16/09/2015

When discussing property transactions or vehicle damage claims, you might encounter the term 'cash in lieu of repairs'. This phrase essentially means that instead of carrying out the agreed-upon or necessary repairs, a sum of money is exchanged. This financial settlement allows one party to receive funds to cover the cost of repairs, which they can then choose to undertake themselves, defer, or even forego. Understanding the nuances of this arrangement is crucial for all parties involved, as it impacts financial obligations, property condition, and future resale values.

What is Cash in Lieu of Repairs?

At its core, 'cash in lieu of repairs' is a financial settlement that replaces the physical act of repairing a property or a vehicle. Instead of the seller or a responsible party performing specific repairs before a sale or as part of an insurance claim, they provide the buyer or claimant with an equivalent amount of money. This allows the recipient greater flexibility in how and when the repairs are addressed.

Contexts for Cash in Lieu of Repairs

This concept appears in several key areas:

Property Transactions

In real estate, it's common for a home inspection to reveal issues that need addressing before a sale can be finalised. These could range from minor cosmetic flaws to more significant structural problems like a leaky roof or faulty wiring. If a seller is unwilling or unable to perform the necessary repairs, they might offer the buyer 'cash in lieu of repairs'. This cash amount is typically negotiated and is meant to cover the estimated cost of the repairs. The buyer then receives this money at closing and is responsible for arranging and paying for the repairs themselves. This can be advantageous for buyers who have preferred contractors or wish to upgrade the property beyond the scope of the original required repairs.

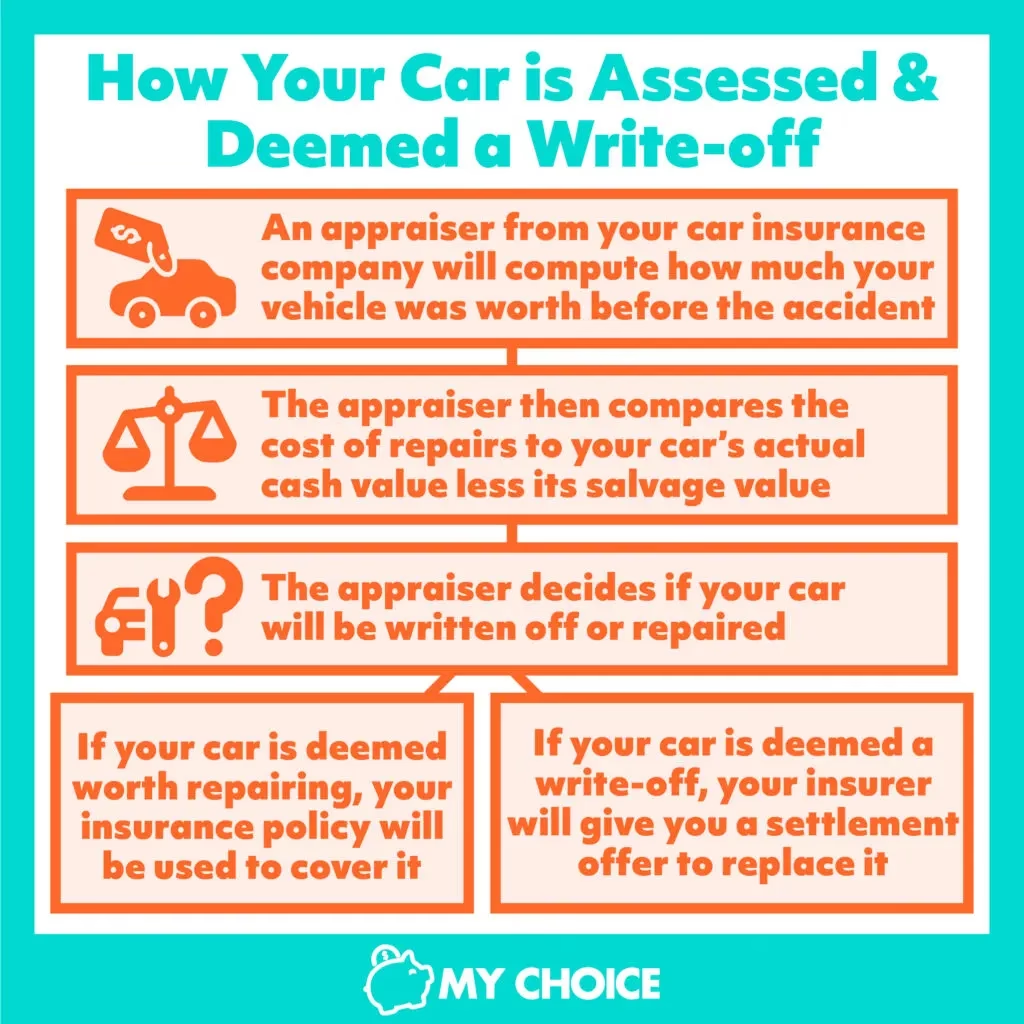

Automotive Insurance Claims

When a vehicle is damaged, an insurance company will typically assess the damage and provide an estimate for repairs. In some cases, particularly with older vehicles or minor damage, the insurer might offer 'cash in lieu of repairs'. This means they will pay the insured the estimated cost of the repairs, but the insured is not obligated to actually fix the car. They might choose to keep the vehicle as is, undertake the repairs themselves with a different, perhaps cheaper, method, or even use the money for a down payment on a new vehicle. It's important to note that if an insured accepts cash and doesn't perform the repairs, they may face issues if the unrepaired damage causes further problems or affects the vehicle's safety.

Homeowners Insurance Claims

Similar to automotive claims, homeowners insurance policies can also involve 'cash in lieu of repairs'. If a home sustains damage (e.g., from a storm, fire, or water damage), the insurer might offer a cash settlement to cover the repair costs. This is often the case for smaller claims or when the policyholder prefers to manage the repairs independently. For example, if a homeowner has a preferred builder or wants to make improvements beyond the original damage, accepting cash can be beneficial. However, it's crucial to ensure the repairs are carried out to restore the property to its pre-loss condition, especially if the property is mortgaged, as lenders may have specific requirements.

Advantages of Cash in Lieu of Repairs

There are several reasons why parties might opt for this type of settlement:

- Flexibility: The recipient has the freedom to choose their own contractors, use different materials, or even decide not to proceed with the repairs immediately.

- Cost Savings: If the recipient is skilled or can find a cheaper contractor than the one estimated by the seller or insurer, they might save money.

- Convenience: For sellers or insurers, it can be more convenient than managing the repair process, especially if they are located remotely or have many claims to handle.

- Personalisation: In property sales, buyers can use the funds to make upgrades or renovations that better suit their needs and taste, rather than being limited to the original repair scope.

Disadvantages and Considerations

While offering flexibility, accepting or offering cash in lieu of repairs also comes with potential drawbacks:

For the Recipient:

- Responsibility: The entire burden of managing and paying for the repairs falls on the recipient. If the estimated cost is insufficient, they will have to cover the difference.

- Quality Control: There's no guarantee that the repairs will be carried out to the same standard as if the original party had managed them.

- Delayed Repairs: The recipient might be tempted to delay or neglect the repairs, potentially leading to further damage or a decrease in property/vehicle value.

- Financing Issues: If the property is mortgaged, lenders may require proof that repairs have been completed to maintain the loan's security.

For the Payer:

- Potential for Disputes: The amount offered might be disputed if it doesn't accurately reflect the cost of necessary repairs.

- Future Liability: If the repairs are not adequately completed by the recipient, the original party might still face scrutiny or claims down the line, especially if the unrepaired issue causes subsequent problems.

Negotiating Cash in Lieu of Repairs

When this option is on the table, negotiation is key. Both parties should aim for a figure that is fair and accurately reflects the cost of the required repairs. Here’s how to approach it:

For Buyers/Claimants:

- Get Multiple Quotes: Obtain repair estimates from at least three reputable contractors. This provides a solid basis for negotiation.

- Factor in Contingencies: Always add a buffer (e.g., 10-20%) to the quotes to account for unforeseen issues that might arise during the repair process.

- Consider Time Value: If you are receiving cash and will undertake repairs later, factor in potential increases in material and labour costs over time.

For Sellers/Insurers:

- Provide Documentation: Offer the repair estimate you used to determine the cash amount.

- Be Realistic: Understand that the recipient may have different preferences or needs.

- Clear Agreement: Ensure the agreement clearly states what repairs the cash is intended to cover and that upon payment, the obligation for those specific repairs is fulfilled.

Legal and Contractual Aspects

It is vital to have a clear, written agreement when 'cash in lieu of repairs' is involved. This document should detail:

- The specific repairs covered by the cash settlement.

- The exact amount of money being exchanged.

- The date by which the payment will be made.

- Confirmation that the payment satisfies the repair obligation.

In property sales, this agreement is often added as an addendum to the purchase contract. For insurance claims, it will be documented within the claim settlement paperwork.

Example Scenarios

Scenario 1: Property Sale

A buyer agrees to purchase a house, but the inspection reveals that the roof needs replacing, estimated at £8,000. The seller doesn't want the hassle of organising the repair and offers the buyer £7,500 in cash at closing to cover the roof replacement. The buyer accepts, using the £7,500 to hire their preferred roofing company.

Scenario 2: Car Insurance

A car is involved in a minor fender-bender. The insurance company estimates the repair cost at £1,200. The car is older, and the owner decides they would rather use the money towards a newer vehicle. They accept a cash settlement of £1,000 (after the excess) from the insurer and keep the damaged car.

Frequently Asked Questions

Q1: Is 'cash in lieu of repairs' always the best option?

A1: Not necessarily. It depends on your priorities. If you want the repairs done to a specific standard or are not comfortable managing the process, having the repairs done by the obligated party might be better. If you value flexibility and potential cost savings, cash can be advantageous.

Q2: Who typically estimates the repair costs?

A2: In property sales, it's often based on quotes obtained by either party. For insurance claims, the insurer provides the estimate, though the claimant can dispute it with their own estimates.

Q3: What happens if the cash received isn't enough to cover the repairs?

A3: If you receive cash in lieu of repairs, you are responsible for any costs exceeding the amount received. This is why obtaining your own quotes and negotiating a fair amount is crucial.

Q4: Can I negotiate the amount offered for 'cash in lieu of repairs'?

A4: Absolutely. It is a negotiation, and you should ensure the amount is sufficient to cover the necessary work, ideally with a contingency.

Q5: Are there tax implications for receiving cash in lieu of repairs?

A5: In most cases, cash received to compensate for the cost of repairs to a personal asset (like a home or car) is not considered taxable income, as it's intended to restore the asset's value. However, it's always advisable to consult with a tax professional for specific advice.

Conclusion

'Cash in lieu of repairs' is a financial mechanism that offers flexibility but also places responsibility on the recipient. Whether in real estate transactions or insurance settlements, understanding the implications, negotiating effectively, and ensuring clear documentation are paramount to a successful outcome. Always weigh the benefits of flexibility against the responsibility of managing the repairs yourself.

If you want to read more articles similar to Understanding Cash In Lieu of Repairs, you can visit the Automotive category.