03/04/2012

Vehicle Excise Duty (VED), often colloquially known as ‘road tax’, ‘car tax’, or ‘road fund licence’, is a mandatory UK-wide tax that grants motorists the legal right to drive or park a vehicle on public roads. Its origins trace back to the early 20th century, but a myriad of reforms over the decades has transformed it into a system that many find perplexing. Fear not, for this comprehensive guide aims to demystify VED, detailing when and why the tax bands shifted, how much you can expect to pay, the payment process, and what actions are required when buying, selling, or taking a vehicle off the road.

When acquiring a new or used vehicle in the UK, it is highly probable that you will be liable for VED. While certain exemptions exist, these have become increasingly rare. Historically, zero-emission vehicles, such as electric cars, enjoyed exemption, but this significant change is set to conclude in April 2025. Currently, only classic cars aged over 40 years (meaning those first registered before January 1985) and vehicles specifically adapted for, or used by, disabled individuals remain exempt from the annual charge. The amount of VED payable is primarily influenced by the vehicle's carbon emissions, although the evolving landscape of vehicle efficiency has prompted the government to frequently adjust tax bands to maintain revenue streams.

A Brief History of UK VED Changes

The journey of VED from a simple engine-size-based tax to its current, more complex emissions-focused model, is marked by several pivotal reforms. Understanding these changes is key to comprehending the current system.

Pre-2001: The Engine Size Era

Before 2001, VED was relatively straightforward, primarily based on engine size. Vehicles with engines up to 1549cc (1.5 litres) paid one rate, and those over 1549cc paid a higher rate. This system was simple but did not incentivise the production or purchase of more environmentally friendly vehicles, as a large, inefficient car could pay the same as a smaller, more efficient one if they both exceeded the 1549cc threshold.

2001-2017: The Dawn of CO2-Based Taxation

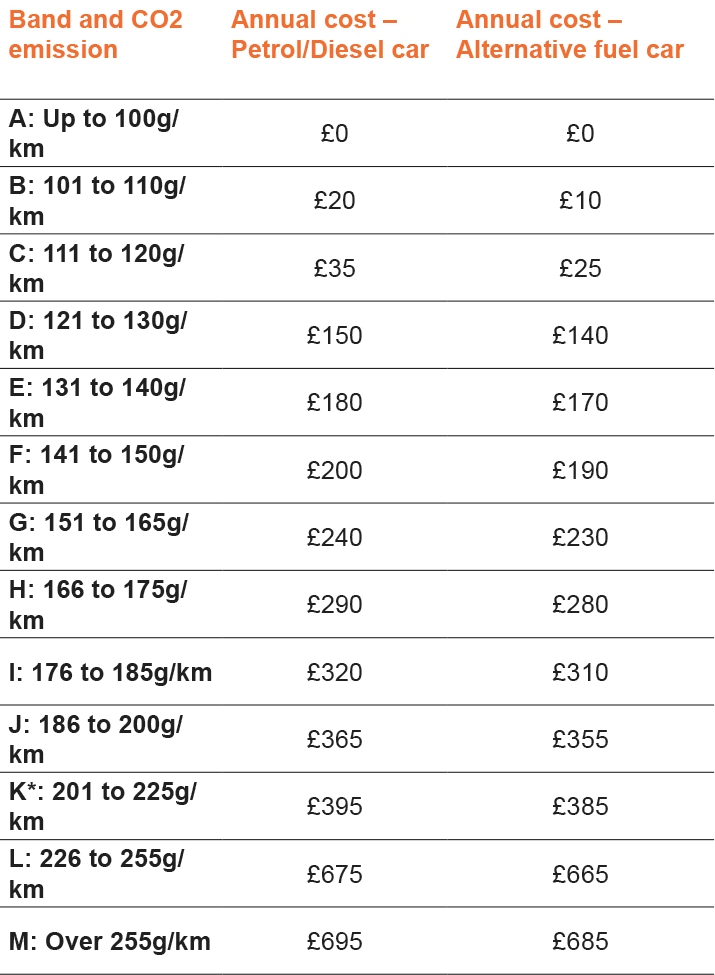

A significant overhaul occurred on 1st March 2001, when VED bands were restructured to primarily depend on a car's CO2 emissions. This marked a deliberate shift towards encouraging lower-emission vehicles. Cars were categorised into different bands (A to M) based on their CO2 output in grams per kilometre (g/km), with lower emissions attracting lower VED rates. This system applied to new cars registered from this date onwards, while older cars continued under the engine-size system or older emissions-based rules depending on their registration date.

Within this period, further tweaks were made. For instance, from April 2010, the first-year VED rate (often referred to as the 'showroom tax') was introduced, which was significantly higher for the most polluting vehicles. This was designed to further discourage the purchase of high-emission cars. The rates for subsequent years remained lower, based on the specific CO2 band.

April 2017: The Major Reform

Perhaps the most impactful change to VED in recent memory came into effect on April 2017. This reform was driven by the government's recognition that as cars became increasingly efficient, more vehicles were falling into the lowest CO2 bands, leading to a projected shortfall in VED revenue. The new system introduced a flat-rate standard charge for most vehicles after their first year, regardless of their CO2 emissions, with only zero-emission vehicles retaining an exemption.

Key elements of the 2017 reform included:

- First-Year Rate: Still based on CO2 emissions, this rate is paid for the first 12 months from new registration. Higher emitters pay more.

- Standard Rate: From the second year onwards, most cars pay a flat standard rate. This rate applies to petrol and diesel cars.

- Alternative Fuel Discount: A small discount was introduced for vehicles running on alternative fuels like LPG or natural gas, although this has since been removed.

- Premium Car Supplement: A new 'expensive car supplement' was introduced for vehicles with a list price of over £40,000. This additional charge is applied for five years from the second year of registration, on top of the standard rate.

- Zero-Emission Exemption: Pure electric vehicles and other zero-emission cars continued to be exempt from VED under the 2017 rules.

This radical shift meant that many popular, low-emission petrol and diesel cars, which previously benefited from very low or even zero VED, now faced the standard annual charge from their second year of registration. The intention was to ensure that all drivers contributed to the road network, rather than just those with older or higher-emission vehicles.

April 2025: End of EV Exemption

The latest significant change, as highlighted, is the removal of the VED exemption for zero-emission vehicles, including electric cars, from April 2025. This means that new electric cars registered from this date will pay the same first-year rate as a petrol or diesel car with 1-50g/km CO2 emissions. From their second year onwards, they will pay the standard rate. Furthermore, electric cars registered between 1st April 2017 and 31st March 2025 will begin paying the standard rate from April 2025. Electric cars first registered before 1st April 2017 will also transition to paying the standard rate from April 2025. The premium car supplement will also apply to electric vehicles with a list price over £40,000 from April 2025.

Current VED Rates (Post-April 2017, and looking to 2025)

Here’s a breakdown of the VED rates for cars registered after 1st April 2017. Rates are subject to annual inflationary increases, so these figures are illustrative of the structure.

First-Year VED Rates (based on CO2 emissions)

| CO2 Emissions (g/km) | First-Year Rate (Petrol/Diesel) |

|---|---|

| 0 | £0 |

| 1-50 | £10 |

| 51-75 | £30 |

| 76-90 | £130 |

| 91-100 | £160 |

| 101-110 | £180 |

| 111-130 | £220 |

| 131-150 | £270 |

| 151-170 | £675 |

| 171-190 | £1,060 |

| 191-225 | £1,665 |

| 226-255 | £2,365 |

| Over 255 | £2,745 |

Standard VED Rates (from second year onwards)

| Vehicle Type | Annual Standard Rate | Premium Car Supplement (if applicable) |

|---|---|---|

| Petrol/Diesel Cars | £190 (approx.) | +£410 (approx.) for 5 years |

| Alternative Fuel Cars (e.g., Hybrid) | £180 (approx.) | +£410 (approx.) for 5 years |

| Electric Cars (from April 2025) | £190 (approx.) | +£410 (approx.) for 5 years |

Note: The premium car supplement applies to cars with a list price of over £40,000 for five years, starting from the second year of registration. After five years, the standard rate applies.

How to Pay Your Road Tax

Paying your VED is a straightforward process, primarily managed by the Driver and Vehicle Licensing Agency (DVLA). You will need your V5C registration document (logbook) or a V11 reminder letter.

- Online: The quickest and easiest method is via the official GOV.UK website. You can pay using a credit or debit card.

- By Phone: You can call the DVLA vehicle enquiry line.

- At a Post Office: Many Post Office branches offer the service, but you will need your V5C or V11 and a valid MOT certificate (if applicable).

- Direct Debit: For convenience, you can set up a Direct Debit to pay annually, every six months, or monthly. This ensures you don't miss a payment and avoid penalties. Paying monthly or every six months incurs a small surcharge.

It's crucial to remember that VED is the responsibility of the registered keeper of the vehicle. You will receive a V11 reminder when your VED is due for renewal.

What Happens When You Sell or Buy a Car?

The VED system does not automatically transfer when a car changes ownership. This is a common point of confusion.

- Selling Your Car: When you sell your vehicle, you must notify the DVLA immediately. The VED paid for that vehicle is not transferable to the new owner. You will automatically receive a refund for any full months of VED remaining on the vehicle. The new owner must tax the vehicle themselves before they can legally drive it.

- Buying a Car: As a buyer, it is your responsibility to tax the vehicle before you drive it away. You can do this online using the 11-digit reference number from the new keeper slip (V5C/2) provided by the seller.

Taking a Car Off the Road (SORN)

If you intend to keep your vehicle off public roads – for example, if it's undergoing long-term repairs, being stored, or is a classic car not in use – you must declare a Statutory Off Road Notification (SORN) to the DVLA. A SORN means you don't have to pay VED for that period. It's a legal declaration, and failure to have either valid VED or a SORN can result in significant fines. Once a SORN is in place, you cannot drive or park the vehicle on a public road until it is taxed again.

Consequences of Not Paying VED

Driving or keeping an untaxed vehicle on a public road is a serious offence. The DVLA uses automated number plate recognition (ANPR) cameras to detect untaxed vehicles. If caught, you could face:

- An immediate fine (typically £80)

- Your vehicle being clamped or impounded, incurring release fees and storage charges

- Prosecution, leading to a court fine of up to £1,000

It is paramount to ensure your VED is always up to date, or that a valid SORN is in place if the vehicle is not in use on public roads.

Frequently Asked Questions About VED

Q1: Can I still pay VED for 6 months?

Yes, you can pay VED annually, or in 6-monthly or monthly instalments via Direct Debit. Be aware that paying in instalments typically incurs a small surcharge, making the annual payment slightly cheaper overall.

Q2: Do classic cars still need VED?

Yes, classic cars are exempt from VED once they reach 40 years of age. This exemption rolls forward, meaning a car becomes exempt on 1st April each year if it was built more than 40 years ago. Even if exempt, you still need to apply for VED (at a zero rate) or declare a SORN.

Q3: What if I forget to renew my VED?

The DVLA sends out V11 reminder letters, but ultimately, it is your responsibility to ensure your vehicle is taxed. If you forget, you risk being caught by ANPR cameras and facing the penalties mentioned above. You can check your vehicle's VED status online at any time using its registration number.

Q4: Does the MOT affect VED?

Yes, for vehicles that require an MOT, you cannot renew your VED without a valid MOT certificate. The DVLA's system will automatically check if your vehicle has a current MOT pass.

Q5: How do hybrid cars fit into the VED system?

Hybrid cars, like petrol and diesel vehicles, are taxed based on their CO2 emissions for the first year. From the second year onwards, they pay the standard rate. Prior to the 2017 changes, many hybrids with low CO2 emissions benefited from very low VED, but now generally pay the standard rate, albeit with a small 'alternative fuel' discount for qualifying vehicles. However, with the removal of this discount and the flattening of rates, the distinction is minimal for most.

Q6: Will electric cars be more expensive to tax after April 2025?

Yes, from April 2025, electric cars will no longer be exempt from VED. They will pay the standard rate, and new electric cars will also pay a first-year rate. Those with a list price over £40,000 will also be subject to the premium car supplement for five years. This change means owning an EV will incur the same VED costs as many petrol/diesel cars.

Understanding the nuances of VED is essential for any UK motorist. While the system has become more complex with its various changes over the decades, the core principle remains: if your vehicle is on a public road, it must be taxed. Staying informed about the latest rates and regulations, especially with the upcoming changes for electric vehicles, will help you avoid unnecessary fines and ensure you remain compliant with the law.

If you want to read more articles similar to UK Road Tax: Navigating VED Band Changes, you can visit the Automotive category.