24/08/2024

- Can Robo-Taxis Deliver Affordable Mobility?

- The Road to Affordable Autonomous Mobility

- Key Cost Drivers and Economic Projections

- Factors Influencing Robo-Taxi Costs

- Implications for Industry Stakeholders

- The Role of Autonomy in Decarbonisation

- COVID-19's Impact on Autonomous Driving

- The Future of Mobility: MaaS and Robo-Taxis

- Conclusion: The Economic Case for Robo-Taxis

- Frequently Asked Questions (FAQs)

Can Robo-Taxis Deliver Affordable Mobility?

The automotive industry is on the cusp of a significant transformation, driven by the advent of autonomous vehicle (AV) technology. As these self-driving services, particularly robo-taxis and robo-shuttles, begin to roll out and scale, their impact on the entire mobility value chain will be profound. For sectors already grappling with disruption, such as electrification, understanding the localized mobility contexts and the evolution of AV technology is paramount to assessing the future landscape. This article delves into the potential of shared AV services to deliver affordable mobility, examining the critical cost factors, consumer adoption drivers, and the broader implications for various industry stakeholders.

The Road to Affordable Autonomous Mobility

The viability of robo-taxis and robo-shuttles hinges on a confluence of factors: regulatory frameworks, technological readiness, the attractiveness of the business case, and crucially, customer preference. Consumer acceptance is intrinsically linked to how the costs of these AV services compare to existing mobility options. While the initial fully burdened costs for these services are currently substantial, owing to high technology, development, and operational expenditures, a significant decline is anticipated over the next decade. This reduction will be fuelled by advancements in AV technology and the emergence of more integrated, seamless, and multimodal mobility ecosystems. Our analysis suggests that, unlike traditional mobility models, shared AV services will necessitate new operational paradigms where costs are meticulously managed to ensure profitability and competitiveness.

The potential for robo-taxis to become price-competitive with private non-autonomous cars, and even public transit services, is substantial. We project that in certain contexts, the cost per mile for a robo-taxi could be as little as 20 percent higher than that of a private, non-autonomous car. Robo-shuttles, while potentially less convenient, could even be 10 to 40 percent cheaper. Furthermore, for personal, non-pooled robo-taxi trips, the cost per mile could be as low as 40 to 50 percent of a traditional driver-based ride-hailing service. Beyond mere price competitiveness, enhanced convenience and a growing perception of safety, as AV performance continues to improve, are expected to be key drivers of consumer acceptance. Regulatory interventions, such as bans on private single-occupancy vehicles in city centres or the implementation of congestion charges, could further tip the scales, making private car ownership less attractive and more expensive, thereby encouraging a shift towards shared autonomous mobility.

Key Cost Drivers and Economic Projections

While early robo-taxi services will undoubtedly carry a higher cost than today's driver-based options, we anticipate this gap to narrow rapidly. Our projections indicate that the cost per mile for robo-taxis could decrease by over 50 percent between 2025 and 2030. This significant reduction will be driven by several key factors:

- Decreasing Hardware Costs: The declining cost of high-performance chips and sensors will play a crucial role.

- Operational Efficiencies: Reduced maintenance requirements, higher overall mileage accumulation, and a decrease in empty miles travelled will contribute to lower operating costs.

- Economies of Scale: As the technology matures and adoption increases, development and validation costs will be amortised across a larger fleet, lowering the per-unit cost.

- Smarter Fleet Management: Improved algorithms for route planning and demand forecasting will minimise idle time and empty miles.

When comparing the total cost of ownership (TCO) for private vehicles versus robo-taxis, the economics present an interesting picture. Private vehicle costs encompass depreciation, operation (fuel, cleaning, maintenance, parking), and fixed costs (insurance, financing, registration). Despite the added expense of AV hardware and software, robo-taxis may exhibit lower depreciation rates per mile by 2030, primarily due to significantly higher utilisation rates and longer projected lifetime mileage. This advantage will likely necessitate the development of purpose-built vehicles designed for enhanced durability and suitability for robo-taxi applications.

However, robo-taxis are expected to incur substantially higher operating costs, particularly in the initial years. These include:

- AV System Maintenance: Regular check-ups, error tracking, and sensor recalibration will be critical and potentially costly.

- Remote Operations: Maintaining remote vehicle control centres to manage edge cases (e.g., unmapped construction zones), support passengers, and ensure smooth operations will add to overheads.

- Data and Mapping: The need for regularly updated AV maps and location-based services, such as road hazard warnings and traffic sign recognition, represents an ongoing cost.

- Energy Consumption: Autonomous systems, including sensors and high-performance computing, are expected to increase energy usage.

- Wear and Tear: Increased utilisation will lead to greater wear and tear, and higher cleaning demands, especially for vehicle interiors.

Beyond vehicle-specific costs, mobility services themselves account for a significant portion of the total cost. This includes payment processing, customer app development and operation, data analytics for fleet optimisation, customer support, marketing, and general administrative functions.

Factors Influencing Robo-Taxi Costs

The cost per mile for AV services is not uniform and is influenced by several key variables:

1. Geographic Location and Market Dynamics

The operational area significantly impacts overall costs. For instance, a robo-taxi trip in China might be 5 to 25 percent cheaper than an equivalent trip in the United States, attributed to lower labour and energy costs, as well as differing base vehicle costs influenced by local customer requirements. Despite these variations, purchasing power differences across geographies can still support a strong business case for AVs.

2. City Density and Operational Efficiency

City density plays a critical role. In areas with lower population density, robo-taxis will likely experience a higher proportion of empty miles. To compensate, fleet operators will need to charge more for revenue-generating miles. The cost difference between operating in a transit-oriented city like Philadelphia and a more car-dependent peripheral city like Indianapolis could be as much as 50 percent.

3. Vehicle Type and Specialisation

The type of vehicle used will have a substantial impact on per-mile costs. A premium, SUV-sized robo-taxi could command a per-mile price double that of a compact, two-seater autonomous vehicle. Similarly, a robo-shuttle operating within a confined area at low speeds, such as a campus or residential complex, could cost significantly less than one undertaking longer, higher-speed inter-city routes. These cost differences stem from varying sensor and computing requirements; low-speed systems, for example, may not need long-range LiDAR and will have lower maintenance and operational costs. If these low-speed shuttles are integrated into public transit networks, the need for extensive marketing or complex payment systems can also be reduced.

4. Operational Scale and Market Dominance

The scale of operations is a critical determinant of cost-effectiveness. Companies operating at a significant scale can amortise high initial investments across a larger fleet, potentially achieving price points six to eight times lower than smaller, subscale competitors. This suggests that players initially focusing on specific local markets will likely need to form partnerships with larger, scaled operators or rely on local operational excellence to remain competitive. We foresee a trend towards consolidation, with a smaller number of dominant players emerging.

Implications for Industry Stakeholders

The burgeoning robo-taxi ecosystem will reshape the strategies and operations of numerous industry players:

- Automakers (OEMs): OEMs entering the robo-taxi sector must develop purpose-built vehicles that prioritise durability, low maintenance, and high uptime. Predictive maintenance, modular battery systems, and fast-charging capabilities will be essential. To transition into mobility service providers, OEMs will need to secure partnerships, investment, and AV technology expertise to orchestrate a complete solution, or offer integrated vehicles with their own AV stacks while outsourcing the mobility service component.

- Mobility Service Providers: These operators must focus on achieving market leadership in select cities to leverage economies of scale in areas like vehicle control centres and local hubs. Reducing operational and service provisioning costs through smart strategies for hub placement, charging schedules, and advanced algorithms for route planning and demand forecasting will be paramount.

- Cities and Transit Agencies: Municipalities will wield significant influence through pricing mechanisms, subsidies, and licensing. They can shape their mobility mix by fostering integrated transit systems, making robo-shuttles more attractive than private cars but less so than public transport, or by leasing strategically located properties to reduce empty ride costs.

- Suppliers: Suppliers should strategically allocate R&D to enhance AV durability and reduce energy demand. Some may need to pivot their business models, transitioning from component suppliers to providers of AV maintenance or vehicle control centre operations. Partnerships across the automotive ecosystem, particularly with aftermarket players, will be crucial.

- AV Technology Players: These companies must clearly define their role within the ecosystem, whether by developing the full AV tech stack, sourcing base vehicles, licensing their technology, or providing engineering expertise to various partners.

The Role of Autonomy in Decarbonisation

The widespread adoption of AVs has significant implications for the carbon footprint of the mobility sector. An unconstrained rollout, driven by lower costs and increased convenience, could lead to an increase in vehicle miles travelled (VMT), potentially acting as a headwind to decarbonisation efforts, even if AVs are predominantly electric. However, in a well-managed and integrated mobility transition, AV services can complement a more environmentally friendly ecosystem. Policies that encourage the pooling of robo-taxis and shuttles, and their close integration with public transit, can create a significant tailwind for decarbonisation efforts.

COVID-19's Impact on Autonomous Driving

The COVID-19 pandemic has introduced some complexities to the AV rollout. While testing was suspended and investments were scaled back in 2020, leading to layoffs and project halts for some players, the mid-term outlook suggests delays of months rather than years. Industry observers anticipate further consolidation and increased cooperation. Despite these short-term disruptions, the long-term importance of robo-taxis as a significant revenue pool, potentially reaching $1.3 trillion by 2030, remains high. Consumer demand for autonomous solutions is also expected to grow. The pandemic may have accelerated a shift towards private mobility options for some, but the underlying trend towards shared, on-demand, and potentially autonomous services is expected to persist.

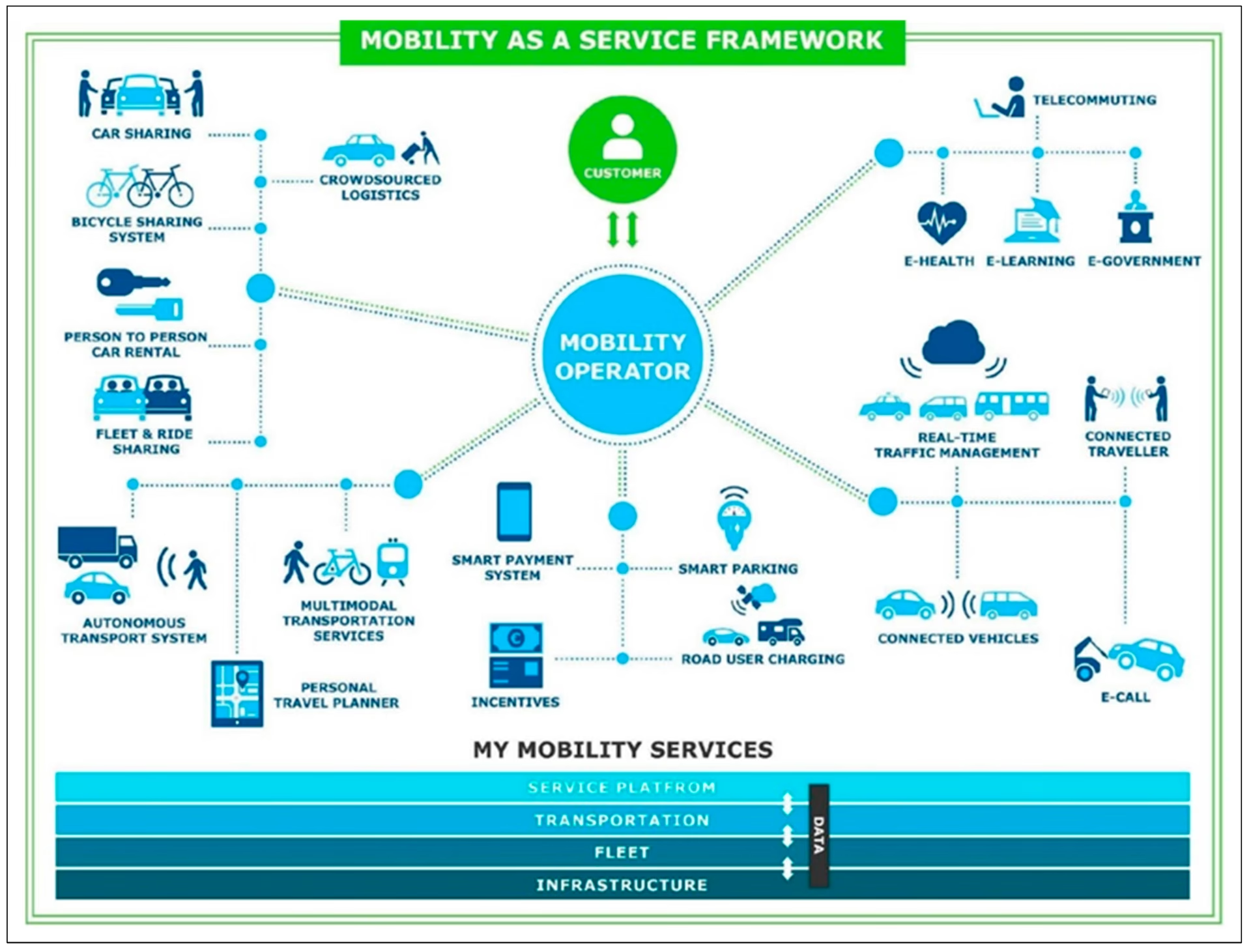

The Future of Mobility: MaaS and Robo-Taxis

The concept of Mobility as a Service (MaaS) is intrinsically linked to the rise of robo-taxis. MaaS integrates various transportation modes – ride-sharing, car-sharing, bike-sharing, scooters, and public transit – into a single, user-friendly platform. This allows users to plan, book, and pay for their journeys seamlessly across multiple options. Key components of MaaS include multimodal transport, real-time information, integrated payment systems, and data analytics. Experts from Accenture, Deloitte, and McKinsey all highlight the transformative potential of MaaS, with projections indicating substantial market growth. They agree on the vital role of public-private partnerships, the importance of cities in shaping mobility policies, and the growing consumer acceptance of shared mobility. McKinsey, in particular, places a strong emphasis on robo-taxis and robo-shuttles as the future of MaaS, offering more affordable point-to-point travel options. The successful implementation of MaaS will require collaboration across stakeholders, the development of customer-centric offerings, and potentially, purpose-built vehicles designed for shared-use scenarios.

Conclusion: The Economic Case for Robo-Taxis

The transition to autonomous mobility, particularly through robo-taxis, presents a compelling economic case for the future. While significant technological and operational challenges remain, the potential for cost reduction, increased efficiency, and enhanced accessibility is substantial. For robo-taxis to deliver on their promise of affordable mobility, the industry must focus on achieving adequate scale, fostering a robust AV ecosystem, and relentlessly pursuing operational excellence. The economics of robo-taxis are sensitive to various cost assumptions, with vehicle durability and mobility provisioning costs having the most significant impact on total cost of ownership. By addressing these factors and embracing the collaborative spirit of MaaS, robo-taxis are poised to revolutionise urban transportation, making it more sustainable, convenient, and affordable for all.

Frequently Asked Questions (FAQs)

Q1: Will robo-taxis be cheaper than owning a car?

In many scenarios, particularly with pooled rides and high utilisation, robo-taxis are projected to be more cost-effective per mile than owning and operating a private vehicle by 2030, when factoring in all associated costs of ownership and usage.

Q2: What are the main cost drivers for robo-taxis?

The primary cost drivers include the initial investment in AV hardware and software, ongoing maintenance of the autonomous systems, operational costs for remote support centres, data and mapping services, energy consumption, and the costs associated with the mobility service platform itself (app development, customer support, etc.).

Q3: How will regulations affect robo-taxi adoption?

Regulations will play a crucial role. Policies that restrict private vehicle use in urban centres, implement congestion charges, or favour shared mobility can significantly boost the adoption and economic viability of robo-taxis.

Q4: What is Mobility as a Service (MaaS)?

MaaS integrates various transportation modes (public transit, ride-sharing, bike-sharing, etc.) into a single platform, allowing users to plan, book, and pay for their journeys seamlessly. Robo-taxis are expected to be a key component of future MaaS offerings.

Q5: How quickly will robo-taxis become affordable?

While initially more expensive, significant cost reductions are expected between 2025 and 2030, driven by technological advancements and economies of scale, making them increasingly competitive with traditional options.

If you want to read more articles similar to Robo-Taxis: The Future of Affordable Urban Mobility?, you can visit the Automotive category.