02/07/2002

Navigating the complexities of UK road traffic legislation can feel like a daunting task for any vehicle owner or driver. Among the many statutes governing our highways, the Road Traffic Act 1988 stands as a cornerstone, with various sections dictating responsibilities and ensuring public safety. One such pivotal section is Section 144A, which specifically addresses the critical issue of vehicle insurance. This article delves into the intricacies of Section 144A, aiming to provide a comprehensive understanding of its requirements, the reasons behind its implementation, and the consequences of failing to comply. Whether you're a seasoned motorist or new to the road, grasping the essence of this law is paramount for responsible vehicle ownership and to avoid potentially severe penalties.

- Understanding Section 144A: The Core Requirement

- Key Terms and Concepts

- The Purpose Behind Section 144A

- What is Required Under Section 144A?

- Who Must Comply?

- What Vehicles are Covered?

- Penalties for Non-Compliance

- Exemptions and Special Cases

- Ensuring Compliance with Section 144A

- Frequently Asked Questions

Understanding Section 144A: The Core Requirement

At its heart, Section 144A of the Road Traffic Act 1988 mandates that all motor vehicles used or kept on public roads in the United Kingdom must have valid insurance. This isn't a suggestion; it's a legal obligation designed to protect all road users. The minimum level of insurance required is third-party insurance. This means that the policy must cover liability for any personal injuries sustained by other people, or damage caused to their property or vehicles, in the event of an accident where your vehicle is involved. The fundamental aim is to ensure that victims of road traffic accidents are not left without recourse for compensation, thereby promoting a safer and more equitable road network.

The scope of Section 144A is broad, encompassing virtually all motor vehicles that operate on public roads. This includes:

- Cars

- Motorcycles

- Commercial vehicles (vans, lorries, etc.)

- Buses and taxis

- Even vehicles that are temporarily in use or only used seasonally, provided they are kept on a public road.

The law applies equally to private individuals and commercial entities operating fleets of vehicles. The principle of Continuous Insurance Enforcement (CIE) is central to Section 144A. This means that a vehicle must remain insured at all times it is kept on a public road, even if it is not being actively driven. The only permissible exception is when a vehicle has been officially declared off the road through a Statutory Off-Road Notification (SORN).

Key Terms and Concepts

To fully grasp Section 144A, understanding a few key terms is essential:

Third-Party Insurance: This is the minimum level of cover required by law. It protects against claims made by others for damage to their property or for personal injury they suffer as a result of an accident involving your vehicle. It does not cover damage to your own vehicle.

Certificate of Insurance: This is the legal document that serves as proof that your vehicle is insured. It must be carried by the driver and presented to law enforcement officers upon request. Failure to produce a valid certificate can lead to penalties.

Continuous Insurance Enforcement (CIE): This is the principle that vehicles must be insured at all times when kept on a public road. The DVLA uses automated record checks to identify uninsured vehicles, making it crucial to maintain continuous cover.

Statutory Off-Road Notification (SORN): If you are not using your vehicle on public roads and intend to keep it off the road, you must notify the DVLA by submitting a SORN. This exempts the vehicle from the insurance requirement. A SORN is typically declared when a vehicle is being stored, repaired off-road, or awaiting disposal. It is also relevant if the vehicle is not taxed or is to be broken down for parts before scrapping.

The Purpose Behind Section 144A

The legislation behind Section 144A serves several vital purposes aimed at improving the overall safety and fairness of the UK's road network:

- Enhancing Road Safety: By ensuring all vehicles are insured, the Act aims to reduce the number of accidents caused by uninsured drivers who may be less inclined to adhere to safe driving practices. It encourages a culture of responsibility among vehicle owners.

- Protecting Accident Victims: This is perhaps the most critical objective. When an accident occurs, especially one involving serious injury or significant damage, victims need assurance that they can receive fair compensation. Section 144A guarantees that there is an insurance provider to cover these costs, preventing victims from suffering financial hardship due to the uninsured status of another driver.

- Reducing Financial Burden on the Government: Accidents involving uninsured drivers can place a considerable strain on public resources. If victims cannot claim compensation from an insurer, they may turn to government schemes or welfare systems, increasing the financial burden on taxpayers. Enforcing insurance coverage shifts this responsibility to the insurance companies, where it rightfully belongs.

- Promoting Responsible Vehicle Ownership: The requirement for insurance fosters a sense of responsibility among vehicle owners. It encourages them to maintain their vehicles properly, understand their legal obligations, and be accountable for their actions on the road.

What is Required Under Section 144A?

To comply with Section 144A, vehicle owners and drivers must adhere to the following specific requirements:

- Mandatory Insurance Coverage: As reiterated, all motor vehicles on public roads must have at least third-party insurance. This policy must be valid and cover the specified liabilities.

- Continuous Insurance: The principle of CIE means that your vehicle must be insured without interruption if it is kept on a public road. Lapses in insurance, even for a short period, can lead to penalties.

- Possession of a Valid Certificate of Insurance: You must be able to produce a valid insurance certificate when requested by the police or other authorised personnel. It is advisable to keep this document readily accessible, either in hard copy or digitally.

- Correct Vehicle Registration: Ensure that your vehicle's details on the insurance policy match its registration details held by the DVLA. Discrepancies can cause issues.

Who Must Comply?

The responsibility for compliance with Section 144A falls on several parties:

- Vehicle Owners: The primary responsibility lies with the registered keeper or owner of the vehicle to ensure it is insured or declared SORN if not in use on public roads.

- Drivers: Anyone driving a vehicle must ensure that the vehicle they are operating is insured and that they themselves have the necessary licence and are complying with the terms of the insurance policy.

- Businesses and Fleet Operators: Companies operating multiple vehicles have a significant responsibility to ensure their entire fleet is insured, with appropriate policies in place for all vehicles and drivers. This includes managing renewals and ensuring all vehicles are accounted for under the CIE system.

What Vehicles are Covered?

The legislation covers a wide array of motor vehicles, ensuring comprehensive protection:

| Vehicle Type | Details |

|---|---|

| Private Cars and Motorcycles | Standard personal vehicles used for commuting, leisure, etc. |

| Commercial Vehicles | Vans, lorries, HGVs, company cars used for business purposes. |

| Specialised Vehicles | Taxis, private hire vehicles, buses, minibuses, agricultural vehicles used on public roads. |

| Classic and Vintage Vehicles | If kept on a public road, even if only used occasionally, they require insurance or a SORN. |

| Electric Scooters and Similar Devices | Certain powered personal transport devices may also fall under specific insurance regulations depending on their classification and use. |

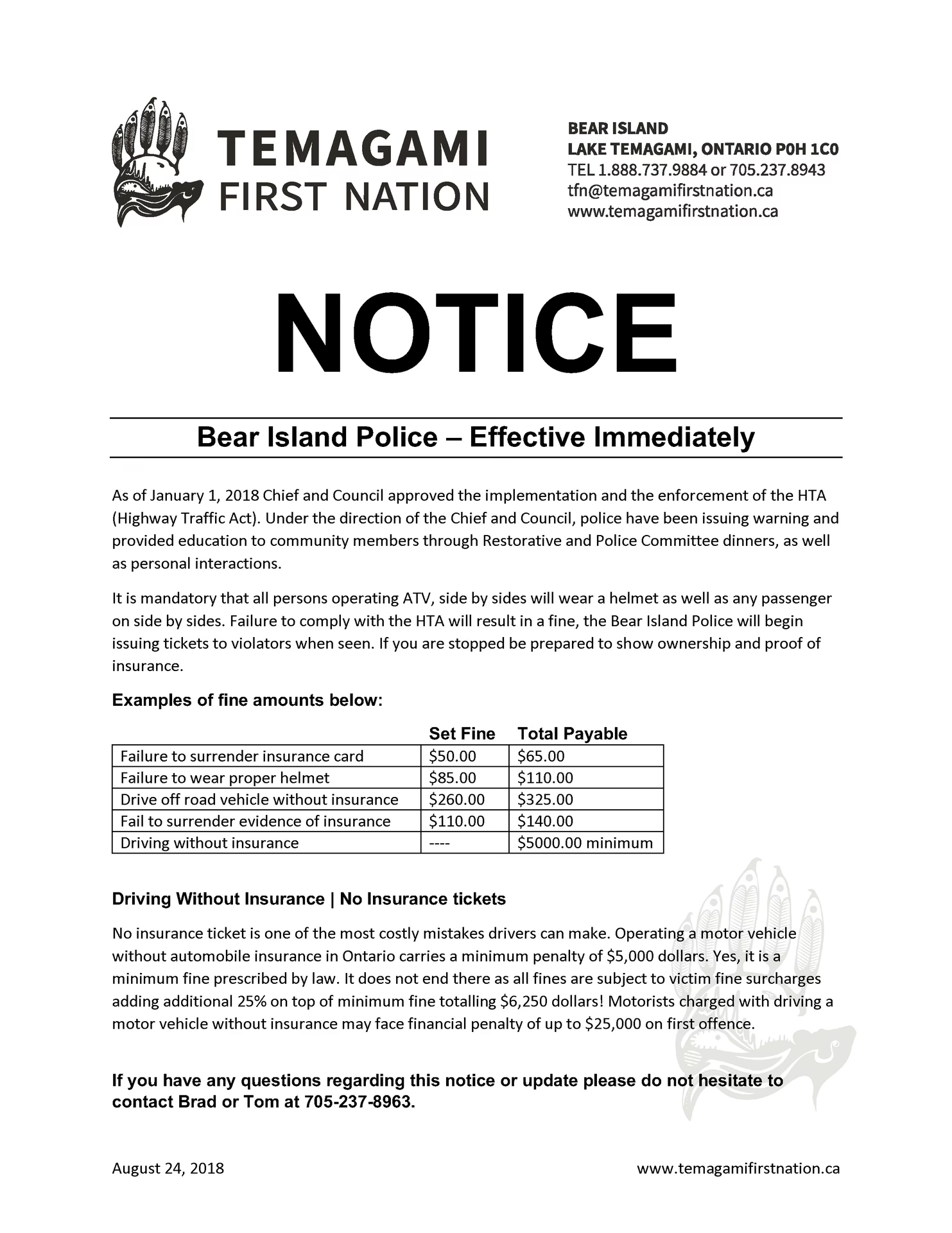

Penalties for Non-Compliance

The consequences of failing to comply with Section 144A can be severe and far-reaching:

- Fixed Penalty Notices (FPNs): Typically, an initial FPN of £300 may be issued for driving an uninsured vehicle.

- Vehicle Seizure and Impoundment: Law enforcement officers have the power to seize and impound uninsured vehicles. Recovering an impounded vehicle involves paying significant fees for towing and storage, and if these are not settled, the vehicle can be destroyed or sold.

- Court Prosecution: For more serious or repeat offences, the case may be taken to court. This can result in much higher fines, potentially unlimited, depending on the severity of the offence and the discretion of the court.

- Criminal Conviction: A court conviction for using or keeping an uninsured vehicle results in a criminal record. This can have a profound impact on future employment opportunities, international travel (especially to countries like the USA or Canada), and even mortgage or loan applications.

- Points on Driving Licence: Convictions for uninsured driving typically result in 6 to 8 penalty points on your driving licence. Accumulating 12 or more points within a three-year period can lead to disqualification from driving.

It's crucial to understand that the enforcement of CIE means that the DVLA actively identifies uninsured vehicles through data matching with the Motor Insurance Database (MID). This makes it exceptionally difficult to avoid detection.

Exemptions and Special Cases

While the rule is strict, there are limited circumstances where a vehicle might be exempt from the insurance requirement under Section 144A:

- Statutory Off-Road Notification (SORN): As mentioned, vehicles officially declared SORN and genuinely kept off public roads are exempt from insurance. This is the most common and significant exemption.

- Vehicles Used Exclusively on Private Property: Vehicles used solely on private land (e.g., farms, private estates, construction sites) and never on a public road do not require insurance under this Act.

- Certain Specialist Vehicles: Some vehicles used in agriculture or construction that are designed for off-road use and do not typically travel on public roads may be exempt, provided they remain off public roads.

- Military and Emergency Vehicles: These may operate under different regulatory frameworks and could have specific exemptions.

It is vital to ensure that any exemption claimed is valid and correctly documented. For instance, simply not taxing a vehicle does not automatically exempt it from insurance; a SORN must be properly submitted.

Ensuring Compliance with Section 144A

Staying compliant with Section 144A is straightforward if you follow these guidelines:

- Obtain Adequate Insurance: Ensure your vehicle has at least the minimum required third-party insurance cover. Consider whether comprehensive cover is more suitable for your needs.

- Maintain Continuous Cover: Be vigilant about your policy's expiry date. Renew your insurance well in advance or ensure a new policy is in place before the old one lapses. If you sell your vehicle, cancel your insurance promptly.

- Declare SORN When Necessary: If you stop using your vehicle on public roads, immediately submit a SORN declaration to the DVLA. Keep the confirmation of your SORN.

- Verify Driver Coverage: If others drive your vehicle, ensure they are named on your insurance policy or that your policy includes an "any driver" clause if applicable.

- Keep Records: Always retain a copy of your current insurance certificate. Keep records of policy renewals, payments, and any correspondence with your insurer. If you have declared a SORN, keep the confirmation document safe.

- Update Details: Ensure your address, vehicle details, and any changes in circumstances are promptly updated with both your insurer and the DVLA.

Frequently Asked Questions

Q1: What happens if my insurance expires and I don't realise it immediately?

A1: Even if you don't realise it, driving or keeping an uninsured vehicle on a public road is illegal. The CIE system is designed to catch such lapses, and you could face penalties. It is your responsibility to know when your insurance is due for renewal.

Q2: Can I drive my car on a public road if it's declared SORN?

A2: No. A vehicle declared SORN must be kept off public roads. Driving it on a public road, even to a garage or MOT station, requires you to first insure it and remove it from the SORN register.

Q3: My car is not being used and is stored in my garage. Do I still need insurance?

A3: If your garage is on a public road or your vehicle can access a public road from it, and you have not declared a SORN, then yes, it must be insured. If it's truly off-road and inaccessible to public roads, you should declare a SORN.

Q4: What if I buy a car that is uninsured?

A4: The responsibility to insure the vehicle falls on the new keeper from the moment they take ownership. If you drive it away from the seller's premises on a public road without insurance, you are committing an offence.

Q5: Are classic cars exempt from insurance?

A5: Not automatically. If a classic car is kept on a public road, it must be insured or declared SORN, regardless of how infrequently it is used. Some specialist insurers offer 'laid-up' or 'restricted use' policies for classic cars, which can be more affordable.

Section 144A of the Road Traffic Act is a fundamental piece of legislation designed to protect everyone on our roads. By understanding its requirements and taking proactive steps to ensure compliance, you not only avoid severe penalties but also contribute to a safer and more responsible motoring environment for all.

For expert legal advice regarding road traffic law or if you are facing penalties related to uninsured driving, seeking assistance from qualified legal professionals is highly recommended.

If you want to read more articles similar to UK Road Traffic Act: Section 144A Explained, you can visit the Automotive category.