25/03/2015

In 2024, many households across the UK are feeling the pinch. With the relentless rise in mortgage and rent payments, childcare costs, and car insurance premiums, managing car finance often becomes an unexpected burden. If you find yourself in this challenging position, struggling to meet your car finance payments, you're not alone. Fortunately, UK consumer law provides a vital lifeline: Voluntary Termination (VT). This legal right, often overlooked or actively downplayed by finance companies, allows you to end your car finance agreement early under specific conditions. Understanding how to exercise this right can save you from deeper financial distress, potentially offering a more favourable outcome than repossession or defaulting on payments. This comprehensive guide will walk you through everything you need to know about initiating a Voluntary Termination, ensuring you are well-equipped to navigate the process with confidence.

- Understanding Voluntary Termination (VT)

- Which Car Finance Agreements Qualify for VT?

- Why Might You Consider Voluntary Termination?

- Your Legal Right to Terminate: The 50% Rule

- VT vs. Other Ways of Ending Your Contract

- Critical Timing: Don't Lose Your Right to VT

- How to Initiate Your Voluntary Termination (VT)

- Should You Make an Affordability Complaint?

- Common Problems You Might Encounter & How to Address Them

- What if I Want to Keep My Car?

- Frequently Asked Questions (FAQs)

Understanding Voluntary Termination (VT)

Voluntary Termination (VT) is your legal right to end a Hire Purchase (HP) or Personal Contract Purchase (PCP) finance agreement early. It's a provision enshrined in UK law, specifically Section 99 of the Consumer Credit Act 1974, designed to protect consumers. Essentially, if you've paid a certain portion of the total amount payable under your agreement, you have the right to hand the car back and walk away, often with no further payments.

This option is particularly relevant in today's economic climate. When faced with the prospect of unmanageable car finance payments, VT offers a structured and legally sound alternative to simply defaulting. While finance companies may not actively suggest VT – as it’s generally less profitable for them than you continuing to pay – knowing your rights can empower you to make the best decision for your financial well-being. It's often a far better route than allowing the lender to repossess the vehicle, which can lead to significantly higher costs and a more detrimental impact on your credit file.

Which Car Finance Agreements Qualify for VT?

It's crucial to understand which types of car finance agreements fall under the protection of Voluntary Termination. VT applies to agreements where you are hiring the car with an option to purchase, meaning the finance company retains ownership until the final payment is made. The main types are:

- Hire Purchase (HP): This is the most straightforward type of agreement where VT applies. You make regular payments over a set period, and at the end, you own the car.

- Personal Contract Purchase (PCP): Although PCP contracts include a large 'balloon payment' at the end, they are legally considered a type of HP agreement. Therefore, the same VT rules and protections apply as with traditional HP contracts.

- Conditional Sale: Very similar to HP, with the condition being that ownership transfers to you once all payments are made. The terms for VTing a car under a Conditional Sale agreement are identical to those for HP. For the purposes of this article, wherever HP is mentioned, the same applies to Conditional Sale contracts.

However, there are important exclusions:

- Leasing Agreements: If you are leasing a car (sometimes called Personal Contract Hire or PCH), you do not have a right to Voluntary Termination. With leasing, you never own the car; you are simply renting it for a fixed period.

- Personal Bank Loans: If you borrowed money from your bank to buy a car, you typically have a simple, unsecured loan. In this scenario, you own the car outright from the start. If you struggle with repayments, the bank cannot repossess your car, as the loan isn't directly tied to the vehicle itself. Your options here would involve negotiating with your bank or seeking debt advice for the loan itself.

Why Might You Consider Voluntary Termination?

There are several compelling reasons why you might explore the option of handing back your car through VT:

- Unaffordable Repayments: This is perhaps the most common reason. If, due to unforeseen circumstances like job loss, illness, or simply the rising cost of living, you can no longer comfortably afford your monthly payments, VT provides a legal exit strategy. Before proceeding, it's always advisable to seek free debt advice from organisations like National Debtline, who can help you assess all your debt options.

- Negative Equity in the Car: Sometimes, the market value of your car falls faster than your finance balance, or high interest rates mean you're paying off very little capital. This can lead to a situation where you owe more on the car than it's worth. VT can cap your financial liability at the 50% figure, which is often significantly less than the total outstanding balance, especially in PCP agreements with a large balloon payment.

- Car No Longer Suitable: Your needs might change. Perhaps you need a larger family car, or you no longer require a car for commuting. Whatever your reason for wanting a different vehicle, VT can allow you to exit your current agreement without incurring the potentially high costs associated with early settlement or trade-in when in negative equity.

Regardless of your specific motivation, the procedure for initiating a Voluntary Termination remains the same.

Your Legal Right to Terminate: The 50% Rule

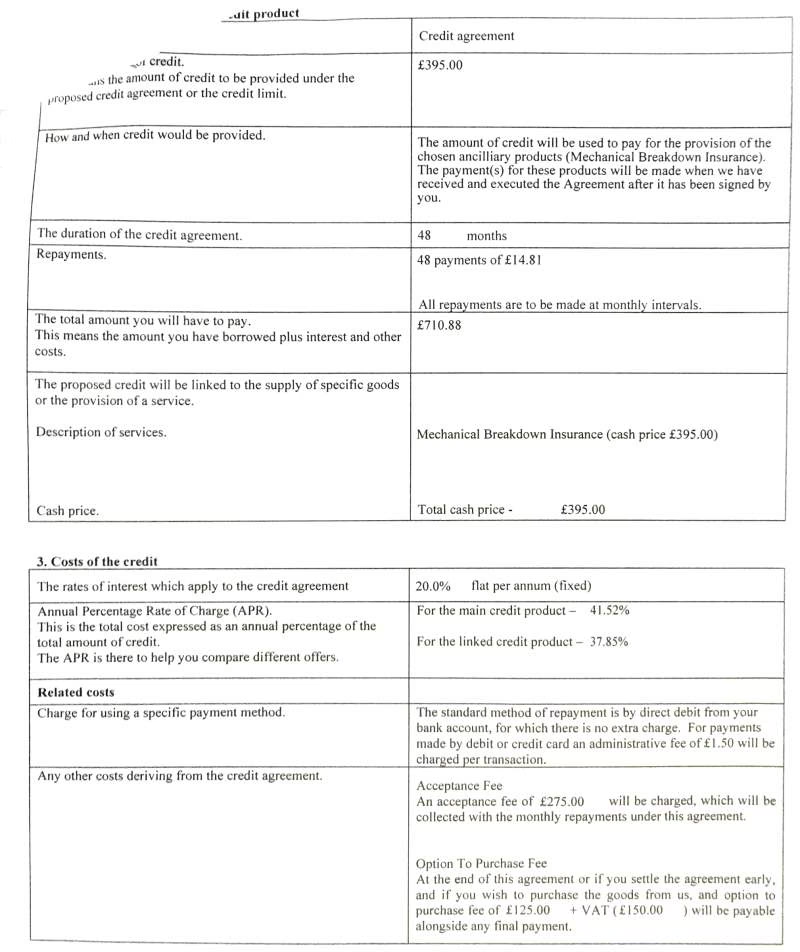

The foundation of your right to Voluntary Termination lies within Section 99 of the Consumer Credit Act 1974. Your original finance agreement, whether HP or PCP, will contain a clause outlining this right. It typically reads something similar to:

"TERMINATION: YOUR RIGHTS. You have a right to end this Agreement. To do so, you should write to the person you make your repayments to. They will then be entitled to the return of the Goods and to half the amount payable under the agreement, that is [£x – the exact figure for your contract]. If you have already paid at least this amount plus any overdue instalments and have taken reasonable care of the goods, you will not have to pay any more."

The Crucial 50% Figure

The '[£x]' mentioned above is the 50% figure, representing half of the total amount payable under your agreement. This figure is paramount. You must locate it in your finance contract. For a traditional HP contract, where payments are usually consistent, you will typically reach this 50% threshold roughly halfway through your payment schedule.

However, for PCP contracts, the large lump sum (balloon payment) due at the end is included in the 'total amount payable'. This means you will likely be much further than halfway through your monthly payments before you reach the 50% figure. It's not uncommon for this threshold to be met closer to two-thirds or three-quarters of the way through a PCP term.

What You Owe After VTing the Car

Your financial liability after Voluntary Termination depends on how much you've already paid:

- You have paid less than the 50% figure: You can still VT your car! The termination clause does not state that you must have reached the 50% mark before you can terminate. Upon VT, you will owe the difference between what you have already paid and the 50% figure. This amount becomes a debt you will need to settle with the finance company.

- You have paid at least the 50% figure with no arrears: In this ideal scenario, you can hand back the car, and you will not owe any more money at all to the finance company. It's important to note, however, that if you have paid more than the 50% figure, you will not receive any money back from the lender.

- You have paid more than the 50% figure and you have some arrears: Again, you can still VT your car. You do not have to clear the arrears before terminating the agreement. However, when you VT the car, you will still owe the outstanding arrears to the finance company.

The 'Reasonable Care' Clause

The other critical aspect of the termination clause is the requirement to have 'taken reasonable care' of the goods (the car). This means returning the vehicle in a condition consistent with its age and mileage, allowing for normal wear and tear. It does not mean the car must be in showroom condition. Lenders often attempt to recoup losses by alleging excessive damage, sending invoices for minor paintwork scuffs or alloy wheel marks.

To protect yourself against unreasonable charges, it is absolutely vital to thoroughly photograph the car, inside and out, from all angles, before it is returned. Document any existing minor marks and the overall condition. This photographic evidence will be your strongest defence if the lender tries to claim for damage beyond what is considered fair wear and tear. Consult guides on 'fair wear and tear' standards to understand what is generally acceptable.

VT vs. Other Ways of Ending Your Contract

It’s important to understand that Voluntary Termination is distinct from other ways a car finance agreement might end, and often far more financially advantageous.

The Cost of Alternatives

- Repossession or Lender Termination: If you simply stop paying, or if the lender terminates the contract due to arrears, you typically lose the protection of the 50% cap. In this scenario, you could be liable for the *entire* remaining amount payable under the contract, less whatever the car sells for at auction. Cars sold at auction by finance companies often fetch lower prices, leaving you with a substantial debt.

- Voluntary Surrender: This is a common trap. If you hand back the car without formally invoking your right to Voluntary Termination, it may be treated as a 'voluntary surrender'. This does not provide the same legal protections as VT, meaning you could still be liable for a significant portion of the outstanding finance, similar to repossession. Always use the specific language 'Voluntary Termination' and follow the correct written procedure.

Comparison Table: Ending Your Car Finance

| Action | Cost Implications | Ownership | Legal Right / Basis |

|---|---|---|---|

| Voluntary Termination (VT) | Liability capped at 50% of total amount payable (plus arrears/damage). Often the cheapest option if in negative equity. | Lender owns until VT is complete. | Statutory right under Consumer Credit Act 1974. |

| Lender Repossession | Owe full remaining contract value minus sale price (often low auction price). Can be very expensive. | Lender owns. | Lender's right if arrears/breach of contract. |

| Voluntary Surrender | Similar to repossession, you owe the full amount. No 50% cap. | Lender owns. | No specific statutory right/protection. |

| Selling (Settlement) | Pay off the full settlement figure. If sale price is less, you cover the difference. | Lender owns until settled, then buyer. | Requires finance company's agreement. |

What About Selling the Car?

Since you don't legally own the car under HP or PCP until the final payment, you cannot simply sell it yourself. However, you can arrange to settle the car finance early through a sale. To do this, you'll need to contact your finance company and request a 'settlement figure'. This is the total amount required to pay off the finance and gain ownership. Some specialist firms buy cars in this situation and can help facilitate the process, covering the settlement figure directly with the finance company and paying you any remaining equity (or you paying them if in negative equity).

Critical Timing: Don't Lose Your Right to VT

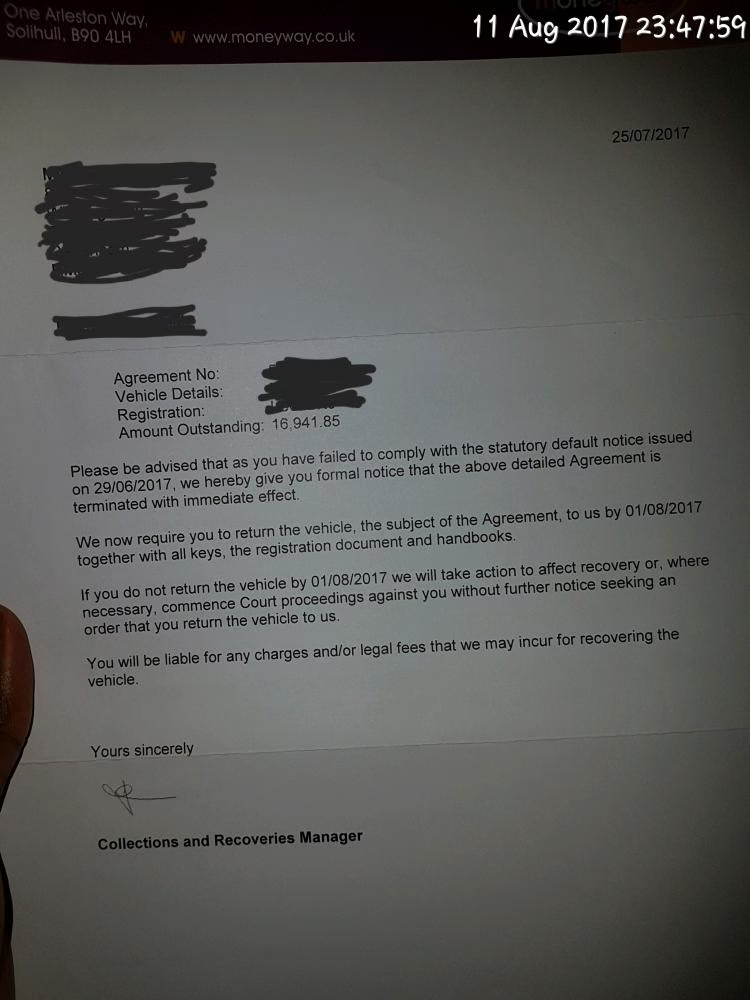

This is a crucial point: you can only terminate your contract if it is still ongoing. If the finance company terminates your contract first due to arrears or a breach of the agreement, you lose your statutory right to Voluntary Termination. As explained above, this can lead to a much larger debt.

Therefore, if you anticipate or are already experiencing difficulties with your car finance payments, it’s vital to act promptly. Don't panic if you miss just one payment, as lenders must follow specific procedures. They are usually required to send you a Default Notice, giving you a chance to pay the arrears before they can terminate the contract. However, as soon as you know you have a problem, seek debt advice. Having a clear understanding of your options beforehand will allow you to act quickly if you receive a Default Notice, potentially allowing you to VT before the lender takes more drastic action.

How to Initiate Your Voluntary Termination (VT)

The process for VT is straightforward, but it requires careful adherence to the correct steps to ensure you benefit from your legal protections.

1. Notify the Finance Company in Writing

This is the most critical step. You must inform the finance company in writing that you are terminating your contract. Do not rely on phone calls alone. If you simply return the car or tell them verbally, it might be treated as a 'voluntary surrender', which, as discussed, does not offer the same legal protection as VT.

- Use a Template Letter: Organisations like National Debtline provide simple template letters for Voluntary Termination. Using one of these ensures all necessary legal wording is included.

- Send by recorded delivery: Mail the letter to the finance company's official address (found in your credit agreement). This provides proof that you sent the letter and that they received it. Keep a copy of the letter and the proof of postage. While not legally required, sending a copy by email can also be a good idea for an additional record.

- Be Clear on the Phone: If you speak to the lender on the phone, always use the phrases 'terminate my agreement' or 'voluntary termination'. Do not agree if they ask if you want to 'surrender' the car or have it 'repossessed' – these are not VT.

- Refuse to Sign Lender's Documents: The finance company may send you their own forms or ask you to sign documents. It is generally best to refuse to sign anything other than your original VT letter, as these documents might contain clauses that waive your rights or impose additional charges.

2. Handle Personalised Registration Plates

If your vehicle has a personalised (private or cherished) registration plate, you must address this before returning the car:

- Apply to DVLA: You need to apply to the DVLA (Driver and Vehicle Licensing Agency) to have your personalised plate removed from the vehicle. This must be done *before* you return the car.

- Consequence of Not Removing: If you don't remove it, the finance company will sell the vehicle with your private plate still attached, and you will lose the right to use it.

- New V5C (Logbook): The DVLA will send you a new V5C registration document (also known as a logbook) reflecting the standard registration. This typically takes 4 to 6 weeks. The finance company cannot collect your vehicle until you have this new logbook.

- Re-fit Old Plates: The DVLA will usually confirm that the vehicle registration will revert to its old, original one. Please ensure you put these old, standard plates back on the vehicle before it is collected.

3. Returning the Car

Once you've formally notified the lender and handled any personalised plates, they will arrange the return of the vehicle:

- Collection or Delivery: The lender will provide details on how to return the car. They may ask you to deliver it to a specific location (this should not be an unreasonable distance away), or they may arrange to pick it up from your home.

- No Collection Charge: You should not be asked to pay a charge for the collection or return of the vehicle.

- Prepare the Vehicle: Ensure all keys, the full service history, any manuals, and accessories (e.g., locking wheel nuts) are with the car.

- Document Condition (Crucial!): Before the car is handed over, take extensive, high-resolution photographs and videos of the entire vehicle. Document the interior, exterior, wheels, and dashboard mileage. This evidence is vital to counter any potential claims for unreasonable damage.

4. Settling Any Remaining Money

After the car has been returned, the finance company will assess its condition and confirm your final liability:

- Confirmation of Debt: They will either confirm that you owe nothing further or provide a statement detailing any outstanding amounts (e.g., the difference to the 50% figure if you hadn't reached it, any arrears, or charges for damage beyond reasonable care).

- Challenge Unfair Calculations: If you believe their calculation is unfair or includes unreasonable damage charges, you should challenge it in writing, providing your photographic evidence.

- Settling Valid Debts: If there's a valid debt, you'll need to settle it. You can propose an affordable monthly payment plan based on your budget. National Debtline offers tools to help you create a budget. While lenders can take you to court for a County Court Judgment (CCJ) if you don't pay, many will accept reasonable payment offers.

Should You Make an Affordability Complaint?

If your car finance was a struggle from the outset, causing you difficulty in paying other essential bills and living expenses, the finance agreement itself may have been 'unaffordable'. For instance, if your other debts (like credit cards or overdrafts) were increasing while you were trying to keep up with car payments, this is a strong indicator.

You can make an affordability complaint even after you have voluntarily terminated the car. Winning such a complaint can have significant benefits:

- It can clear any remaining debt you might owe after the VT (e.g., the difference to the 50% figure or damage charges).

- You may even be entitled to a cash refund of some of your payments.

- Any negative markers related to the car finance on your credit record could be removed or amended.

There are template letters available online (e.g., from consumer debt advice sites) to guide you through making an affordability complaint.

Common Problems You Might Encounter & How to Address Them

While many people experience a smooth VT process, it's wise to be aware of potential issues and how to tackle them. For any of these problems, organisations like National Debtline and forums like Legal Beagles' Vehicle Finance section are invaluable resources for advice and support.

1. "Lender Says I Can't Terminate the Contract"

Some lenders may incorrectly claim you cannot VT because you haven't yet paid 50% of the total amount, or because you have arrears. This is incorrect. Your right to terminate is statutory and not conditional on having reached the 50% figure or being free of arrears (though you will owe any difference or arrears).

- Your Response: Firmly reiterate that you are terminating your contract under Section 99 of the Consumer Credit Act 1974, and that Sections 99 and 100 do not state that termination is conditional on having paid half the total contract amount or on not having arrears.

- Escalation: If the lender persists, lodge a formal written complaint with them. State clearly that if the complaint is not resolved, you will escalate it to the Financial Ombudsman Service (FOS). You can take your complaint to the FOS as soon as it's rejected by the lender in writing, or after 8 weeks if you haven't received a response.

2. Making it Difficult to Return the Car

Lenders might try to make the return process inconvenient or costly, for example, by:

- Adding charges for collection.

- Insisting you complete their specific documentation (which you should generally refuse to sign).

- Demanding you deliver the car to a location that is an unreasonable distance away.

Seek advice if this happens. Legal Beagles often has useful template letters for challenging such tactics.

3. Unreasonable Charges for Damage to the Car

As mentioned, lenders may try to charge for damage beyond reasonable care. If you believe the amount requested is excessive or for fair wear and tear:

- Challenge in Writing: Write to the lender, detailing why you dispute the charges. Refer to your photographic evidence and argue what constitutes fair wear and tear for a vehicle of that age and mileage.

- Escalate to FOS: If you cannot resolve the dispute directly, take your complaint to the Financial Ombudsman Service. The FOS has a track record of intervening and reducing unreasonable wear and tear charges, as seen in cases reported by The Times where fees were substantially reduced after FOS intervention.

4. Excess Mileage Charges (PCP Contracts)

PCP contracts include an agreed annual mileage limit, with charges for exceeding it. When you VT the car, finance companies typically demand payment for any excess mileage accrued. This is a somewhat 'grey area' legally:

- Legal Debate: Some legal experts argue that excess mileage charges are not part of the 'total amount payable' and therefore should not be owed under a VT. However, Financial Ombudsman Service decisions on this issue have been mixed, with some ruling it is fair for excess mileage charges to be paid upon VT.

- Challenging the Charge: If you wish to challenge an excess mileage charge, be prepared for a potentially lengthy and determined fight, possibly involving exchanges with the finance company's solicitors and even a readiness to go to court. The Legal Beagles forum can offer significant support and guidance if you choose this path.

What if I Want to Keep My Car?

Voluntary Termination is the right choice when you can no longer afford or no longer want the car. If your primary goal is to retain the vehicle despite financial difficulties, VT may not be your best option. In this scenario, you should explore other alternatives, such as:

- Negotiating with your finance company for a temporary payment holiday or reduced payments.

- Making an affordability complaint, which could lead to a restructuring of your finance.

- Seeking comprehensive debt advice to explore all available solutions for your overall financial situation.

Always ensure you understand all your options before making a decision, especially one as significant as ending a finance agreement.

Frequently Asked Questions (FAQs)

Q: Will Voluntary Termination affect my credit score?

A: Yes, a Voluntary Termination will be noted on your credit file. However, it is generally considered less damaging than a default or a repossession, as it is a legal right you are exercising. If you owe money after VT (e.g., for the difference to the 50% figure, arrears, or valid damage charges) and fail to pay it, this unpaid debt will negatively impact your credit score.

Q: Can I VT my car if I have missed payments or am in arrears?

A: Yes, you can still exercise your right to Voluntary Termination even if you have missed payments or are in arrears. However, you will still be liable for any outstanding arrears at the point of termination. These arrears will need to be paid to the finance company after the car is returned.

Q: How long does the Voluntary Termination process take?

A: The initial notification to the lender is immediate. The time it takes for the car to be collected or returned depends on scheduling with the finance company. If you have a personalised registration plate, the DVLA processing for a new V5C can take 4 to 6 weeks, which will delay the car's collection. The final settlement of any outstanding money can take longer if there are disputes over damage or calculations.

Q: Do I need a solicitor to VT my car?

A: No, you do not legally require a solicitor to exercise your right to Voluntary Termination. It is a statutory right under the Consumer Credit Act 1974. However, if the finance company is being particularly difficult, uncooperative, or making unreasonable demands, seeking advice from organisations like National Debtline or consumer forums like Legal Beagles can be extremely helpful.

Q: What is considered "fair wear and tear"?

A: Fair wear and tear refers to the normal deterioration of a vehicle that occurs naturally with age, mileage, and regular use. It does not include damage caused by accidents, neglect, or misuse. Examples of fair wear and tear might include minor stone chips, light surface scratches consistent with the car's age, and normal tyre wear. Dents, deep scratches, cracked windscreens, torn upholstery, or significant damage would typically be considered beyond fair wear and tear and could incur charges.

If you want to read more articles similar to Voluntary Termination: Ending Your Car Finance, you can visit the Automotive category.