18/01/2009

Driving in the UK comes with responsibilities, not least the legal requirement for car insurance. We dutifully pay our premiums year after year, often without a full grasp of what our money actually buys us. The common understanding is that insurance kicks in after a crash, but what about those perplexing moments when your car simply stops working, or a vital component fails? Who pays for repairs if a car is "faulty"? This article aims to demystify the complex world of car insurance, clarifying when your policy will cover repair costs and, crucially, when it won't. Understanding the nuances of your coverage is paramount to avoiding unexpected financial burdens.

- Understanding Your Car Insurance Policy: A Crucial Distinction

- When Does Car Insurance Cover Repairs? Accident-Related Damage

- How Do Car Insurance Companies Decide on Repairs?

- Does It Matter Who's at Fault in an Insurance Claim?

- Comparative Table: Car Insurance Coverage Levels

- Scenarios: Who Pays for Accident Repairs?

- What if My Car Has a Manufacturing Defect?

- Beyond Standard Car Insurance: Other Protections for Mechanical Issues

- When Your Insurance Might Not Pay Out: Invalidating Your Policy

- Frequently Asked Questions (FAQs)

- Conclusion

Understanding Your Car Insurance Policy: A Crucial Distinction

Before diving into specific scenarios, it's vital to grasp a fundamental distinction: car insurance is primarily designed to cover damage or loss resulting from unforeseen events like accidents, theft, fire, or vandalism. It is not a maintenance contract or a warranty for mechanical reliability. This is where the term "faulty" can become ambiguous. Does "faulty" refer to damage caused by an accident, or does it mean a component has failed due to its age or normal usage? The answer to this question profoundly impacts who pays for the repairs.

Standard car insurance policies, regardless of their level, explicitly exclude coverage for wear and tear and general mechanical breakdown. Think of it this way: your car's engine or gearbox failing because it's old or has accumulated high mileage is considered an expected part of vehicle ownership and maintenance. Insurance companies price their policies based on risk assessments for unpredictable events, not the predictable degradation of parts over time. Therefore, if your car is "faulty" because its engine gives up the ghost or its brakes fail due to normal usage, your standard car insurance policy will not cover the cost of those repairs. This is a common misconception that often leaves motorists feeling frustrated and financially exposed.

While standard insurance doesn't cover mechanical faults arising from age or use, it is your primary financial safeguard against the costs of damage caused by specific, insurable events. The scope of coverage depends entirely on the type of policy you hold.

- Comprehensive Car Insurance: This is the highest level of cover available and offers the broadest protection. It covers damage to your own vehicle resulting from an accident (regardless of who was at fault), theft, vandalism, fire, and natural disasters such as floods or hail. So, if your car becomes "faulty" because it was involved in a collision, comprehensively insured, your insurer will typically cover the repair costs to get it back on the road, or declare it a write-off if the damage is too severe.

- Third-Party Fire & Theft (TPFT) Insurance: This policy offers a mid-range level of protection. In addition to covering damage to other people's vehicles or property and injuries to others (the "third party" element), it also covers your own car if it is stolen or damaged by fire. However, crucially, it does not cover damage to your car if it's involved in an accident, even if the accident wasn't your fault. In such a scenario, you would typically need to claim against the at-fault driver's insurance, which can be a longer and more complex process.

- Third Party Insurance Cover: This is the minimum legal requirement for driving on UK roads. It solely covers damage or injury caused to other people, their vehicles, or their property in an accident where you are deemed at fault. It offers absolutely no protection for your own vehicle, meaning if your car is damaged in a collision, you would be solely responsible for the repair costs. This level of cover is becoming less common, with most insurers nudging drivers towards TPFT or Comprehensive policies.

How Do Car Insurance Companies Decide on Repairs?

After an insurable event, such as a road traffic collision, your insurer will initiate a claims process. This typically involves them either sending an investigator to assess the damage at the scene or, more commonly, arranging for your car to be taken to an approved repair centre or an assessment facility. The insurer's experts will then evaluate the extent of the damage, taking into account several factors:

- Level of Damage: The primary consideration is how severe the damage is and whether it's economically viable to repair.

- Age of the Car: Older cars with lower market values are more likely to be declared a "write-off" even for relatively minor damage, as the cost of repair might exceed the car's pre-accident value.

- Mileage on the Car: High mileage can also contribute to a lower market value, influencing the repair vs. write-off decision.

If the cost of repairs approaches or exceeds the car's market value, the insurer will likely declare it a "write-off." This means they will pay you the market value of the car (minus any excess) rather than repairing it.

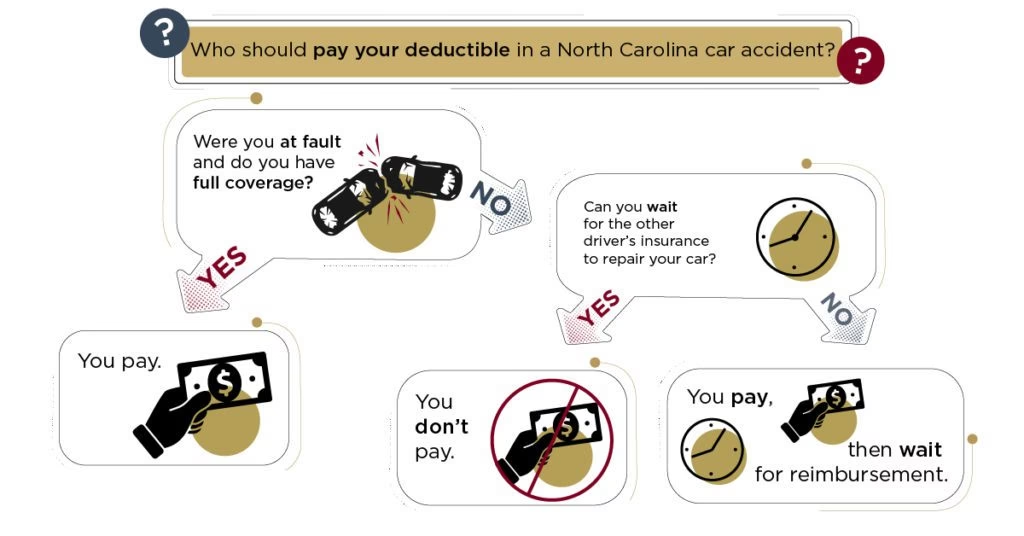

Does It Matter Who's at Fault in an Insurance Claim?

This is a frequently misunderstood aspect of car insurance. For those with comprehensive cover, the question of who is at fault for an accident does not prevent you from being compensated for damage to your car and any personal injuries you sustain. Your comprehensive policy will cover your costs regardless of fault. The determination of fault primarily dictates which insurer ultimately bears the financial burden of the entire incident. If you are deemed at fault, your insurer will pay for your repairs and the third party's damages. If the other driver is at fault, their insurer will pay for your damages (either directly or by reimbursing your insurer if you've already claimed through them).

For those with only Third-Party Fire & Theft or Third-Party cover, fault is critical. If you are at fault, your policy will only cover the third party's costs, leaving you to pay for your own car's repairs. If the other driver is at fault, you would claim directly against their insurance to cover your vehicle's damage.

Comparative Table: Car Insurance Coverage Levels

| Feature/Coverage Aspect | Third Party (Minimum) | Third-Party Fire & Theft (TPFT) | Comprehensive |

|---|---|---|---|

| Damage to Other People's Cars | Yes | Yes | Yes |

| Damage to Other People's Property | Yes | Yes | Yes |

| Injuries to Other People | Yes | Yes | Yes |

| Your Car Damaged in an Accident | No | No | Yes (regardless of fault) |

| Your Car Stolen | No | Yes | Yes |

| Your Car Damaged by Fire | No | Yes | Yes |

| Your Car Damaged by Vandalism | No | No | Yes |

| Your Car Damaged by Natural Disaster | No | No | Yes |

| Accidental Damage (e.g., parking ding) | No | No | Yes |

| Personal Injury to You | No | No | Yes (usually via personal accident cover) |

Scenarios: Who Pays for Accident Repairs?

Let's illustrate with practical examples based on common road incidents:

Example 1: You caused an accident

- Scenario: You misjudged a roundabout manoeuvre and collided with another car, or you pulled out of a junction into oncoming traffic. You are deemed to be entirely at fault.

- With Comprehensive Insurance: Your comprehensive policy will cover the repairs to both your vehicle and the third party's vehicle. It will also cover any personal injuries sustained by either party. You would pay your policy excess.

- With TPFT Insurance: The third party will claim through your insurance to recoup their costs, including car repair, the cost of a hire car in the interim, and any personal injury claims. However, your own car's damage will not be covered by your policy, meaning you are responsible for paying for your own repairs.

Example 2: An accident where both parties are at fault - 50/50 Split Liability

- Scenario: You are reversing out of a parking space, and another car reverses into you simultaneously. Both parties could have taken action to prevent the collision. Insurers agree to split liability 50/50.

- With Comprehensive Insurance: Your car's repairs and any injuries to persons in it (including yourself) will be covered fully. Effectively, 50% of the cost is borne by your insurer and 50% by the other party's insurer (or your insurer recovers 50% from them). You would typically pay 50% of your excess.

- With TPFT Insurance: 50% of the costs for your car's repairs and any personal injuries you sustain will be covered by the other party's insurance. Your insurance will cover 50% of the third party's costs, but it will not cover your remaining 50% share of your own car's damage or your injuries. You would still be out of pocket for half of your repair costs.

Example 3: Another driver is entirely at fault

- Scenario: You are stopped at traffic lights, and another driver rear-ends your vehicle. They admit full responsibility.

- With Comprehensive Insurance: You can choose to claim through your own comprehensive policy, and your insurer will then recover their costs from the at-fault driver's insurer. This can often be quicker. You may have to pay your excess initially, but it should be reimbursed by your insurer once they've recovered costs from the other party.

- With TPFT or Third Party Insurance: You would make a claim directly against the at-fault driver's insurance. Their policy would then cover the repairs to your vehicle and any personal injuries you or your passengers sustained. This process can sometimes take longer, as it relies on the other insurer's assessment and acceptance of liability.

What if My Car Has a Manufacturing Defect?

This is a specific type of "faulty" car that falls outside the remit of standard car insurance. If your car develops a fault due to a defect in its design or manufacturing, this is typically covered by the manufacturer's warranty. New cars come with a warranty (often 3-7 years, depending on the manufacturer) that covers mechanical and electrical defects that occur through no fault of the owner.

For second-hand cars, if purchased from a dealership, you may still have some protection under the Consumer Rights Act 2015. This act states that goods must be of satisfactory quality, fit for purpose, and as described. If a significant fault develops within the first six months of purchase, it's generally presumed to have been present at the time of sale, and the onus is on the dealer to prove otherwise. After six months, the burden of proof shifts to you.

It's crucial to understand that neither your car insurance nor breakdown cover will deal with manufacturing defects. Always refer to your car's warranty booklet or seek advice from the dealership or a consumer rights organisation if you suspect a manufacturing fault.

Beyond Standard Car Insurance: Other Protections for Mechanical Issues

While your standard car insurance won't cover mechanical breakdowns or wear and tear, other financial products can offer protection:

- Extended Warranties: Once your manufacturer's warranty expires, you can often purchase an extended warranty. These are designed to cover the cost of repairs for specific mechanical and electrical components should they fail. The scope of coverage varies significantly, so always read the policy terms carefully.

- Breakdown Cover: Services like the AA, RAC, or Green Flag provide assistance if your car breaks down due to a mechanical or electrical fault. While they don't pay for the actual repairs, they will get you to a garage. Some premium breakdown policies may include a contribution towards repair costs, but this is rare and limited.

- Guaranteed Asset Protection (GAP) Insurance: If your car is declared a total write-off after an accident or theft, standard comprehensive insurance pays out the car's market value at the time of the incident. This can be significantly less than what you originally paid or what you still owe on finance. GAP insurance bridges this "gap," paying the difference between your insurer's payout and the original purchase price or outstanding finance.

When Your Insurance Might Not Pay Out: Invalidating Your Policy

Even with the highest level of comprehensive cover, there are specific circumstances under which your insurer will refuse to pay out for damages or injuries. These scenarios typically involve a breach of your policy terms or illegal activity:

- Driving Without a Valid Licence: If you are driving without a current and appropriate driving licence.

- Driving Under the Influence: Operating your vehicle while impaired by drugs or alcohol.

- Unnamed Driver: If the person driving your car at the time of the incident is not named on your insurance policy and is not covered by a specific "driving other cars" clause (which is rare and limited).

- Careless or Reckless Behaviour Leading to Damage/Theft: While comprehensive insurance covers accidental damage, deliberate or extremely careless actions that lead to damage or theft (e.g., leaving keys in an unlocked car with the engine running) can invalidate a claim.

- Misrepresentation: Providing false or misleading information when taking out the policy (e.g., incorrect address, mileage, occupation).

- Unroadworthy Vehicle: Driving a vehicle that you know to be in an unroadworthy condition (e.g., bald tyres, known critical mechanical fault that contributes to an accident).

Always ensure you fully understand your policy's exclusions and obligations to avoid the devastating financial consequences of an invalid claim.

Frequently Asked Questions (FAQs)

Q: Can I get insurance specifically for mechanical faults?

A: Standard car insurance does not cover mechanical faults due to wear and tear. You would need to look into an extended warranty, either from the manufacturer, a dealership, or a third-party provider. These are separate products from car insurance.

Q: Does car insurance cover pre-existing damage?

A: No, car insurance does not cover damage that existed before you took out the policy or before the incident you are claiming for. Insurers are only liable for new damage that occurs during the policy period due to an insured event.

Q: What happens if my car breaks down, but there's no accident?

A: If your car breaks down due to a mechanical fault (e.g., engine failure, flat battery) and no accident has occurred, your standard car insurance policy will not cover the repair costs. This is where breakdown cover (e.g., AA, RAC) comes in handy to get your car recovered to a garage.

Q: Is an MOT failure covered by insurance?

A: No, an MOT failure indicates that your vehicle does not meet the minimum safety and environmental standards required to be roadworthy. The costs of repairs needed to pass an MOT are considered routine maintenance and are not covered by car insurance.

Q: How do I make a car insurance claim?

A: If you're involved in an incident that you believe is covered by your policy, you should contact your insurer as soon as possible, usually within 24-48 hours. Provide them with all the details of the incident, including dates, times, locations, and any third-party details. They will guide you through their specific claims process.

Conclusion

Navigating the question of "Who pays for repairs if a car is faulty?" boils down to understanding the fundamental purpose of car insurance. It is a safety net for unforeseen events like accidents, theft, and fire, not a fund for routine maintenance, wear and tear, or mechanical breakdowns. While comprehensive policies offer extensive protection against accident-related damage, they won't cover your car when its engine simply gives up due to age or a component fails from overuse. For those types of "faults," you'll need to rely on manufacturer warranties, extended warranties, or your own savings. Always review your policy documents thoroughly to understand your specific coverage and limitations, ensuring you're prepared for whatever the road throws your way. Being informed is your best defence against unexpected repair bills.

If you want to read more articles similar to Faulty Car Repairs: Does Your Insurance Pay?, you can visit the Insurance category.