02/05/2017

Can You Buy a Car After a Lease is Up? A Comprehensive Guide

The allure of driving a new car every few years, often with lower monthly payments, has propelled vehicle leasing into mainstream popularity. Reports indicate a significant surge in lease volumes, with consumers drawn to the financial benefits. However, as with any significant financial agreement, understanding the nuances of a lease contract is paramount. One of the most common questions arising for those new to leasing is: what happens when the lease term concludes? Specifically, can you actually purchase the car you've been driving?

The short answer is a resounding yes. Most lease agreements offer the option to purchase the vehicle at the end of the term. This is often referred to as the 'buyout option'. However, the decision to lease, and subsequently to buy, involves understanding your responsibilities, the potential benefits, and the drawbacks.

Understanding What Leasing Entails

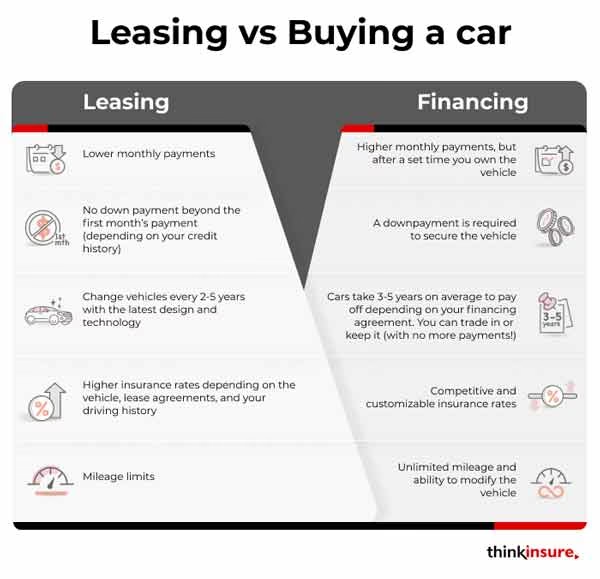

When you lease a vehicle, you are essentially entering into a long-term rental agreement. You do not own the car; instead, you are paying for the depreciation of the vehicle over a set period, typically 36 months. During this time, you'll make regular monthly payments, and your contract will outline your responsibilities regarding maintenance and repairs. It's crucial to remember that ownership remains with the leasing company until you exercise your buyout option.

Know Your Responsibilities: Maintenance and Beyond

A critical aspect of any lease agreement is understanding your responsibilities. Failing to do so can lead to unexpected charges at the end of the lease term. Always scrutinise your lease contract carefully. Pay close attention to clauses detailing mileage limits. Exceeding your agreed-upon annual mileage (commonly 10,000, 12,000, or 15,000 miles) will result in per-mile charges, which can add up quickly.

Maintenance is another key area. Some lease agreements may include certain maintenance services within the warranty plan. This can cover routine services like oil changes and tire rotations. However, if such a plan isn't opted into, or if it's not comprehensive, the responsibility for all maintenance and repairs will fall on you. It's vital to clarify what is and isn't covered before signing. A well-maintained vehicle not only ensures reliability but also impacts the vehicle's residual value, which is a factor in the buyout price.

Review the Pros to Leasing

Leasing offers several compelling advantages:

- Lower Monthly Payments: Typically, lease payments are lower than loan payments for the same vehicle because you're only paying for the depreciation during the lease term, not the full purchase price.

- Drive Newer Cars: Leasing allows you to drive a new car every few years, benefiting from the latest technology, safety features, and design.

- Manufacturer's Warranty: Most leased vehicles are covered by the manufacturer's warranty throughout the lease term. This means most repairs will be covered, reducing your out-of-pocket expenses for mechanical issues.

- Reduced Repair Costs: Newer vehicles, being less prone to breakdowns, generally require fewer repairs than older or used cars.

- No Resale Hassle: At the end of the lease, you can simply return the car. You don't have to worry about the complexities of selling or trading in a vehicle, which can be time-consuming and stressful.

Examine the Cons to Leasing

Despite the benefits, leasing also has its drawbacks:

- Mileage Restrictions: The most significant con is the strict mileage limit. If your driving habits exceed the agreed-upon limit, you'll face substantial penalties.

- Wear and Tear Charges: Beyond normal wear and tear, excessive damage or neglect can incur additional charges when you return the vehicle. This includes things like significant dents, torn upholstery, or bald tyres.

- No Ownership Equity: You don't build equity in the vehicle as you would with a loan. At the end of the lease, if you haven't purchased the car, you have nothing to show for the payments you've made.

- Early Termination Fees: Ending a lease early can be very expensive, often involving significant penalties and fees.

- Customisation Limitations: You are generally not permitted to make significant modifications to a leased vehicle.

Your Options at the End of the Lease

Once your lease term is nearing its end, you'll typically have three main options:

| Option | Description | Considerations |

|---|---|---|

| Purchase the Vehicle | Exercise your buyout option as stipulated in your lease contract. This allows you to become the outright owner of the car. | Compare the buyout price against the current market value of the car. You may need to secure financing if you don't have the cash available. Check for any remaining warranty coverage. |

| Return the Vehicle | Simply hand the keys back to the dealership. Ensure the car is in good condition, within mileage limits, and all scheduled maintenance is up to date to avoid excess charges. | You will likely need to lease or purchase a new vehicle if you require transportation. Be prepared for a potential end-of-lease inspection. |

| Trade-In the Vehicle | Some dealers may allow you to trade in your leased vehicle towards the purchase or lease of another car, even if you haven't officially bought it out. | This is less common and depends heavily on the leasing company's policies and the car's market value. The dealer essentially buys out the lease on your behalf. |

The Buyout Option: Is it Worth It?

Deciding whether to buy out your leased car involves a bit of homework. Your lease agreement will specify a residual value, which is the predicted value of the car at the end of the lease term. This residual value, plus any applicable taxes and fees, forms your buyout price.

To determine if buying out is financially sound, you should:

- Research Market Value: Check reputable sources like Kelley Blue Book (KBB) or Edmunds to see what similar used cars are selling for in your area.

- Assess Vehicle Condition: Honestly evaluate the car's condition. Has it been well-maintained? Are there any significant cosmetic or mechanical issues?

- Factor in Remaining Costs: Consider if any repairs are needed immediately after purchase, or if you'll need to purchase an extended warranty.

If the buyout price is significantly lower than the car's current market value, and the car is in good condition, purchasing it can be a smart move. You'll own a car you're familiar with, likely in good condition, and potentially at a good price.

Returning the Vehicle: Avoiding Penalties

If you choose to return the car, meticulous preparation is key to avoiding unexpected costs:

- Regular Maintenance: Ensure all scheduled maintenance outlined in your lease contract has been performed and documented. Keep your service records.

- Address Minor Damage: Fix any minor dents, scratches, or interior damage that goes beyond normal wear and tear. Small repairs can be much cheaper than the penalties charged by the leasing company.

- Tyre Check: Ensure your tyres have adequate tread depth according to the lease agreement.

- Clean Thoroughly: A deep clean, both inside and out, can make a positive impression during the final inspection.

- Understand the Inspection Process: Familiarise yourself with the leasing company's end-of-lease inspection checklist.

Frequently Asked Questions

Q1: Can I negotiate the buyout price of my leased car?

Generally, the buyout price is set in the lease contract and is not negotiable. However, it's always worth asking your dealership if there's any flexibility, especially if market conditions have changed significantly.

Q2: What if I go over my mileage limit? Will that affect my ability to buy the car?

Going over your mileage limit typically incurs per-mile charges when you return the vehicle. It usually doesn't prevent you from buying the car, but those excess mileage fees will be added to your final bill if you don't buy it out.

Q3: Do I need to get financing before I decide to buy out my lease?

Not necessarily. You can discuss financing options with your dealership, or you can seek pre-approval from your bank or a credit union to compare rates.

Q4: What happens if the car's market value is higher than the buyout price?

This is an ideal scenario! You've found a great deal. You can purchase the car and then potentially sell it privately for a profit, or trade it in for more than you paid for the buyout.

Q5: Can I lease a car and then buy it out immediately?

While technically possible, it's usually not financially advantageous. Lease contracts are structured assuming you'll use the car for the lease term. Early buyouts might incur penalties or not reflect the best financial outcome.

In conclusion, the ability to purchase a car after your lease term is a standard and often beneficial option. By understanding your lease agreement, your responsibilities, and by doing your due diligence on the vehicle's value, you can make an informed decision that best suits your needs and financial goals.

If you want to read more articles similar to Leasing a Car: Your Options at the End, you can visit the Automotive category.