21/02/2002

It's a scenario no one wants to face, but unfortunately, it's a common consequence of road traffic accidents: your vehicle is out of action, and you need a way to get around. For many, a rental car becomes the immediate solution. But what happens when the damage wasn't your fault, or when you're the one responsible? Understanding the intricacies of rental car provision after an accident is crucial, especially in the UK, where the automotive landscape and insurance regulations can sometimes feel complex. This guide aims to demystify the process, outlining who pays for what and what steps you should take.

- When Another Driver Is to Blame

- If You Are Responsible for the Accident

- Disputed Fault and Insurance Delays

- Steps to Securing a Rental Car After an Accident

- Rental Car Agreements in the UK: Key Considerations

- FAQs

- Q: What happens if the insurance company is being difficult about my rental car?

- Q: Can I speed up the process with the at-fault driver's insurance company?

- Q: What if the insurance company refuses to pay for a rental car even when the other driver is clearly at fault?

- Q: Does the at-fault driver pay for the rental car?

- Q: What if my car insurance doesn't cover the accident?

- Q: How do I get rental car reimbursement if I wasn't at fault?

When Another Driver Is to Blame

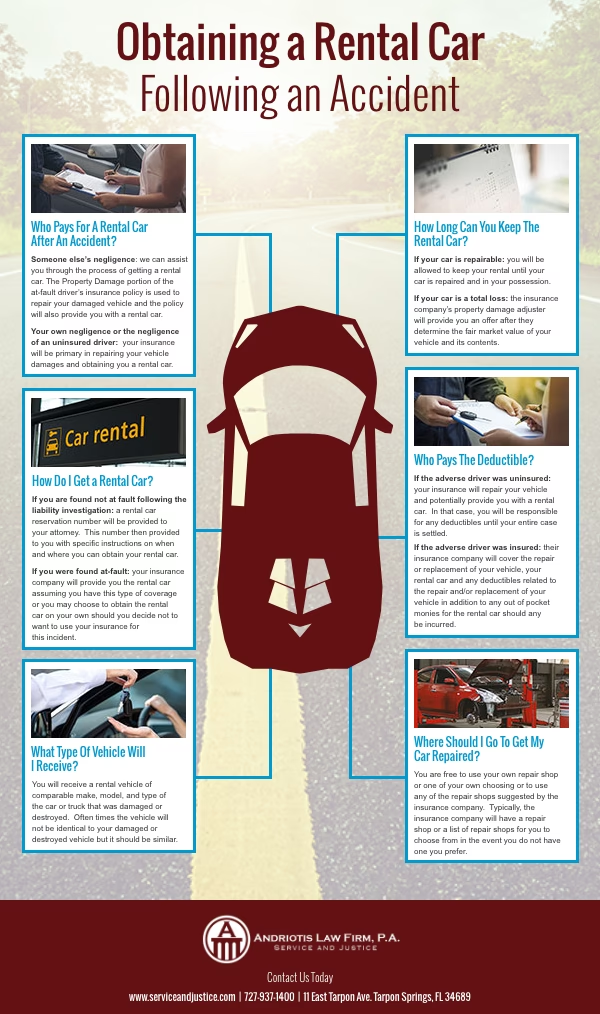

If your vehicle has been damaged by another driver's negligence, the general principle is that the at-fault party's insurance should cover your losses. This extends to the cost of a rental car while your own vehicle is undergoing repairs. The rationale behind this is straightforward: the party responsible for the accident should bear the financial burden of the resulting inconvenience and necessary expenses. In the UK, this typically means the third-party insurer of the driver who caused the accident will be liable for your rental car costs for a reasonable period of repair.

However, it's not always as simple as a direct handover. You'll likely need to engage with the other driver's insurance company. It's advisable to confirm the specifics of their coverage and their process for authorising rental vehicles. Sometimes, their insurer might offer a direct arrangement with a rental company, or they may reimburse you for costs incurred, provided you keep all your receipts. It's important to be aware that insurance companies, regardless of fault, may employ strategies to manage their payouts, so clear communication and documentation are key.

If You Are Responsible for the Accident

The situation changes significantly if you are deemed to be at fault for the accident. In this instance, your ability to secure a rental car at no direct cost to yourself hinges entirely on your own insurance policy. Specifically, you'll need to have purchased rental reimbursement coverage as an add-on to your comprehensive or collision insurance. This is an optional coverage, and it's not automatically included in all policies. If you have this cover, your insurer should step in to cover the costs of a rental car for a specified period, as outlined in your policy terms.

Without this specific coverage, you would typically be responsible for the full cost of the rental vehicle yourself. This is where understanding your policy documents before an incident occurs becomes paramount. Many drivers opt for this coverage due to the significant disruption a vehicle being off the road can cause.

Disputed Fault and Insurance Delays

Accidents, unfortunately, can lead to disputes over who was actually at fault. This can significantly complicate the process of obtaining a rental car. If liability is unclear or contested, the insurance companies involved may be hesitant to authorise rental costs until the matter is resolved. This is where staying in close communication with your own insurance provider is vital. If you have rental reimbursement coverage, your insurer can often provide a rental car while they work to recover the costs from the other party's insurer through a process called subrogation.

If the other party's insurer is delaying a decision or disputing your claim, and you do not have your own rental coverage, you may find yourself paying for the rental car out of your own pocket. It's crucial to keep meticulous records of all communication with insurance adjusters. Requesting communication in writing can provide valuable evidence should disputes arise later. In cases of prolonged delays or unreasonable behaviour from an insurance company, you might consider contacting your local Division of Insurance or seeking legal advice.

Steps to Securing a Rental Car After an Accident

Navigating the aftermath of an accident can be stressful. Here's a practical step-by-step approach to securing a rental car:

- Review Your Insurance Policy: The very first step is to thoroughly examine your own car insurance policy. Look for a section on 'rental reimbursement' or 'courtesy car' coverage. Note any daily maximums, the total number of days covered, and any limitations on the type of vehicle you can rent.

- Contact Your Insurance Agent or Provider: Once you've reviewed your policy, contact your insurance agent or the claims department. They can confirm your coverage, explain the process, and advise you on approved rental companies or direct you on how to proceed.

- Understand Your Coverage While Driving the Rental: It's essential to know if your existing insurance coverage extends to the rental car. Typically, if you have comprehensive and collision coverage, it will transfer to the rental. However, clarify this with your insurer to avoid any surprises.

- Communicate with the At-Fault Party's Insurer (If Applicable): If the other driver caused the accident, contact their insurance company to initiate a claim for your rental car needs. Be prepared for potential delays or requests for documentation.

- Consider Your Transportation Needs: If your vehicle is expected to be in the repair shop for an extended period, or if your rental coverage has limits, think about alternative transportation options. This could include rideshare services, public transport, or even negotiating a longer-term rental if your insurer agrees.

Rental Car Agreements in the UK: Key Considerations

The popularity of car rentals in the UK is undeniable, driven by factors like the high cost of new vehicles and fluctuating fuel prices. When you rent a car in the UK, the rental agreement is your key document. It will outline the terms and conditions, including:

Liability and Insurance

In the UK, rental car agreements typically include Third Party Liability Insurance, often with unlimited coverage. This is a legal requirement for all drivers. Many rental companies bundle this, along with Collision Damage Waiver (CDW) and Theft Protection, into a pre-paid package. However, it's crucial to understand that CDW usually means the rental company waives their right to charge you the full cost of repairs for bodywork damage. You will almost always still be liable for an 'excess' payment.

The Excess Payment

The excess is the amount you, the renter, must contribute towards the cost of repairs if the vehicle is damaged, or towards its replacement if it's stolen. This figure can vary significantly, often ranging from £500 to £3,000 or more, depending on the vehicle type and the rental company's policy. Some specialised insurance providers offer 'car hire excess insurance,' which can cover this excess amount, providing an extra layer of financial protection.

Rental Costs During Repair

Your rental agreement should also specify whether you are obliged to continue paying the rental fees while your vehicle is undergoing repairs. Furthermore, it should confirm whether you are entitled to a replacement vehicle at no additional cost if your rental is involved in an incident.

FAQs

Q: What happens if the insurance company is being difficult about my rental car?

If the at-fault driver's insurer is delaying a decision or arguing about fault, and you have rental coverage on your policy, file a claim with your insurer. They will cover the rental and then seek reimbursement from the other party's insurer. If you don't have your own coverage, you might have to pay out-of-pocket. You can also contact your state's or local Division of Insurance for assistance, or consult an attorney to put pressure on the insurer.

Q: Can I speed up the process with the at-fault driver's insurance company?

Having an experienced attorney can often expedite the process. Insurance companies may respond more quickly when faced with the potential of legal action. Documenting all communications in writing is also crucial for building a case and demonstrating the necessity of a timely resolution.

Q: What if the insurance company refuses to pay for a rental car even when the other driver is clearly at fault?

This is a common tactic. Your options include filing a claim with your own insurer if you have rental coverage, contacting your local Division of Insurance, or hiring a lawyer. A lawyer can send a demand letter and negotiate on your behalf, potentially resolving the issue more swiftly. Always review any settlement offer carefully to ensure it doesn't waive your rights to property damage and rental car reimbursement.

Q: Does the at-fault driver pay for the rental car?

Yes, if the other driver is proven to be at fault for the accident, their insurance company should cover your rental car costs. However, the process can be slow, and they may dispute liability. If you have rental coverage, your insurer can cover the costs and then pursue the at-fault party's insurer for reimbursement.

Q: What if my car insurance doesn't cover the accident?

If you only have minimum liability coverage and no comprehensive or collision cover, your insurance won't pay for damage to your vehicle. If the other driver was at fault, you'll need to claim against their insurance. If the at-fault driver was uninsured or underinsured, your Uninsured/Underinsured Motorist (UM/UIM) coverage may apply.

Q: How do I get rental car reimbursement if I wasn't at fault?

You can file a claim with the at-fault driver's insurance company. If they delay or dispute, you can use your own insurance's rental coverage and let them pursue subrogation. Consulting an attorney early on can significantly speed up the recovery of your rental car reimbursement and other damages.

Ultimately, being informed about your insurance coverage and understanding the procedures following an accident are your best defences against unexpected costs and prolonged inconvenience. If you're unsure about your rights or are facing difficulties with an insurance claim, seeking professional legal advice is always a prudent step.

If you want to read more articles similar to Rental Car Woes After an Accident, you can visit the Insurance category.