31/05/2019

- Understanding the Surge in Car Insurance Premiums

- The Root Causes: Why Are Premiums So High?

- Is This a Temporary Blip or a Long-Term Trend?

- Factors Influencing Your Premium

- The Impact of Technology and Electrification

- Consumer Strategies for Lower Premiums

- The Dealer's Perspective and SMART Insurance

- Regulatory Scrutiny and Future Outlook

- Frequently Asked Questions

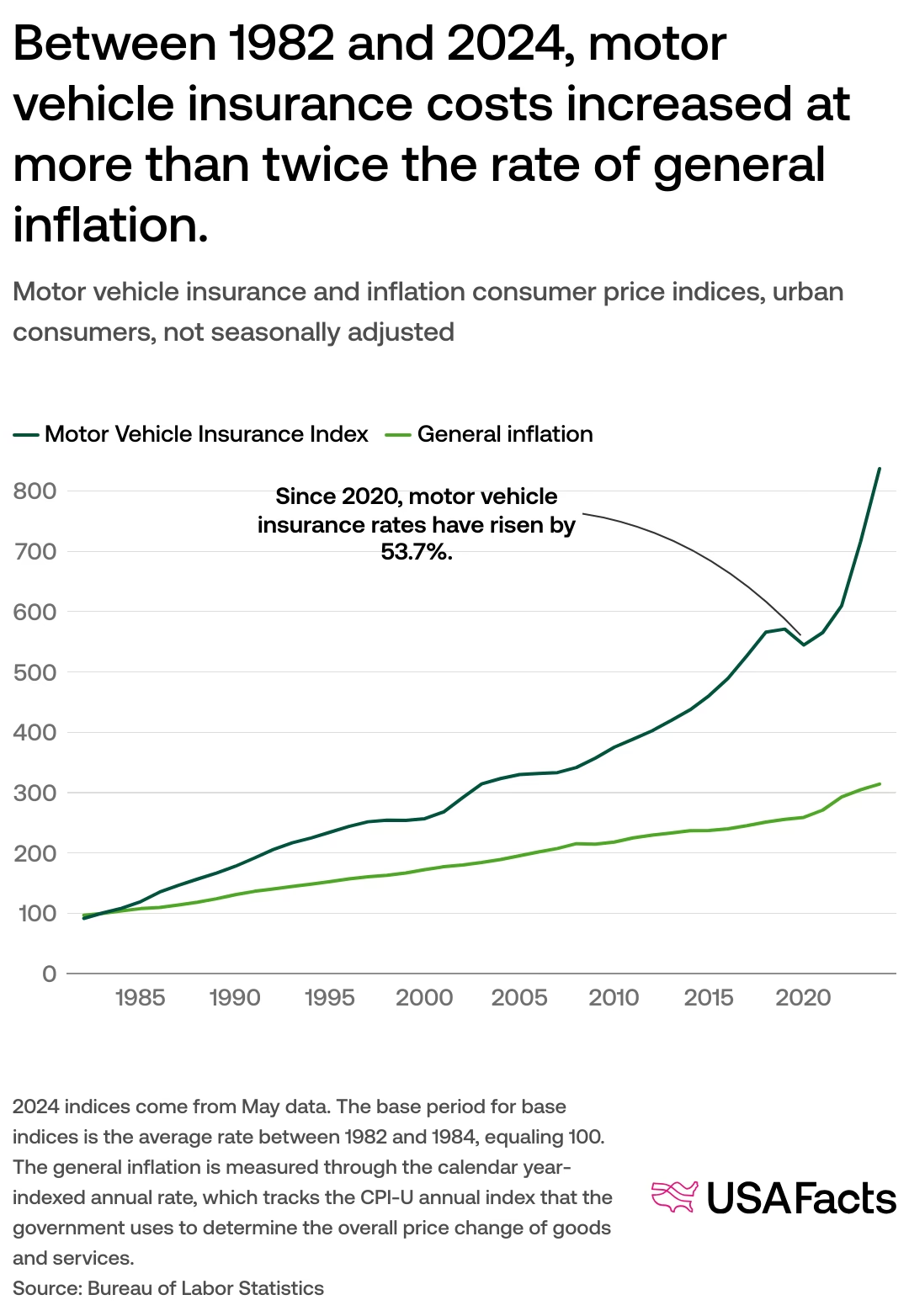

In 2024, many motorists across the UK have been left bewildered by the significant increases in their car insurance premiums. The cost of protecting your vehicle against the unexpected has become a substantial financial burden for countless individuals. Reports from industry bodies like the Association of British Insurers (ABI) and data from consumer analysts consistently highlight a steep upward trend. For instance, private fully comprehensive car insurance premiums saw a staggering 29% rise in the latter half of last year, reaching an average of £561. More alarming still, some analyses indicate an even more dramatic 61% jump in premiums over a single year. This surge has not gone unnoticed, with the Financial Ombudsman Service reporting a five-year high in motor insurance complaints. While inflation's grip on the wider economy is beginning to loosen, its impact on car insurance costs appears to be a lagging effect, creating considerable challenges for drivers and the automotive industry alike. In some extreme cases, certain car models are becoming virtually uninsurable due to their prohibitive costs.

Several interconnected factors are contributing to this sustained increase in car insurance costs. As Tom Banks, Car Spokesperson for Go.Compare, explains, “Car insurance premiums have been increasing for some time... the cost of car insurance had risen by 35% between Q2 2022 and Q4 2023”. While recent figures for 2024 show a slight dip to an average of £447, many drivers are still paying considerably more than a few years ago. The primary drivers behind these escalating costs are widely attributed to the soaring expenses associated with replacement parts and labour, coupled with the pervasive impact of inflation.

James Finucane, Senior Economist at the Swiss Re Institute, elaborates on this point, stating, “The rise in car insurance prices is a lagged response to the inflation surge that affected car prices and repair costs. Inflation filtered through into insurance claims costs and caused a big jump in car insurers’ underwriting losses. Price rises today reflect insurers’ attempts to repair results and return to normal profit levels.” Essentially, insurers are still recalibrating their pricing to account for the higher costs they incurred due to past inflation, aiming to restore profitability.

Louise Thomas, a motor insurance expert at Confused.com, concurs that insurers are facing increased outlays. She also highlights additional contributing factors:

- Increased Claim Costs: Claims are simply costing insurers more to cover.

- Inflationary Impact on Parts and Labour: The general rise in prices directly affects the cost of vehicle components and the wages of mechanics.

- Advanced Vehicle Technology: Modern cars are equipped with increasingly sophisticated technology, such as complex sensor systems and infotainment units. Repairing or replacing these components is more costly and time-consuming.

- Higher Risk of Accidents: With more vehicles on the road compared to the pandemic period, the overall risk of accidents and subsequent claims has increased. This naturally leads to insurers having to pay out for more incidents.

Is This a Temporary Blip or a Long-Term Trend?

The crucial question for consumers is whether these price hikes are a temporary anomaly or the beginning of a sustained trend. While predicting the future with certainty is impossible, experts suggest that a significant drop in premiums is unlikely in the immediate future, though some stabilisation might be on the horizon.

Banks from Go.Compare suggests, “While we can’t predict the future of pricing, it’s unlikely that the landscape will change overnight and it may be a while before we see premiums decreasing. It’s good news to see that, according to the ABI, these increases are stabilising…” He stresses the importance of shopping around at renewal, as premium prices can fluctuate significantly from one year to the next.

Finucane offers a similar outlook, anticipating that “car insurance prices to start stabilising now that used car prices are declining and repair costs are likely to decelerate. This will slow the increase in claims costs. As profitability is restored, competition will contribute to lower price gains.”

However, not everyone shares this optimistic view. Rocio Concha, Director of Policy and Advocacy at Which?, points out, “While it’s encouraging to see the price of premiums steadying, they still remain eye-wateringly high and prohibitively expensive for many drivers. It won’t be lost on motorists that premiums increased by a quarter in 2023 compared to 2022.”

Insurers use a multitude of factors to calculate your car insurance premium, essentially assessing the risk you pose. These include:

| Factor | Impact on Premium | Explanation |

|---|---|---|

| Driver's Age | Higher for younger drivers | Younger drivers (especially under 25) statistically have a higher incidence of accidents. |

| Driving History | Higher for drivers with claims/convictions | A history of claims, penalty points, or convictions indicates a higher risk. |

| Location (Postcode) | Varies significantly | Postcodes with higher rates of theft, vandalism, or accidents can lead to higher premiums. |

| Vehicle Type & Value | Varies | More expensive cars, or those in higher insurance groups (based on repair costs, performance, parts cost), typically cost more to insure. |

| Annual Mileage | Higher for higher mileage | More time spent on the road increases the likelihood of an accident. However, excessively low mileage can also be flagged as a potential risk. |

| Occupation | Varies | Certain occupations may be statistically linked to higher or lower risk profiles. |

| No Claims Discount (NCD) | Lower for fewer years of NCD | A proven track record of claim-free driving earns discounts. |

| Voluntary Excess | Higher for lower voluntary excess | Choosing to pay more towards a claim (voluntary excess) reduces your premium. |

| Vehicle Security | Lower for enhanced security | Features like alarms, immobilisers, or parking in secure locations can reduce premiums. |

| Advanced Driver Assistance Systems (ADAS) | Can vary; potentially lower for safety features | While ADAS improves safety, the cost of repairing these systems can increase premiums. |

The Impact of Technology and Electrification

The automotive landscape is undergoing a rapid transformation, with significant implications for insurance. Modern vehicles are increasingly equipped with sophisticated technologies, including Advanced Driver Assistance Systems (ADAS) like adaptive cruise control, lane-keeping assist, and automatic emergency braking. While these systems enhance safety, they also drive up repair costs. Even minor incidents can necessitate the replacement of expensive sensors and recalibration, adding to the insurer's payout.

Furthermore, the shift towards electric vehicles (EVs) introduces new risk profiles. EVs often have higher initial purchase prices, and their repair processes can be more complex and costly due to integrated battery systems and specialised components. Their rapid acceleration can also contribute to a higher accident probability. As Finucane notes, “Cars are becoming more complicated – and expensive – to fix.”

Despite the challenging market, consumers can adopt several strategies to try and mitigate the rising cost of car insurance:

- Shop Around: This remains the golden rule. Never auto-renew without comparing quotes from multiple insurers. Comparison websites are a good starting point, but also check direct insurers. Even loyal customers can find significant savings by switching. Data shows that drivers who switched insurers after receiving a renewal quote saved an average of £90.

- Pay Annually: If financially feasible, paying your premium in one annual instalment can often be cheaper than monthly payments, as insurers typically add interest for spreading the cost. However, be mindful that this option may not be accessible for all budgets.

- Increase Voluntary Excess: By agreeing to pay a higher amount towards any claim, you can reduce your overall premium. However, ensure the voluntary excess is an amount you can comfortably afford to pay if you need to make a claim.

- Enhance Vehicle Security: Installing an advanced car alarm, an immobiliser, or consistently parking in a secure garage or well-lit area can demonstrate a lower risk of theft to insurers, potentially leading to a reduced premium.

- Review Your Mileage: Be accurate about your annual mileage. While high mileage increases risk, very low mileage might also be viewed with suspicion. Ensure your declared mileage reflects your actual usage.

- Protect Your No-Claims Bonus (NCB): While protecting your NCB allows you to keep your discount even after a claim, it means you'll have to pay for minor damage yourself. With rising used car values, this can sometimes be a viable option for small repairs.

- Consider Telematics (Black Box Insurance): For careful drivers, particularly younger ones, a telematics device can monitor driving behaviour and potentially lead to lower premiums if you demonstrate safe driving habits.

The Dealer's Perspective and SMART Insurance

The current economic climate also presents challenges for car dealerships. Mike Edwards, Chief Sales and Marketing Officer at AutoProtect Group, highlights the desire for dealers to streamline the car-buying process. He notes the growing appeal of SMART insurance (Servicing, Maintenance, and Repair) products, which can help fix minor damage, maximise part-exchange values, and protect a customer's NCB. This proactive approach can enhance customer satisfaction and simplify the sales process.

Regulatory Scrutiny and Future Outlook

Concerns have been raised about the fairness of pricing, particularly regarding the interest charged on monthly payments. Which? has called for greater regulatory guidance to ensure that insurers are not exploiting customers by charging excessive interest rates on instalment plans. The regulator is urged to act swiftly to address these practices.

Looking ahead, while the current situation is challenging, the expectation is that as inflation continues to subside and the costs for insurers begin to stabilise, market competition will play a greater role in bringing down premiums. However, the ongoing evolution of vehicle technology and the transition to electric vehicles mean that the risk landscape for insurers will continue to change, potentially influencing future pricing models.

Frequently Asked Questions

Q1: Why has my car insurance gone up so much recently?

Increases are primarily due to rising costs for insurers, driven by inflation affecting repair parts and labour, as well as more complex vehicle technology requiring expensive repairs. Higher accident frequency also plays a role.

Q2: Will car insurance prices come down soon?

Experts predict that prices may start to stabilise as inflation eases and used car prices decrease. However, a significant drop is not expected immediately, and premiums may take time to reflect these stabilising costs.

Q3: What is the biggest factor affecting my car insurance premium?

While many factors are considered, the cost of claims (both frequency and severity) is the main driver. This is influenced by repair costs, accident rates, and the complexity of vehicle technology.

Q4: How can I get cheaper car insurance?

Key strategies include shopping around for quotes, considering an annual payment, increasing your voluntary excess, enhancing vehicle security, and accurately declaring your mileage. Protecting your No Claims Bonus can also help long-term.

Q5: Are electric vehicles (EVs) more expensive to insure?

EVs can sometimes be more expensive to insure due to their higher initial purchase price, the cost of battery repairs or replacement, and potentially more complex repair processes compared to traditional internal combustion engine vehicles.

If you want to read more articles similar to Car Insurance Costs Explained, you can visit the Automotive category.