include 'gap insurance', which can cover the difference between the insurance payout and the outstanding finance. Check your policy documents carefully.

Continuing the Finance Agreement?

In rare circumstances, some lenders may allow the finance agreement to continue, even if the car is written off. This is highly dependent on the lender's policy and the specific terms of your agreement. If this is an option, it usually means you would continue making payments on the finance, even though you no longer have the vehicle. This is generally not a favourable outcome, and it's crucial to understand why this might be offered and what the implications are.

Your Rights and Responsibilities

It's essential to be aware of your rights and responsibilities throughout this process:

- Right to a Fair Settlement: You have the right to a settlement offer that reflects the market value of your car before the accident.

- Responsibility to Inform: You are responsible for informing both your insurance provider and your lender promptly.

- Responsibility for Shortfalls: Unless you have specific gap insurance, you are responsible for any shortfall between the insurance payout and the outstanding finance.

- Responsibility to Review: You must review all documentation from both your insurance company and your lender carefully.

Frequently Asked Questions

Q1: What if my car is financed and is stolen and not recovered?

The process is very similar to a write-off. Your insurance company will treat it as a total loss. You will receive a settlement, which will then be used to pay off your outstanding finance. Again, inform your lender immediately and be prepared for a potential shortfall.

Q2: Can I keep the written-off car?

Generally, no. Once the insurance company declares a car a write-off and pays out the settlement, they usually take ownership of the vehicle. This is because they will sell it for salvage.

Q3: What if I disagree with the insurance settlement figure?

You can negotiate with your insurance company. Gather evidence of your car's market value, such as advertisements for similar vehicles in your local area. If you still cannot agree, you may wish to seek advice from a consumer rights organisation or a legal professional.

Q4: Does my lender have to accept the insurance payout?

Yes, your lender is obligated to accept the insurance payout as settlement for the financed vehicle, up to the outstanding amount of your loan. They cannot refuse the payment.

Q5: What is 'gap insurance'?

Gap insurance (Guaranteed Asset Protection) is an optional add-on to your car insurance policy. It covers the 'gap' between what your insurance company pays out for a written-off car and the amount you still owe on your finance agreement. It's highly recommended if you have financed your vehicle, especially if you have a substantial loan or have put down a small deposit.

Conclusion

Experiencing a car accident with a financed vehicle can be daunting, but by understanding the roles of your insurance provider and lender, and by communicating proactively, you can navigate the situation effectively. Always prioritise communication with both parties, review your policy documents, and be prepared for potential shortfalls. Being informed is your best defence against further financial stress during an already difficult time.

If you want to read more articles similar to Car Accident Responsibility & Finance, you can visit the Automotive category.