10/09/2004

Navigating the labyrinth of VAT (Value Added Tax) codes in Sage 50 Accounts can often feel like a daunting task for many UK businesses. Applying the correct tax code to each transaction is not just about keeping your books tidy; it's absolutely fundamental for accurate VAT Returns and maintaining compliance with HM Revenue and Customs (HMRC) regulations. A single misapplied code can lead to incorrect VAT calculations, potential penalties, and a significant headache come VAT reporting time.

This guide aims to demystify the process, helping you understand the factors that influence which Sage 50 tax code to use for your sales, purchases, and even bank charges. While the information here is based on the default or recommended codes in Sage 50 Accounts, and every effort has been made to ensure its accuracy, please remember that this is general guidance. Your specific business circumstances, and indeed, any customisations within your Sage software, may necessitate a different approach. Always cross-reference with the latest HMRC VAT guidance or seek professional advice for specific queries.

- Understanding Default Sage 50 Tax Codes

- Key Questions to Ask Before Choosing a Tax Code

- Choosing the Right Code for Sales Transactions

- Choosing the Right Code for Purchase Transactions

- Bank Charges and Interest

- What if You're Not VAT Registered?

- Important Considerations and Disclaimers

- Common Mistakes to Avoid

- Frequently Asked Questions (FAQs)

- Conclusion

Understanding Default Sage 50 Tax Codes

Before diving into transaction types, let's familiarise ourselves with the most commonly used default tax codes within Sage 50 Accounts. These 'T-codes' dictate how VAT is treated on a transaction, including the rate applied and whether it's included in your VAT Return.

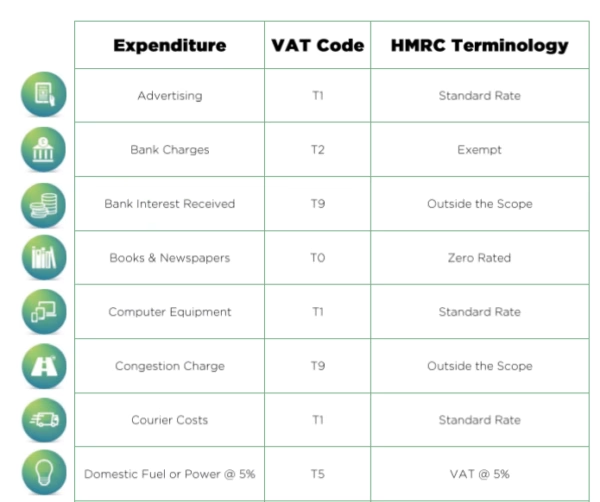

| Sage 50 Tax Code | Default VAT Rate | Description | Common Use Cases |

|---|---|---|---|

| T0 | 0% | Zero Rated | Sales of food (most), books, children's clothes, exports of goods outside the UK. Allows recovery of input VAT. |

| T1 | 20% (Standard) | Standard Rated | The most common code for goods and services subject to the standard VAT rate in the UK. This is your go-to for most everyday transactions. |

| T2 | 0% | Exempt | Transactions that are exempt from VAT, such as insurance, financial services, education, and health services. No VAT is charged, and you cannot recover any input VAT related to these transactions. |

| T5 | 5% (Reduced) | Reduced Rated | Applies to specific goods and services subject to a reduced VAT rate, such as domestic fuel and power, and some renovations. |

| T9 | 0% | Non-Vatable / Outside Scope | Used for transactions that are entirely outside the scope of UK VAT. This includes items like salaries, dividends, grants, or if your business is not VAT registered. |

| T4, T7, T8 | Varies | Historical EU Codes | These codes were traditionally used for EU transactions. Post-Brexit, their usage has significantly changed, and they are often now superseded by T0, T1, or specific import/export procedures. Always verify current HMRC rules. |

It's vital to grasp the distinction between 'Zero Rated' (T0) and 'Exempt' (T2). While both result in no VAT being charged to the customer, a business making zero-rated supplies can still recover input VAT on related purchases, whereas a business making exempt supplies generally cannot. This difference can significantly impact your VAT recovery.

Key Questions to Ask Before Choosing a Tax Code

To accurately determine the correct tax code, consider these fundamental questions for each transaction:

- Is your business VAT registered? If not, almost all your transactions will likely use T9, as you won't be charging or reclaiming VAT.

- What type of transaction is it? Is it a sale (income), a purchase (expenditure), or a bank charge/interest?

- What is the nature of the goods or services? Are they standard-rated, zero-rated, reduced-rated, or exempt from VAT in the UK?

- Where is the customer or supplier located? Are they in the UK, the EU, or the Rest of the World? International transactions have specific VAT rules.

- Is the transaction genuinely 'Outside the Scope of VAT'? This means it falls completely outside the UK VAT system.

Choosing the Right Code for Sales Transactions

Sales transactions represent your income, and getting the VAT right here is paramount for accurate VAT liabilities.

UK Sales

- Most Common Sales (Standard Rated): For the vast majority of goods and services sold within the UK, you will use T1. This applies the current standard VAT rate (currently 20%) to your sales. Examples include selling electronics, consultancy services, or car repair labour.

- Zero-Rated Sales: If you're selling items like most food products, books, or children's clothing within the UK, you'll use T0. Although no VAT is charged to the customer, the sale is still reported on your VAT Return, and you can recover input VAT on related purchases.

- Exempt Sales: For services such as insurance, financial services (e.g., interest on loans), or certain educational services, use T2. No VAT is charged, and these sales are generally not reported in the main boxes of your VAT Return, though they may be required for specific disclosures if you are partially exempt.

International Sales (Post-Brexit Considerations)

The rules for international sales, especially with the EU, have undergone significant changes post-Brexit. It's crucial to stay updated with HMRC guidance.

- Sales of Goods to EU or Rest of World: If you are exporting goods from the UK to customers in the EU or any other country outside the UK, these are generally considered zero-rated exports. You would typically use T0. Ensure you retain proof of export (e.g., shipping documents). The recipient in the destination country will typically be responsible for any import VAT and duties.

- Sales of Services to EU or Rest of World: The VAT treatment of services depends heavily on the 'place of supply' rules. For most business-to-business (B2B) services supplied to customers in the EU or outside the UK, the 'reverse charge' mechanism often applies, meaning the customer accounts for the VAT in their own country. In Sage 50, you would typically use T0 for these services, indicating no UK VAT is charged. For business-to-consumer (B2C) services, UK VAT may apply, or specific destination-based rules may be in play. This area is complex and warrants careful attention to HMRC guidance.

Choosing the Right Code for Purchase Transactions

Purchases represent your expenditure, and applying the correct VAT code here is essential for accurately reclaiming input VAT.

UK Purchases

- Most Common Purchases (Standard Rated): For the majority of goods and services bought from UK suppliers where VAT has been charged, use T1. This allows you to reclaim the input VAT paid. Examples include office supplies, utility bills (if standard rated), or marketing services.

- Zero-Rated Purchases: If you purchase items that are zero-rated in the UK (e.g., most food items, books), you will use T0. While no VAT is charged by the supplier, using T0 correctly records the purchase.

- Exempt Purchases: For services like insurance premiums or certain financial service charges from UK suppliers, use T2. No VAT will have been charged by the supplier, and you cannot reclaim any input VAT on these.

- Non-Vatable / Outside Scope Purchases: For payments that are not subject to VAT at all, such as salaries, dividends, loan repayments, or local authority rates, use T9. These transactions do not appear in your VAT calculations.

International Purchases (Post-Brexit Considerations)

Purchases from abroad, particularly imports, have become more intricate since Brexit.

- Imports of Goods from EU or Rest of World: Goods imported into the UK are subject to UK import VAT. For most businesses, this is now managed through Postponed VAT Accounting (PVA). Under PVA, you record the import VAT on your VAT Return and reclaim it simultaneously, effectively making it VAT neutral for most VAT-registered businesses. In Sage 50, you would typically use T1 for the value of the goods, adjusting your nominal codes to reflect the PVA entries, or use specific import codes (e.g., T20 if configured for PVA) if your Sage setup supports it. The key is to ensure the import VAT is correctly declared and recovered.

- Purchases of Services from EU or Rest of World: For many B2B services purchased from suppliers outside the UK, the 'reverse charge' mechanism applies. This means you, the recipient, are responsible for accounting for the VAT. In Sage 50, you would typically use T0 for the gross value of the service, and then manually adjust your VAT Return (or use a specific Sage code like T20 if configured for reverse charge) to declare both the input and output VAT, making it VAT neutral. This requires careful handling to ensure compliance.

Bank Charges and Interest

Bank charges and interest typically fall under specific VAT categories:

- Bank Interest Received or Paid: This is generally an exempt supply of financial services. You would use T2.

- Standard Bank Charges (e.g., account fees): These are usually also exempt from VAT and would therefore be coded as T2.

- Specific Services (e.g., credit card processing fees for your sales): Some specific banking services may be standard-rated. Always check the VAT breakdown on your bank statements or invoices. If VAT is charged, use T1.

When in doubt, always refer to the specific invoice or statement from your bank to see if VAT has been applied.

What if You're Not VAT Registered?

If your business is not registered for VAT, the process simplifies considerably. You generally won't charge VAT on your sales, nor will you reclaim VAT on your purchases. In Sage 50 Accounts, for nearly all transactions, you would use the T9 (Non-Vatable / Outside Scope) tax code. This ensures that no VAT is calculated or reported on your VAT Return.

The only exception might be if you're making purchases from a supplier who incorrectly charges you VAT. In such cases, you still cannot reclaim it, and you should ideally ask the supplier for a corrected invoice. If you cannot, you would still record it as T9, as you cannot recover the VAT.

Important Considerations and Disclaimers

While this guide provides a solid foundation, remember these crucial points:

- Customised Codes: Your Sage 50 Accounts software might have customised tax codes, or the default rates may have been altered. Always verify your specific setup.

- HMRC Guidance is Paramount: The ultimate authority on VAT rules is HMRC. This article provides general guidance. For specific circumstances, especially complex international trade or unique business models, you should always consult the official HMRC website or seek professional advice from a qualified accountant or tax advisor.

- Regular Review: VAT legislation and rules can change. It's good practice to regularly review your understanding and application of tax codes, especially after budget announcements or significant economic changes.

VAT Disclaimer: This article provides general rather than specific guidance to assist all of our customers. We always do our best to make sure that the information is correct but as it's general guidance, no guarantees can be made concerning its suitability for your particular needs. The information is valid at the time of publishing and is provided without any warranty of any kind, express or implied. You should take professional advice if you require specific guidance on your individual circumstances, for example, to ensure that the results obtained from using our software comply with statutory or regulatory requirements. For VAT, customs and excise and duties enquiries you should call the HM Revenue and Customs (HMRC) National Advice Service Helpline on 0300 200 3700, contact your local HMRC office or visit their website at www.hmrc.gov.uk. In no event will we be liable to you for any direct, indirect, consequential or incidental loss or damage arising out of or in connection with your use of the information provided.

Common Mistakes to Avoid

Even experienced users can fall foul of common VAT coding errors. Being aware of these can save you significant trouble:

- Confusing Zero-Rated (T0) with Exempt (T2): As discussed, this is a frequent error. Remember, T0 allows input VAT recovery, T2 does not. Incorrectly coding an exempt supply as zero-rated could lead to incorrect input VAT claims.

- Incorrectly Applying International VAT Rules: Post-Brexit, international trade rules are more complex. Assuming old EU rules still apply, or misinterpreting import VAT and reverse charge mechanisms, can lead to serious compliance issues and incorrect VAT liabilities. Always double-check HMRC guidance for cross-border transactions.

- Not Updating Codes for Rule Changes: VAT rates and rules can change. Ensure your Sage 50 software and your understanding of the codes are up-to-date with the latest HMRC pronouncements.

- Ignoring the 'Outside the Scope' Category (T9): Not all money movements are subject to VAT. Transactions like salaries, dividends, or inter-company transfers (that aren't actual supplies) should be T9. Incorrectly applying a VAT-bearing code to these can inflate your VAT Return figures.

- Failing to Keep Proper Records: Regardless of the code used, proper documentation (invoices, proof of export, etc.) is crucial to support your VAT treatment of transactions. HMRC can request these at any time.

Frequently Asked Questions (FAQs)

Here are some common questions users have about Sage 50 tax codes and VAT:

What's the difference between T0 (Zero-Rated) and T2 (Exempt)?

Both T0 and T2 result in no VAT being charged on the sale. However, the key difference lies in input VAT recovery. For T0 (zero-rated) supplies, you can still recover input VAT on purchases related to those supplies. For T2 (exempt) supplies, you generally cannot recover input VAT. For example, a bookshop selling zero-rated books (T0) can reclaim VAT on its rent, but an insurance broker selling exempt insurance (T2) usually cannot reclaim VAT on its office supplies.

Can I create new tax codes in Sage 50 Accounts?

Yes, Sage 50 Accounts allows you to create new tax codes or modify existing ones. However, this should only be done with extreme caution and a clear understanding of the VAT implications. Incorrectly setting up a new code can lead to significant errors in your VAT reporting. It's often better to stick to the default codes unless advised otherwise by a professional.

What if I use the wrong tax code on a transaction?

Using the wrong tax code can lead to an incorrect VAT Return. If you underpay VAT, HMRC may charge penalties and interest. If you overpay, you'll be out of pocket. Small errors can often be corrected in a subsequent VAT period, but significant or repeated errors may require a voluntary disclosure to HMRC. Always aim for accuracy from the outset.

How do I deal with imported goods and services from outside the UK?

For imported goods, the most common method for VAT-registered businesses is Postponed VAT Accounting (PVA). This allows you to declare and recover import VAT on the same VAT Return, improving cash flow. In Sage 50, you'll typically record the full value of the import using T1 (or a specific import code if configured) and ensure the PVA figures are correctly reflected. For imported services (B2B), the reverse charge mechanism often applies, where you account for both the input and output VAT. These are complex areas, and detailed HMRC guidance or professional advice is essential.

Where can I find the most up-to-date HMRC VAT information?

The official HMRC website (www.hmrc.gov.uk) is the definitive source for current VAT guidance. Look for sections on 'VAT rates', 'VAT place of supply', and 'importing and exporting'. You can also call the HMRC National Advice Service Helpline on 0300 200 3700 for direct assistance.

Conclusion

Mastering VAT codes in Sage 50 Accounts is a cornerstone of accurate financial management and compliance for any VAT-registered business in the UK. By understanding the default codes, asking the right questions about each transaction, and diligently applying the correct code, you can ensure your VAT Returns are precise and avoid potential pitfalls. While this guide provides a robust framework, the dynamic nature of VAT rules, especially concerning international trade, means vigilance and a willingness to consult HMRC or a tax professional for specific advice are always your best defence. Invest time in understanding these codes, and you'll build a solid foundation for your business's financial health.

If you want to read more articles similar to Mastering VAT Codes in Sage 50 Accounts, you can visit the Automotive category.